Key takeaways

In just two decades, the cost of homeownership has soared disproportionately compared to income growth.

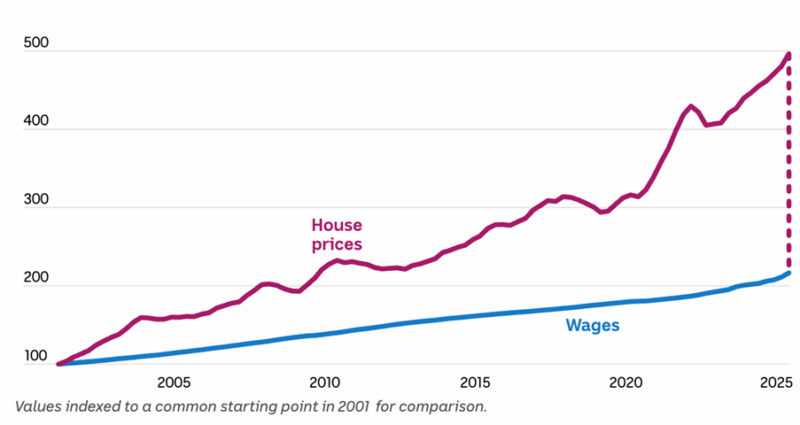

While average incomes have doubled since 2001, house prices in many parts of Australia have increased fivefold. This has broken the long-held social contract that hard work and saving would eventually lead to owning a home.

For younger Australians, even those on good incomes, the path to homeownership is increasingly unattainable.

Australia’s housing crisis isn’t the result of one bad policy or a short-term shock, but decades of compounding problems.

Even with optimistic assumptions like stable wage growth, slow property price growth, and perfect policy implementation, housing affordability likely won’t normalise until the 2040s or 2050s.

To fix the housing crisis, Australia must treat housing as essential infrastructure, not just a wealth-building vehicle or political football.

House prices have always been a talking point in Australia, but lately the conversation has shifted from concern to alarm. And for good reason.

Tom Crowley explained this well in a recent article on ABC. He said…

Think back to 2001. A typical nurse-and-electrician couple could save for around six years and buy a modest suburban home.

That same home - adjusted for inflation - might have cost the equivalent of $300,000 at the time.

Fast forward to today. Their child is now a teacher, partnered with someone in a similar middle-income role.

They’ve saved for six years too - in fact, more than double what their parents saved in real terms.

Yet that same home is now valued at around $1.5 million.

Incomes may have doubled since the early 2000s - but house prices have quintupled.

That tells you everything you need to know about the depth of Australia’s housing affordability issue.

Source: abc.net.au

The real shift: a social contract broken

For generations, we had an unwritten promise in Australia: If you worked hard, saved consistently, and lived within your means, home ownership, and the wealth stability it brought, was within your grasp.

Unfortunately, that promise has slowly eroded and now we're facing the uncomfortable truth that for many Australians, even those with good incomes, homeownership is no longer guaranteed.

The ABC analysis highlights what many of us have been warning about for years - the house-price-to-income ratio has stretched so far that it’s reshaping life decisions.

Couples are delaying children, living with parents longer, or taking on dangerously high levels of debt just to get a foot on the ladder.

How we got here: a perfect storm 20 years in the making

The blowout in affordability didn’t come from a single bad policy or a short-term economic shock.

According to Crowley, it accumulated over decades through overlapping forces.

Here are the five biggest:

1. Chronic undersupply

For more than a decade, Australia simply hasn’t built enough new dwellings. And where supply has increased, it's often in the wrong locations or in high-rise formats that don’t meet family needs.

2. Demand-boosting incentives

First-home buyer grants, stamp duty discounts, and low-deposit schemes are all well-meaning, but they all unintentionally add more buying power to a market with too few homes.

And the predictable result is that property prices rise further.

3. Borrowing capacity shocks

Lower interest rates (even the expectation of them) allow buyers to borrow more, pushing prices higher. Even now, with higher rates, constrained supply is preventing prices from easing.

4. Planning bottlenecks

Planning systems are slow, complex, and expensive. Reform efforts have been announced for years, but practical outcomes have lagged far behind the rhetoric.

5. Migration and population growth

Australia relies heavily on migration for economic growth. But population growth has far outpaced new housing construction - a trend reinforced through the 2020s and visible again today.

- Also read:Melbourne property market forecast for 2026 & 2027 | Separating the fundamentals from the sentiment

- Also read:Brisbane Property Market Forecast [2026 & Beyond] – What The Olympics Decade Means for Investors.

- Also read:Sydney property market forecast for 2026 and 2027 | Why the short-term softness is a long-term opportunity

- Also read:Latest Property Price Forecasts. Australian Property Market Outlook 2026-2027: Navigating a Market Correction

- Also read:Everything you need to know about the state of Australia’s property markets in 20 charts – July 2026

Put simply: demand surged, supply limped, and affordability was the casualty.

Why fixing this will take decades

There’s no shortage of political announcements - things like building 1.2 million homes or delivering a "big build".

But the reality is sobering.

Construction capacity is limited. Labour shortages persist. Developers face tight finance conditions. Councils resist density. Costs remain elevated. And approval timelines remain stubbornly slow.

Even if we started perfect policy implementation tomorrow, affordability doesn’t snap back in two years… or five… or maybe even ten.

ABC modelling suggests that even under optimistic conditions - where house prices grow slowly, and wages rise steadily - affordability may not look “normal” again until the 2040s or 2050s.

That's two decades away!

And that’s assuming nothing derails the plan - no rate shocks, no building cost spikes, no policy reversals, no recession.

So where does that leave us?

1. Renting will be a long-term reality for many Australians.

And it is likely that the government will continue to protect tenants with increasing tenant friendly legislation.

2. Wealth inequality will widen without intervention.

Housing remains the biggest driver of family wealth in Australia.

Owners will see their equity grow. Non-owners risk falling further behind.

3. Investors play a critical role.

Despite the political finger-pointing, private investors supply over 90 percent of rental homes.

In a time of chronic undersupply, discouraging investors through over-regulation or punitive taxes only makes the crisis worse.

4. The opportunity for strategic investors is significant.

Periods of undersupply have historically been the most rewarding for countercyclical, long-term property investors.

But the winners will be those who buy the right assets: investment-grade properties in locations with strong income, population, and infrastructure growth.

What needs to change

To genuinely address the crisis, Australia needs a mindset shift across both policy and society.

Crowley makes the following suggestions:

- Rebuild supply, not demand

More homes, especially family-suitable dwellings and well-located medium density. - Streamline planning approvals

Cut red tape, standardise processes, and incentivise councils to approve more homes. - Support build-to-rent and community housing

These models are globally proven to stabilise rental markets. - Stop using housing as a political sugar hit

Short-term demand-side handouts do more harm than good. - Reframe housing as essential infrastructure

Like roads or hospitals, housing supports national productivity. Treat it that way.

The bottom line

Australia’s housing crisis wasn’t created overnight, and it won’t be fixed overnight.

It’s the accumulated result of decades of undersupply, structural policy choices, and cultural expectations that no longer align with economic reality.

But acknowledging the scale of the challenge is the first step toward addressing it.

For investors, this environment continues to present opportunities - provided you take a long-term view and avoid the speculative noise.

For policymakers, it’s a moment to be bold.

And for younger Australians, while the mountain is steeper than ever, with the right guidance, strategy, discipline, and timing, it’s still possible to climb it.

Remember that last year, in 2025, over 110,000 new first-home buyers entered the market, which was around 20% of all property transactions.