Key takeaways

The Australian property market is no longer one market. It’s fragmented into multiple micro-markets, even within the same suburb, making broad assumptions dangerous.

The affordable end of the market is outperforming. Lower-priced properties are growing faster than premium ones due to policy support, rate cuts, and surging demand.

Supply shortages are intensifying price pressure. Entry-level homes are disappearing while demand rises, creating strong upward pressure on affordable housing.

Regional markets have structurally strengthened. Lifestyle migration and commodity cycles have driven long-term outperformance, narrowing the gap with capital cities.

Investors must adopt a targeted, not generic strategy. Success now depends on understanding specific micro-markets rather than relying on city-wide or national trends.

Here's something that might change the way you think about Australian property forever.

The media keeps talking about "the property market" as if it's one big, unified beast that either goes up or down.

But that's no longer how it works - in fact, arguably it never did work that way.

What's different now is that the fragmentation has become so pronounced and so structural that treating the market as a monolith isn't just misleading for investors and buyers, it could be genuinely costly.

The Australian property market isn't just moving in different directions across cities.

It's splitting within the same city, sometimes within the same suburb.

This means understanding why and what it means for your decisions is more important than ever.

Welcome to the K-shaped property market

You may have heard economists talk about a "K-shaped economy" - the idea that when economic conditions shift, different groups don't just recover at different speeds, they actually diverge, with some moving strongly upward while others trend down.

Ray White Chief Economist Nerida Conisbee has identified exactly this dynamic playing out in Australian housing, and she's calling it the "K-Turn."

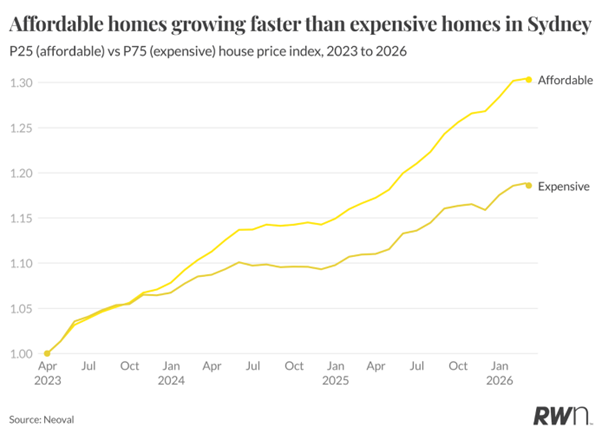

Conisbee explains that Sydney's housing market is now showing a striking divergence, but in the opposite direction of what you might expect. Instead of premium properties leading price growth as they usually do, the cheapest homes are doing the heavy lifting.

Since late 2023, house prices at the 25th percentile of the Sydney market have risen around twice as fast as those at the 75th percentile - creating a widening gap between the cheaper and more expensive ends of the market.

Source: Ray White

Think about that for a moment. It's the bottom of the market that's running hot, not the top. That's not how previous cycles have worked, and it tells us something important is changing.

Why is the cheap end of the market leading?

The short answer is government affordability, first home buyer policies, rates, and structural squeeze.

In October 2025, the federal government significantly expanded its 5% deposit guarantee scheme which allows eligible buyers to purchase with just a 5% deposit without paying lender’s mortgage insurance.

The impact was almost immediate, with first-home buyer loans in New South Wales rising 10.9% in the December quarter alone, roughly double the growth recorded for investor lending over the same period.

Three interest rate cuts during 2025 added further fuel. Affordable homes are consistently outpacing the wider market across most cities, with regional Queensland recording annual growth as high as 13.8%.

But there's also a deeper force at work here. Over the past decade, national house sales under $750,000 have fallen sharply, from about 248,000 in 2015 to roughly 153,000 in 2025.

In other words, entry-level detached homes are simply disappearing.

When supply contracts but demand surges (turbocharged by government schemes), prices at the affordable end don't just firm up - they can rocket.

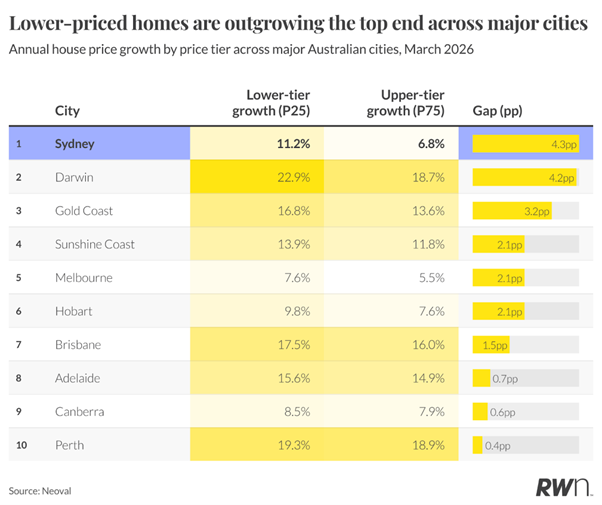

It's not just a price-band Split. It's a geographic split too.

The K-Turn isn't only about cheap vs. expensive. The fragmentation runs right through the geography of Australia's property landscape.

Source: Ray White

Melbourne and Darwin, both slow to join the upswing, are now firmly back in growth territory.

Melbourne has finally surpassed its previous peak, supported by improving affordability and returning population flows, while Darwin's sharp rebound reflects a chronic shortage of listings and high investor demand.

Meanwhile, the regional story has become one of the most remarkable in Australian property history.

Between 2015 and 2025, regional house prices grew 98.8% to $688,000, while national house prices grew only 84.7% to $950,000.

Regional house prices now represent 72% of national prices, up from around 65% historically - the narrowest this gap has ever been.

And the drivers of regional growth aren't what they used to be.

Two powerful engines have driven this transformation: lifestyle migration and the commodity cycle.

Agricultural regions have delivered remarkable returns, with wheat belt areas showing 85% house price growth over the decade.

Mining hubs, particularly in Western Australia and Queensland, have rebounded strongly as the lithium and iron ore sectors revived post-pandemic.

The "median" is lying to you

Here's something that trips up a lot of buyers and investors: the median price figure you see in headlines isn't telling you what you think it's telling you.

Half of all homes sell below the median price. The median is not the entry-level benchmark - it is simply the midpoint of the market.

- Also read:Melbourne property market forecast for 2026 & 2027 | Separating the fundamentals from the sentiment

- Also read:Brisbane Property Market Forecast [2026 & Beyond] – What The Olympics Decade Means for Investors.

- Also read:Sydney property market forecast for 2026 and 2027 | Why the short-term softness is a long-term opportunity

- Also read:Latest Property Price Forecasts. Australian Property Market Outlook 2026-2027: Navigating a Market Correction

- Also read:Everything you need to know about the state of Australia’s property markets in 20 charts – July 2026

First-home buyers typically purchase in the lower half of the market, and as affordability pressures intensify, they are moving even further down the price ladder.

Buyers are swapping land for location, size for access, and houses for apartments.

Unit sales under $750,000 have risen from around 77,000 to nearly 96,000 over the same decade that detached entry-level homes have been disappearing.

In other words, the market is adapting even if affordability broadly hasn't improved.

The national dwelling value-to-income ratio reached 8.2 in September 2025, compared with a 20-year average of 6.8.

It now takes 11 years to save a standard 20% deposit, while around 45% of gross household income is required to service a new mortgage.

Despite all that, buyers are still finding ways in.

What this means for investors

If you're investing, or thinking about it, the fragmented market demands a fragmented strategy.

The old approach of picking a capital city and waiting for the cycle to do the work is increasingly outdated.

Here's what the data is pointing to:

1. The affordable end of the market has genuine structural tailwinds.

Government policy has dramatically lowered the entry barrier for first-home buyers, and that demand isn't going away.

The removal of income caps and the lift in price thresholds under the deposit guarantee scheme have dramatically broadened eligibility and demand is already flowing into the bottom quartile, where affordable houses and units are consistently outpacing the wider market across most cities.

2. Regional markets have matured, but selectivity matters more than ever.

Not all regional markets are created equal.

The commodity-driven markets of WA and Queensland are behaving very differently from the lifestyle markets of coastal NSW or Tasmania.

South Australia now serves as Australia's affordability escape valve, attracting buyers priced out of other states.

3. Supply constraints are a long-term problem and opportunity.

There is currently a shortage of over 200,000 homes in Australia, and the problem is only compounding as we continue to under-deliver.

And this structural undersupply, combined with population growth, is the oldest and most reliable tailwind in property.

The big picture

What Conisbee's K-Turn framework reveals is something important: the market isn't just complex - it's diverging in ways that reward the informed and punish those relying on broad generalisations.

The Australian property "market" is better understood now as dozens of overlapping micro-markets, each responding to its own mix of local supply, buyer demographics, government policy levers and economic conditions.

The Australian housing market is moving forward with far more momentum than most expected a year ago, but also with an unusual degree of uncertainty.

Whether this pace can be sustained will depend heavily on the interest-rate path and how the geopolitical challenges play out.

The investors who'll do best in this environment won't be the ones watching the RBA's every move.

They'll be the ones who understand which market they're in, and why that market specifically is positioned to perform.

That's a very different skill to what worked a decade ago.

And developing it now, while most people are still thinking in broad strokes, is probably the smartest thing a property investor can do.

Ready to find your place in this fragmented market?

If this article has you thinking - good. That's the point.

But thinking about it and actually doing something about it are two very different things.

In a market this fragmented, generic advice won't cut it. You need a strategy that's built around your specific financial situation, your goals, and the right opportunities for right now — not a one-size-fits-all approach recycled from a previous cycle.

That's exactly what the team at Metropole does.

Whether you're looking to buy your first investment property, grow an existing portfolio, or simply make sense of where the opportunities actually are in today's splintered market, a conversation with one of Metropole's experienced Wealth Strategists could be the most valuable time you spend this year.

Click here to book a complimentary consultation with a Metropole Wealth Strategist and get a clear, independent plan to build long-term wealth through property in the markets that make sense for you.