Key takeaways

The ultimate aim isn’t just owning a few properties – it’s achieving financial freedom and choice later in life.

Your “end game” portfolio should allow you to step away from the workforce and live life on your own terms.

Success isn’t about building the biggest portfolio, but the right portfolio.

Plan early for the “end game” – whether that’s living off cash flow, selling, downsizing, or living off equity.

Ultimately, property investing isn’t about property at all – it’s about creating financial freedom and choice.

Most property investors start out with one simple goal – financial freedom.

But the question I often get asked is: “How do I actually live off my property portfolio when the time comes?”

The truth is, owning a few properties isn’t enough.

To achieve financial freedom, you need to build a substantial, diversified, and well-structured asset base that will give you choices later in life.

What should the end game look like?

At some point, you’ll step away from the workforce.

You might call it retirement, or you may simply want the freedom to choose how you spend your days - travelling, pursuing hobbies, giving back, or spending more time with family.

Whatever your vision looks like, the ultimate purpose of building a property portfolio is to give you choices.

When you reach that stage, here’s what I’d like you to have in place:

- Your home, debt-free. I don’t want you to carry non-tax-deductible debt into retirement. Your home should be a financial and emotional anchor, free of the bank’s involvement.

- A portfolio of quality residential properties with a comfortably low loan-to-value ratio, generating reliable cash flow.

- Additional income-producing assets, such as shares, ETFs, or even commercial property, to provide diversification and resilience.

- Superannuation as another pillar of your financial security.

Now we can’t predict exactly how the rules of the game will change over time.

Governments will come and go, interest rates will fluctuate, taxation policies will evolve, and who knows what age you’ll actually be able to access your superannuation.

Even the availability of bank finance in later life remains uncertain.

That’s why the key is to build a substantial, diversified asset base held in a flexible ownership structure.

Over the years, I’ve found that most investors move through four stages:

- Education stage - learning the rules, strategies, and mindset of successful investing.

- Accumulation stage - aggressively building your asset base through leverage and smart property purchases.

- Transition stage - lowering your loan-to-value ratio and shifting focus toward cash flow.

- Living off your portfolio - the point where your property becomes a cash machine that funds your lifestyle.

The transition to cash flow

So, how do you make that all-important transition from growth to cash flow?

There's no right way, as everyone's circumstances are different, but here are a couple of options.

1. Slow down the pace of growth

Once your portfolio is substantial, resist the urge to keep endlessly accumulating.

Instead, let time and capital growth do the heavy lifting.

By not refinancing to buy more, your loan-to-value ratio naturally falls.

Lower debt means higher net rental income, which turns into the passive income that fuels your lifestyle.

2. Convert to principal-and-interest loans

During your accumulation stage, interest-only loans help you maximise borrowing power and flexibility.

But in the cash flow stage, switching some loans to principal-and-interest allows your tenants to help retire your debt.

Over time, this strengthens your cash position - even if the principal repayments aren’t tax-deductible.

3. Consider commercial property

Residential property is a growth play.

Commercial property, by contrast, usually delivers stronger yields but less capital appreciation, since rents often rise only in line with CPI.

Adding one or two commercial assets to a well-established portfolio can boost cash flow without derailing your growth strategy.

4. Use superannuation or savings strategically

Once you reach preservation age, you may choose, with advice, to sell some assets in your SMSF.

Under current rules, gains in the pension phase are tax-free, and you can use proceeds to retire external debt or rebalance your income streams.

5. Redevelop to manufacture growth and income

If one of your properties has redevelopment potential, you might unlock hidden value.

By subdividing or developing, you can either sell surplus dwellings to repay debt or retain them to enjoy higher rental returns from the same landholding.

6. Sell strategically

While I generally advocate holding for the long term, sometimes the right move is to sell one or two properties to reduce debt and increase income.

The key is to weigh the impact of capital gains tax and structure your sale wisely - for example, within an SMSF during pension phase, where gains may be tax-free.

7. Living off equity - my favourite strategy:

Personally, I prefer not to sell at all.

Instead, I’ve lived off the growing equity in my portfolio.

By carefully drawing on equity, I’ve been able to retain high-growth assets, avoid triggering capital gains tax, and still generate the income I need.

- Also read:This week’s Australian Property Market Update – Latest Data, State by State June 23rd 2026

- Also read:Everything you need to know about the state of Australia’s property markets in 20 charts – June 2026

- Also read:Melbourne property market forecast for 2026 & 2027 | Why the opportunity is bigger than it looks

- Also read:Sydney property market forecast for 2026 and 2027 | Why the short-term softness is a long-term opportunity

- Also read:Latest Property Price Forecasts. Australian Property Market Outlook 2026: Where To Now After The Rate Rise & Budget Changes.

It’s a way of having your cake and eating it too - enjoying today while preserving tomorrow for the future.

Note: This is the “end game” - building a life where your money works harder than you do, where your properties provide not just wealth on paper but freedom in practice.

Living off equity – how it works

Here’s the idea: instead of selling properties, you draw on the equity they’ve created as a tax-free way of generating income.

You see, when you sell a property, you trigger capital gains tax. But when you borrow against the equity in a property, the funds you access aren’t considered taxable income.

That means you can keep your high-growth assets working for you while still enjoying the cash flow you need to fund your lifestyle.

It’s like having your cake and eating it too. Of course, the interest paid on this strategy is not tax deductible, as the purpose of the borrowing is not for investment.

An example

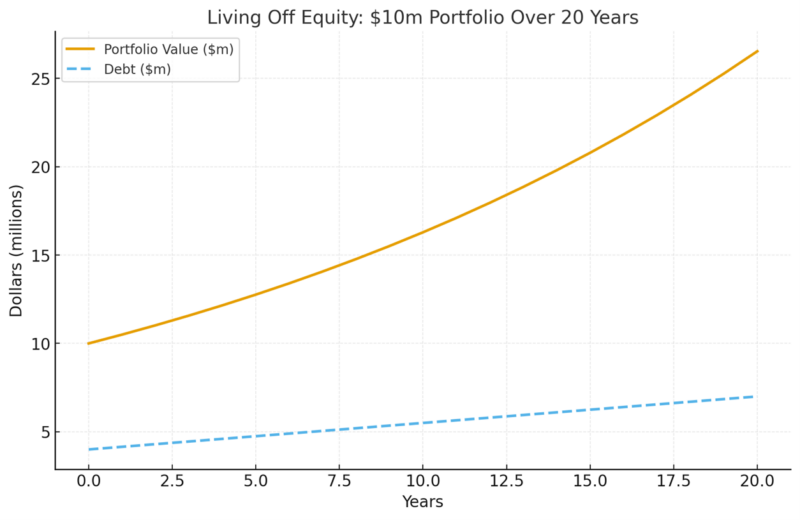

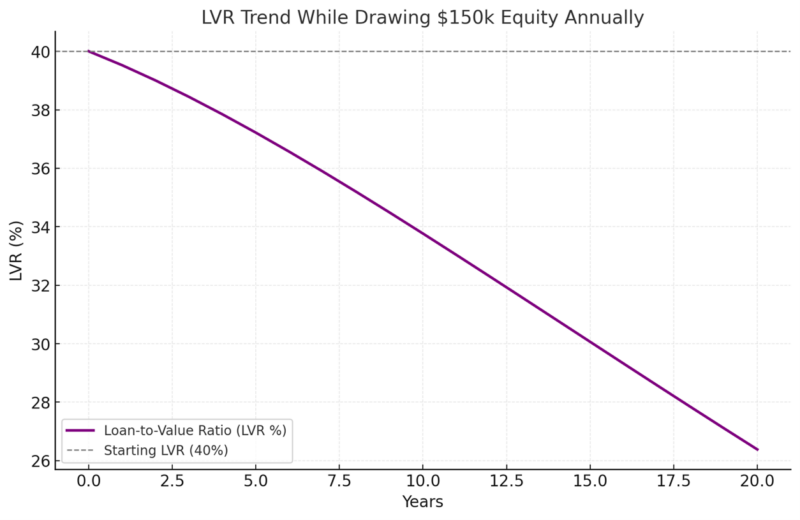

Let’s say you’ve built a $10 million portfolio of well-located properties.

Over time, you’ve reduced your debt to $4 million – a conservative 40% LVR.

At this stage, your properties might generate around $150,000 per year in rental income after expenses and mortgage costs.

That’s a solid income; but perhaps not enough to fund the lifestyle you aspire to.

So, you supplement it with an annual equity drawdown of $150,000 from the bank.

Now look at what happens:

- Your portfolio is still compounding in value. At just 5% annual growth, your $10 million portfolio increases by $500,000 each year.

- You’re only drawing $150,000 of that increase each year.

- Your LVR hardly changes, because the portfolio’s growth far outpaces the equity you’re accessing.

So in this example, you’d enjoy $300,000 per year in lifestyle income – $150,000 from rents plus $150,000 from equity – while still holding onto your entire high-growth portfolio.

Over time, you may eventually rebalance by selling one property, downsizing, or using superannuation to reduce debt.

However, for a significant period – often a decade or more – this approach allows you to live abundantly while your wealth continues to compound in the background.

Why this strategy works best with a strong foundation

Of course, this strategy only works if you’ve built a large enough portfolio of investment-grade properties to begin with.

You need the right assets in the right locations, and you need to manage your borrowings so banks are comfortable letting you access that equity.

That’s why I always tell investors: focus on quality over quantity.

The real wealth comes from well-located, high-demand assets that will continue to appreciate strongly over the long term.

Now, you may be wondering: “That all sounds great, Michael, but will the banks still let me live off equity?”

The truth is, in the old days it was easy.

You could walk into a bank, get a low-doc loan, and as long as your properties were increasing in value, it was smooth sailing. Today it’s harder – much harder.

But it’s still very doable if you own the right type of property and you’ve lowered your loan-to-value ratio enough to demonstrate strong serviceability.

Of course, you can’t achieve this overnight.

It takes years of building a substantial asset base, reducing your LVR, and using the power of leverage, compounding, and time.

But remember that if you follow this model, you still are earning income - in fact you’re getting it from a number of sources:

1. Capital growth is passive income – but banks don’t count it.

Yes, your properties may be growing by hundreds of thousands of dollars each year, but lenders won’t recognise this growth as “income.” The good news is that you don’t pay tax on it either.

2. Rental income is the key.

This is why I recommend lowering your LVR so your rental income comfortably covers your property expenses and mortgage repayments and have sufficient surplus income so that the banks are happy to extend more credit.

3. Diversified income streams.

If you can demonstrate additional income from shares, dividends, or superannuation, you’ll be in a stronger position.

At the time of writing, banks are conservative.

They’re not prepared to refinance a portfolio based purely on the prospect of capital growth.

What this means is that by the time you reach the “living off equity” stage, you’ll need to have shifted your strategy as I’ve outlined and turned your portfolio into a true Cash Machine, giving you the financial freedom to live life on your terms.

Final thoughts

The goal isn’t to build the biggest portfolio. It’s to build the right portfolio – one that will eventually fund the life you want.

Whether you choose to live off cash flow, downsize, sell strategically, or (like me) live off equity, the important thing is to plan for the end game early.

After all, property investing isn’t really about property. It’s about creating the financial freedom to live life on your terms.