Key takeaways

Headlines exaggerate short-term weakness.

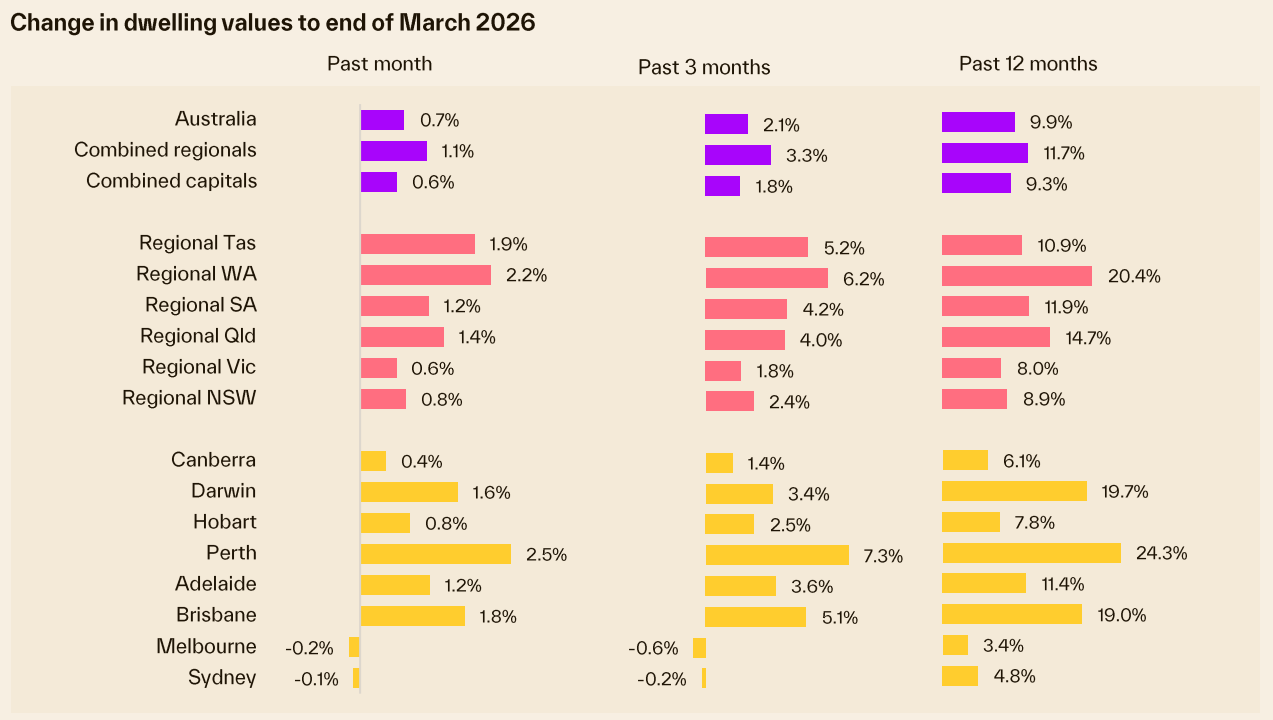

Melbourne was labelled a “basket case,” yet many suburbs delivered strong price and rental growth. Savvy investors saw relative affordability as an opportunity rather than a problem.

Property crashes need forced sellers and weak demand. Despite constant crash predictions, strong employment and housing shortages kept prices rising. National values actually increased strongly during 2025.

Rate cuts don’t solve affordability. Lower interest rates increase borrowing capacity, but in undersupplied markets, this often pushes prices higher. Monetary policy can boost demand, but it doesn’t increase housing supply.

Australia doesn’t have one property market. Even with falling interest rates, performance varied widely between cities and suburbs. Local factors like jobs, population growth, and supply shortages drive results.

Long-term fundamentals matter more than forecasts. Media predictions often ignore supply shortages, credit conditions, and employment trends. Investors who focus on fundamentals and history make better long-term decisions than those chasing headlines.

Every year, the media confidently predicts what’s ahead for our property markets.

And every year, when we look back with the benefit of hindsight, a very different story emerges.

Now that 2025 is well behind us, it’s time to check the scoreboard.

Not to criticise for the sake of it, but because if you’re a serious investor, you can’t afford to base your long-term decisions on short-term headlines.

Here are 10 things the media got wrong about Australia’s property markets last year - in 2025, and what you should learn from it.

1. "Melbourne property is a basket case"

If you read the headlines, you’d think Melbourne was a ghost town for investors.

While it was the "laggard" among the big capitals and overall values rose roughly 4.5% over the years, a number of selected suburbs show double-digit capital growth and very strong rental growth.

By the way… at Metropole, we purchased many investment properties for our clients in these suburbs, which experienced significant growth.

The media focused on the exit of some "Mum and Dad" investors due to land tax changes and challenging tenancy reforms, but they overlooked the long-term value play.

Savvy investors saw Melbourne’s relative "affordability" compared to Perth, Sydney and Brisbane as a buying opportunity, not a reason to flee.

In fact, investor lending for Melbourne rose considerably last year.

2. “The property market is about to crash”

There’s always a crash narrative floating around.

In 2025, it was the "18-year cycle" and the "interest rate cliff" (again).

More recently, it has to do with the war in the Middle East.

The media loves the word "crash" because it sells papers or gets clicks on websites, but they forget that a “crash” requires forced selling and no one wanting to buy property.

With unemployment remaining low and a massive structural housing undersupply, there were simply no sellers forced to offload their homes at a discount.

Instead of a crash, we saw a fragmented market, with Cotality's Home Value Index surging 8.6 per cent in 2025, adding roughly $71,400 to the national median dwelling value.

It was the strongest calendar year gain in home values since 2021, when the market spiked 24.5 per cent at a time of record-low interest rates and record-high levels of buying activity.

The lesson for investors is that property markets are driven by supply and demand, credit availability, and strong employment, not headlines.

3. “Rate cuts will quickly fix affordability”

When the RBA began cutting rates in 2025, the narrative quickly shifted to “relief is coming”.

And yes, lower rates improved borrowing capacity at the margin.

But affordability didn’t magically improve, because when borrowing capacity rises in an undersupplied market, buyers compete harder, and that additional capacity often flows straight into higher prices.

Rate cuts change how much buyers can borrow. They don’t create new land, new dwellings, or new infrastructure.

So, affordability didn’t improve last year. In fact, renewed competition just pushed prices higher.

The media confused monetary easing with structural housing reform. They are very different things.

4. “Once rates fall, the market will boom everywhere”

This was another oversimplification.

The rate cuts in 2025 helped support confidence and demand, but performance was highly uneven across the country.

Some markets surged strongly. Others delivered modest gains. And a few lagged.

That’s because interest rates set the broad environment, but local fundamentals determine outcomes.

Employment growth, population inflows, supply pipelines, and relative affordability all played a much bigger role in explaining performance differences than “rates are down”.

Tip: There is no single Australian property market. There are hundreds of sub-markets, each behaving differently.

5. “Rents can't keep rising.”

Throughout 2025, there were regular stories suggesting rental growth would ease because, for a few years, it had outpaced wage growth, leading to affordability pressures.

It’s true that rental growth slowed compared to the extraordinary post-pandemic surge, but rents continued rising overall. In fact, many markets finished the year at record highs.

Vacancy rates remained tight in most capitals, particularly in well-located suburbs close to employment hubs and lifestyle amenities.

The media again confused slowing growth with falling rents. They are not the same thing.

6. “Foreign buyers are driving price growth”

Whenever property prices go up, the media looks for a scapegoat, often pointing to foreign investors.

But the data in 2025 showed that price growth was almost entirely driven by domestic factors: record-breaking migration (increasing demand) and a chronic lack of new supply.

Foreign demand may play a role at the margins, particularly in specific segments, but broad-based national price growth is overwhelmingly driven by local credit conditions and domestic demand.

Blaming foreign buyers is politically convenient. It’s rarely analytically accurate.

7. "The Government will fix the housing shortage"

We heard a lot of big promises about the National Housing Accord and building 1.2 million homes.

- Also read:Melbourne property market forecast for 2026 & 2027 | Separating the fundamentals from the sentiment

- Also read:Brisbane Property Market Forecast [2026 & Beyond] – What The Olympics Decade Means for Investors.

- Also read:Sydney property market forecast for 2026 and 2027 | Why the short-term softness is a long-term opportunity

- Also read:Latest Property Price Forecasts. Australian Property Market Outlook 2026-2027: Navigating a Market Correction

- Also read:Everything you need to know about the state of Australia’s property markets in 20 charts – July 2026

The media dutifully reported these targets as "solutions."

However, reality hit hard: construction completions in 2025 remained nearly 30% below those targets.

Of course, the government was never going to build any of these houses.

It was going to be private builders and developers, and labour shortages and rising material costs meant we couldn't build our way out of the crisis, keeping the floor firmly under established property prices.

8. “We’re heading into a recession - so property will fall”

"Recession" was a buzzword for the first half of 2025.

News cycles were dominated by "recession watch" segments.

Yes, households felt pressure. Yes, per-capita outcomes were soft.

But the broader economy continued to show incredible resilience, and unemployment remained at near historic lows.

This was supported by strong government spending, high commodity prices, and a robust labour market.

We managed to avoid a technical recession, leaving those who sold their assets in "fear" of a downturn looking on from the outside.

The media often conflates economic discomfort with systemic collapse. They are not the same thing.

Note: Of course, we're once again hearing talk about recession, as our economy and housing markets face multiple challenges, many of them coming from overseas. Don't let the Property Pessimist scare you!

9. “The hot markets have peaked - it’s too late”

Whenever a market runs strongly, headlines shift from optimism to warning.

In 2025, many property markets that had already experienced strong growth were repeatedly declared “done”.

Yet several of those markets continued to deliver solid gains.

Markets don’t turn because they’re “due”. They turn when fundamentals shift.

As long as demand exceeds supply and employment remains strong, momentum can persist longer than commentators anticipate.

Trying to pick tops based on sentiment is a poor strategy.

Buying quality assets that outperform through cycles is a much better one.

Just look at how property values have performed over the last year.

10."The 18-year property cycle predicts a 2026 collapse"

By late 2025, the media started priming everyone for a 2026 disaster based on "cycle theories."

They treated the property market like it runs on a clock.

As I’ve always said, markets run on people, credit, and confidence, not numerology.

By focusing on a "magical year" for a crash, the media ignored the actual mechanics of the market, causing many to miss out on the double digit growthseen in powerhouse markets like Perth and Brisbane.

The bigger lesson for serious investors

If you relied on headlines in 2025, you would have been cautious at exactly the wrong times.

The media tends to:

- Overemphasise short-term movements

- Confuse slowing growth with falling prices

- Treat Australia as one homogenous market

- Underestimate the power of credit and employment

- Underappreciate the structural supply shortage

Tip: As an experienced investor, you already know that property is a long-term game, my take-home lesson for you is: Read fewer forecasts, but more history

You see, many years ago I made a goal to read more history and fewer forecasts, and it made a big difference to how I invest.

When you focus on what never changes, you stop trying to predict uncertain events and spend more time understanding timeless behaviour.

In a world full of noise, clarity is your competitive advantage.

If you can separate sentiment from structure, you’ll continue to build wealth - regardless of what the next set of headlines predicts.

I know many people are worried at present.

But think about it …

If you sold your assets during the Iraq War… the GFC… or COVID… you would have been wrong every single time.

This is the fifth big global economic shock in less than two decades.

While we may experience fuel shortages, overall our economy is well situated and well buffered to ride through it

Two things matter most here: how long the war lasts, and also how long it takes to get the global economy back on track after it ends.

Note: What feels like the end of the world is often the beginning of the next wealth cycle.

Having invested for over 50 years, I have realised that every crisis follows the same script:

- Shock

- Panic

- Media exaggeration

- Policy response - we've already received this

- Recovery

- New highs

If you are worried, please remember...

- War resolves (they always do)

- Inflation stabilises

- Rates eventually fall

- Demand returns

- And property values rise to new highs.