Key takeaways

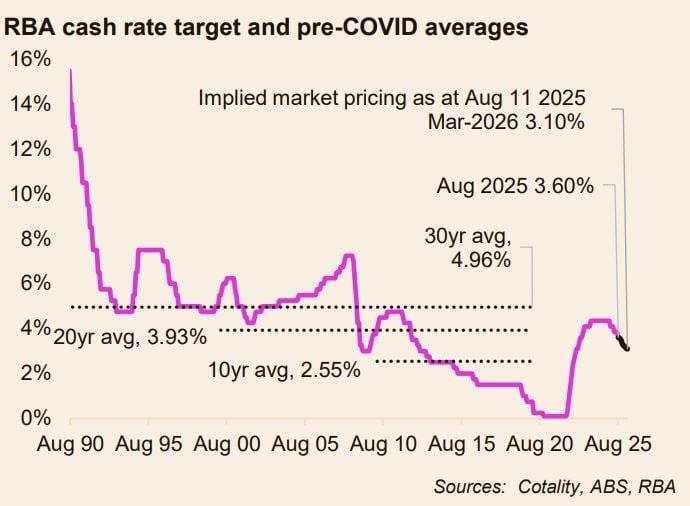

This is the third cut in the current easing cycle, in what was always expected to be cautious and gradual.

The move follows a surprise July ‘hold’ decision, when the RBA paused to assess inflation and labour market trends.

There are 3 more RBA meeting dates this year: Sep 30, Nov 4, Dec 9.

The futures market sees cash rate at 3.2% by year-end and 3.1% by March 2026, implying 1–2 more cuts in the next seven months.

Another cut could boost demand further, but affordability constraints will keep gains contained.

Today’s rate decision marks the third cut in what was always expected to be a cautious and gradual easing path.

This decision follows a surprise ‘hold’ from the Reserve Bank of Australia (RBA) in July, where the board adopted a ‘wait and see’ approach regarding inflation and job markets.

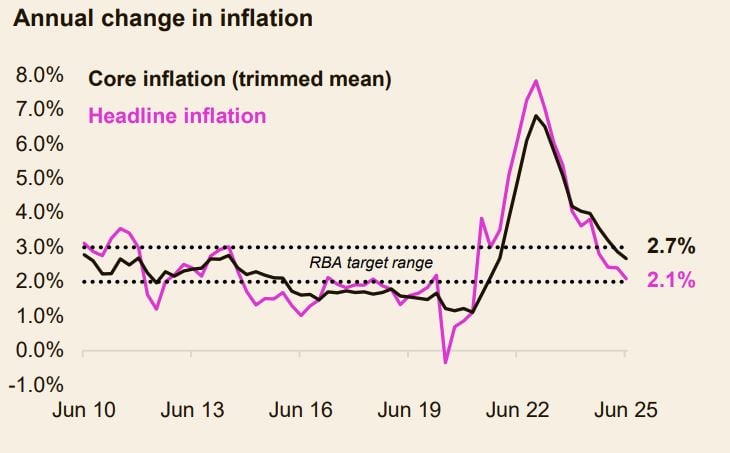

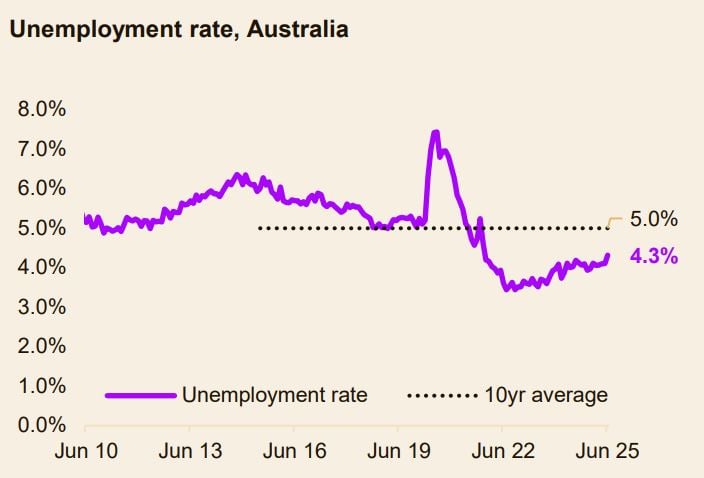

Since the July meeting, core inflation has reduced to 2.7%, the lowest in three and a half years, and labour markets have loosened with the unemployment rate rising to 4.3%, the highest since November 2021.

The rate cut is a net positive for housing markets, supporting demand through increased borrowing capacity and loan serviceability, and is likely to provide a boost to confidence.

Earlier rate cuts have supported a renewed and broad-based positive trend in housing values.

For existing borrowers, if lenders pass on the cut in full, the average variable mortgage rate is expected to reduce to around 5.5%, saving approximately $120 per month on a $750,000 home loan.

Compared to January, repayments on the same loan amount are likely to have reduced by roughly $370 per month.

It is important to keep the context in mind. Although rates are coming down, they are doing so from a high base, and monetary policy settings remain in restrictive territory.

Even if interest rates decrease by another 50 basis points to 3.1%, the cash rate would only be around neutral territory.

- Also read:Australia’s Building Crisis Is Getting Worse – What It Means for Property Investors | Property Insiders

- Also read:Australian housing market update | June 2026

- Also read:This week’s Australian Property Market Update – Latest Data, State by State June 16th 2026

- Also read:Melbourne housing market update | June 2026

- Also read:National Vacancy Rate Holds at 1.2%| SQM Research

Prior to the pandemic, the decade average cash rate was just 2.55%.

For prospective buyers, a reduction in borrowing costs may encourage more would-be purchasers to enter the market, boosting transaction activity.

However, first home buyers still face significant deposit hurdles due to high (and rising) housing prices and recent cost of living pressures that have depleted savings and continue to weigh on expenses for many households.

Overall, we expect housing markets to respond positively to the rate drop, which is occurring against a backdrop of low supply.

However, stretched housing affordability and prudent lending standards are likely to temper the upswing.

Looking ahead, there are only three more opportunities this year for the RBA to cut rates: Sep 30, Nov 4 and Dec 9.

Futures market pricing puts the cash rate at 3.2% by year’s end and 3.1% by March next year implying we could see one or two more rate cuts over the next seven months.

Another rate cut could further energise housing demand, though affordability pressures should keep gains in check.