Key takeaways

Australian consumer sentiment has fallen to 80.6 on the Westpac-Melbourne Institute index, among the weakest readings in the survey's 50-year history

Life satisfaction has dropped below pandemic-era lows, with more than one in three Australians struggling on their current income

Cost of living, interest rate pressure, and policy uncertainty around the federal budget's property tax changes are the main drivers

Sentiment is a measure of current mood, not future property performance - the two regularly diverge

Quality property in undersupplied, owner-occupier driven locations remains strategically sound regardless of the sentiment cycle

Investors who separate their decision-making from the emotional noise of the moment consistently outperform those who don't

The New Zealand precedent suggests negative gearing restrictions on new builds are more likely to lift rents on established property than to drive sustained price falls

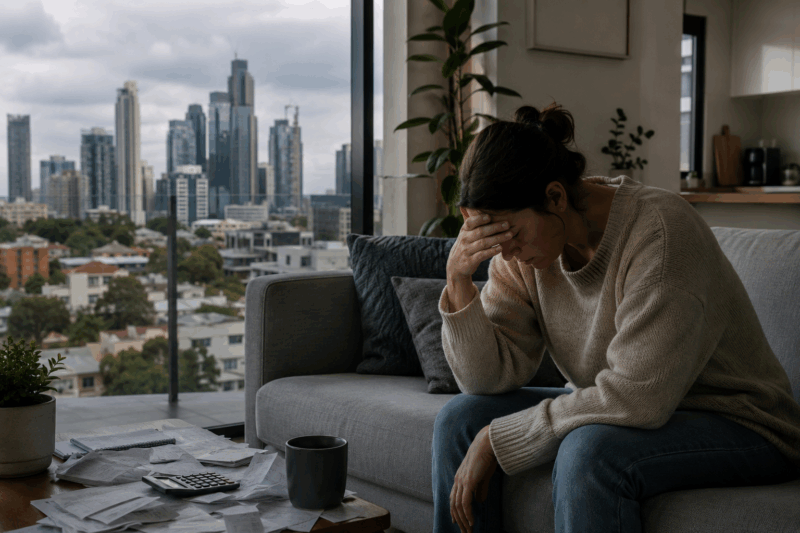

There's a troubling irony in the latest data on how Australians are feeling about their lives.

We endured lockdowns, closed borders, business shutdowns, and genuine fear about a global pandemic, and apparently, we were happier then than we are right now.

New research from the Australian National University found that life satisfaction has fallen to its lowest recorded level in the ANUpoll series, reaching levels below even the depths of the pandemic lockdowns.

Average life satisfaction has dropped to just 6.22 on a scale of zero to ten. The previous record low was 6.52, recorded in April 2020 when much of the country was in lockdown.

We've now gone below that and the mood on financial matters is just as bleak.

The numbers are hard to ignore

The Westpac-Melbourne Institute Consumer Sentiment Index dropped 2.9% in June to 80.6, back amongst the weakest readings in the survey's fifty-year history, with pessimists now outnumbering optimists by nearly 20%.

The 'family finances vs a year ago' and 'family finances, next 12 months' sub-indexes both dropped sharply in June, giving up almost all of their May gains to be back near April lows.

More than one in three Australians - 34.9% - said they are finding it difficult or very difficult to get by on their current income, a record high for the survey.

Professor Nicholas Biddle from the ANU said the current decline showed a country under "considerable strain", with life satisfaction now lower than at any point during the 2020s - lower than during COVID lockdowns and lower than when inflation was at its peak a couple of years later.

What's actually driving this?

Cost of living is clearly front and centre.

Three consecutive RBA rate rises in 2026 have returned the cash rate to 4.35%, and while there's been some relief at the petrol pump from a temporary fuel excise reduction, Westpac's Matthew Hassan noted that cost-of-living issues came back with a vengeance in June, with the fuel excise halving providing only a small and brief reprieve.

But it goes deeper than household budgets. For the first time in the ANUpoll series, more Australians are dissatisfied with the direction of the country than satisfied, with 54% saying they were not very or not at all satisfied.

Nearly three in five Australians - 59.1% - believe life was better 50 years ago, and a similar proportion expect it to be worse in 50 years' time.

That's a marked level of pessimism about the future, especially when you consider how much living standards have improved materially over the decades.

Biddle noted that while incomes and life expectancy have risen, there are objective measures that are noticeably worse - access to the housing market and the cost of education among them.

There's also something else brewing.

Just over 30% of workers are now concerned that machines or computer programs will replace their jobs - a concern that has nearly doubled since 2018. The anxiety around AI and job security is clearly feeding into the general unease.

And on property specifically, Westpac noted a sharp drop in house price expectations, suggesting some consumers are becoming more unsettled about the impact of the recently announced tax changes - meaning the federal budget's negative gearing and CGT reforms are already weighing on the psychology of the market, even before they take effect.

What sentiment data actually tells us about property

I've been tracking property markets through enough cycles now to have a healthy respect for sentiment data - and an equally healthy scepticism about how most people interpret it.

Consumer sentiment is a measure of how people feel right now. It's shaped by the headlines they're reading, the conversations they're having, and the pressure on their household budgets at this particular moment.

What it doesn't measure is the underlying structural forces that drive property values over the long run.

And over the years, I have learned that sentiment and property values have an imperfect relationship at best.

Some of the best buying opportunities I've seen, and some of the best returns our clients at Metropole have achieved, came during periods when consumer confidence was deeply negative.

- Also read:Melbourne property market forecast for 2026 & 2027 | Separating the fundamentals from the sentiment

- Also read:Brisbane Property Market Forecast [2026 & Beyond] – What The Olympics Decade Means for Investors.

- Also read:Sydney property market forecast for 2026 and 2027 | Why the short-term softness is a long-term opportunity

- Also read:Latest Property Price Forecasts. Australian Property Market Outlook 2026-2027: Navigating a Market Correction

- Also read:Everything you need to know about the state of Australia’s property markets in 20 charts – July 2026

Warren Buffett's famous advice about being greedy when others are fearful applies to property markets every bit as much as it does to share markets.

When sentiment is low, and buyers are cautious, competition thins out, vendors become more flexible, and patient investors can secure quality assets on better terms than they'd find at the top of a cycle.

The distinction that matters

There's an important difference between sentiment affecting the mood of the market and sentiment changing the fundamental investment case for quality property.

Sentiment affects transaction volumes, it affects auction clearance rates in the short term, and it can cause some price softening in weaker market segments.

What it doesn't change is the long-run supply-demand equation underpinning well-located property in our major cities.

Australia's housing shortage hasn't gone anywhere. Sydney and Melbourne are both significantly undersupplied relative to population growth and household formation. Brisbane's structural story is strengthening as 2032 Olympics infrastructure spending accelerates.

None of that changes because consumer confidence indices are printing near their lowest levels in fifty years.

The ANU data also showed that Australians with higher levels of education reported higher life satisfaction, lower financial stress, and greater confidence in institutions.

In my experience, the property investors who build genuine wealth are those with the financial literacy and emotional discipline to separate how they feel from what the data is telling them about long-run fundamentals.

A word on the Budget's impact on sentiment

I don't think that the timing of this sentiment slump is random.

The May 2026 federal budget's changes to negative gearing - limiting it to new builds for properties purchased after budget night - and the proposed CGT discount adjustments from July 2027 have added a layer of policy uncertainty that's clearly unsettling some home buyers and investors.

Westpac's analysis pointed to a sharp drop in house price expectations as one of the more notable shifts in the June survey, which they linked directly to consumer concern about the recently announced tax changes.

My view is that the policy changes will have a more modest impact on established investment-grade property than the headlines suggest.

Existing investors are fully grandfathered on the negative gearing changes, and quality assets in inner and middle-ring suburbs have always been driven more by owner-occupier demand than by the tax strategies of investors.

Those fundamentals don't shift because of a budget announcement.

The more likely outcome, as we saw when New Zealand made similar negative gearing changes, and when negative gearing was removed in the 1980s in Australia, is upward pressure on rents as investment in new supply becomes the only tax-effective path - which in turn supports yields for existing landlords with established property.

Staying strategic when the headlines are negative

Clearly, the psychological challenge for investors right now is real.

When the news cycle is relentlessly negative, when your neighbours are anxious, when the dinner party conversation has shifted from "property always goes up" to "now isn't the time" - that's precisely when your strategy and your discipline matter most.

At times like this, the gap between investors who act on sound fundamentals and those who act on sentiment widens. The former build wealth; the latter wait for certainty that never quite arrives.

The Australian economy has structural strengths that don't disappear because consumer confidence has taken a hit - strong population growth driven by migration, a tight labour market at 4.3% unemployment despite the anxiety around job security, and a chronic undersupply of housing in every major city.

The conditions that drive long-run capital growth in quality property haven't changed. What's changed is the mood of the market - and for prepared investors with a strategic plan, that's more of an opportunity than a threat.

At Metropole, we work with investors who understand that wealth is built across decades, not during the brief windows when everything feels comfortable. If you'd like to talk through what this environment means for your property strategy, click here now to organise a chat with one of the wealth strategists at Metropole.