Key takeaways

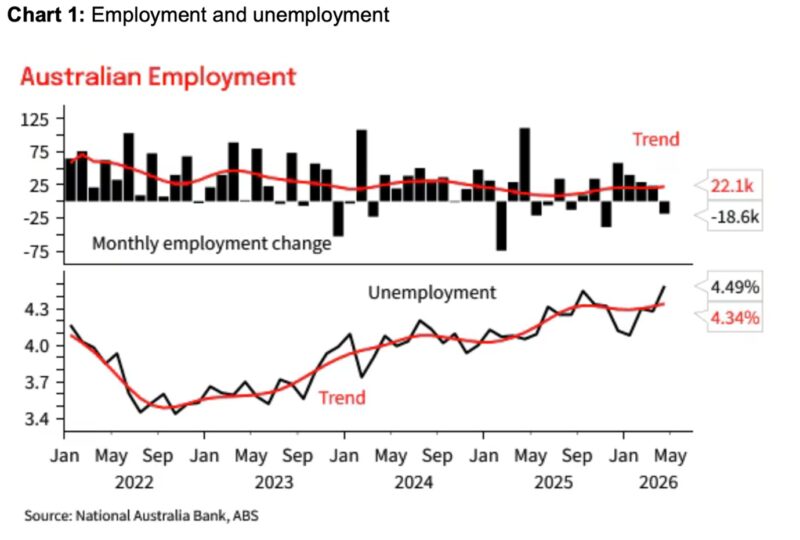

Australia’s unemployment rate rose to 4.5% in April, with employment falling by 19,000 jobs, but much of the weakness was concentrated in volatile youth employment data

The softer labour market has reduced the likelihood of a June rate rise, with NAB now expecting the next RBA increase to be delayed until August.

Westpac now holds a “high conviction” view that the RBA will pause in June, although both major banks still expect at least one more rate rise later this year.

Businesses appear to be slowing hiring rather than cutting jobs, while workers are seeking extra hours to cope with rising living costs and energy prices.

For property investors, a delayed rate rise offers short-term relief, while long-term property fundamentals like undersupply and population growth remain supportive of capital growth.

Fresh data from the Australian Bureau of Statistics released today shows the unemployment rate climbed to 4.5% in April, up from 4.3% in March, with employment falling by around 19,000 people in the month.

The unemployment rate is now at a level above Federal Treasury and the Reserve Bank’s forecasts, and that’s before the full impact of three rate hikes and soaring prices on the back of the Middle East conflict kick in.

On the surface, that may sound a little alarming, but before you read too much into a single month's numbers, it's worth understanding what's actually going on here.

The April result was worse than most economists forecast as market consensus were forecasting unemployment to hold at around 4.3% and employment to rise by roughly 15,000 people, so this landed well below the bar.

Some of the weakness could be tied to Easter falling unusually inside the survey window this year, which introduced seasonal distortions that aren't fully captured by the standard adjustment process.

The youth cohort aged 15 to 24 accounted for essentially the entire downside surprise, with youth employment collapsing by 56,400 and youth unemployment jumping 0.9 percentage points to 11.1%.

Moves of that scale in that age group are typically very noisy, and it is likely this will wash out when the May numbers are released.

So there's genuine reason to be cautious about over-interpreting one month's data.

The trend unemployment rate, which smooths out these fluctuations, actually held steady at 4.3%, and trend employment continued to grow at a modest pace.

That said, the headline number is still a new cycle high, and it sits awkwardly alongside the RBA's own forecasts.

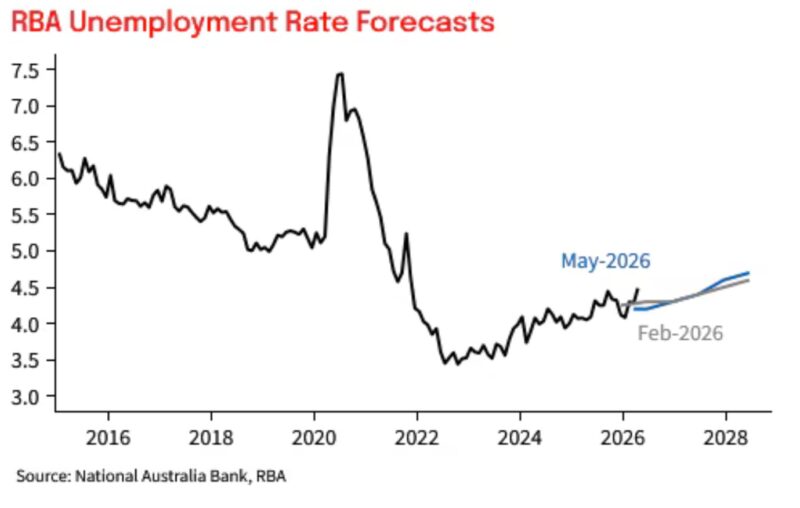

The RBA's May Statement on Monetary Policy projected unemployment would average 4.2% across the second quarter before ending the year at 4.3%. We're already above that, and it's only May.

What the banks are now saying about rate hikes

NAB has revised its RBA call as a direct result of these stats.

They were previously expecting the RBA to lift the cash rate by another 25 basis points at the June meeting. They've now pushed that expectation to August.

Their reasoning is straightforward.

The RBA's board has been framing its decisions around two competing concerns - keeping a lid on inflation on one side, and protecting full employment on the other.

Today's data shifts the balance.

There's less urgency to lean firmly against inflation when the labour market is softening faster than expected, and NAB believes the RBA now has more justification to sit on its hands in June and monitor the incoming data.

- Also read:Land Prices Are Surging While Building Cost Growth Cools | Property Insiders

- Also read:Melbourne housing market update | July 2026

- Also read:Australian housing market update | July 2026

- Also read:Latest Property Price Forecasts. Australian Property Market Outlook 2026-2027: Navigating a Market Correction

- Also read:Everything you need to know about the state of Australia’s property markets in 20 charts – July 2026

Westpac has gone further, describing their call for an RBA pause in June as now "high conviction."

They do add that the chance the RBA waits even longer than August is not zero, particularly given the uncertainty flowing from Middle East conflict and its impact on oil prices and domestic cost pressures.

It's worth being clear though: neither bank is saying the rate hiking cycle is over. They're saying it's delayed.

Both still expect at least one more 25 basis point increase once the RBA gets clearer visibility on how energy prices are passing through to inflation.

The question has shifted from " a rate rise in June. in June?" to "June or August?" and possibly beyond.

The broader economic picture

Hours worked actually rose in April despite the fall in employment, which is a slightly odd combination.

Westpac flagged this as possibly reflecting workers seeking additional hours to buffer against rising living costs, particularly energy. That dynamic tends to appear in the early stages of a cost-of-living shock, before it fully feeds through into reduced employer demand.

NAB noted that businesses appear to be holding off on hiring amid elevated uncertainty rather than actively shedding staff.

The job finding rate - the share of unemployed people who move into employment in a given month - fell noticeably in April. That's a leading indicator worth watching.

What this means for property investors

For anyone with a variable rate mortgage or investment loan, a June pause from the RBA gives useful breathing room.

It means at least another six to eight weeks before any further pressure on repayments, assuming NAB's revised August call proves correct.

But I wouldn't be planning your investment strategy around the assumption that rates are done.

The RBA's primary concern remains inflation, and until we see clear evidence that energy price rises aren't embedding themselves in broader price expectations, the Board is going to remain cautious.

They have space to wait, and they're likely to use it.

The bigger picture for long-term investors hasn't really changed. A slightly looser labour market, combined with global uncertainty, reduces the risk of the RBA aggressively hiking rates - which is actually a more supportive environment for property over the medium term than many people appreciate.

The fundamentals that drive capital growth in well-located investment-grade properties aren't going to be derailed by one month's employment data.

Supply constraints remain significant, population growth is still absorbing demand, and the structural undersupply in our major cities isn't going to resolve quickly.

If you've been waiting for a clearer read on where rates are heading before making a decision, this data at least suggests the environment is becoming slightly more predictable.