Key takeaways

The counterintuitive solution to Australia’s housing crisis is higher house prices.

Without prices rising to meet construction costs, developers won’t build, and supply will keep shrinking.

More supply isn’t the solution unless it’s viable to build.

Rising property prices are the only real fix to Australia’s housing crisis.

For existing owners and investors, this environment points to ongoing capital growth and rental income gains.

Have you ever wondered what the real fix for Australia’s housing crisis might look like?

Well, buckle up because it might not be what you expect.

Here’s a bold assertion that’s bound to stir up some debate: the only way to truly resolve our housing crisis is for house prices to keep rising.

Yes, you heard that right.

At first glance, it sounds counterintuitive, maybe even a little controversial, doesn’t it?

But when you look at the numbers, the costs, and the dynamics of our housing system, the uncomfortable truth emerges – without rising prices, we simply won’t get the new housing we desperately need.

We need more homes, but fewer are being built

Australia is currently experiencing a rental and affordability crisis.

Population growth is surging, vacancy rates are at record lows, and rents are climbing at a pace we haven’t seen in decades.

And yet, despite this overwhelming demand, the very homes we need most – new apartments – aren’t being built.

According to international property consultants CBRE, Australia will complete just 52,500 new apartments in 2025, down from more than 64,000 last year.

That’s 30,000 fewer homes than forecast only two years ago.

The reason is simple: the economics don’t stack up.

Developers can’t sell apartments at prices high enough to cover today’s construction costs.

Feasibilities remain about 20% underwater, which means that if developers build now, they’ll lose money.

Why the numbers don’t work

The gap between what it costs to build and what people can pay has never been wider.

- Construction costs jumped 38% in just three years to mid-2023, and even though the increasing construction costs have softened since then, they're still rising considerably faster than inflation.

- Land costs and government levies remain high.

- Banks still demand 70–75% of presales before financing, but buyers are reluctant to commit off-the-plan.

- Developers traditionally expect 20% margins – margins that are impossible to achieve right now.

Even looking out to 2030, CBRE expects total completions to undershoot earlier forecasts by around 50,000 apartments.

That’s a massive shortfall at a time when demand is only intensifying.

Demand is surging at the same time

Yet demand isn’t slowing down – it’s accelerating.

- Also read:Latest Property Price Forecasts. Australian Property Market Outlook 2026: Where To Now After The Rate Rise & Budget Changes.

- Also read:Melbourne property market forecast for 2026 & 2027 | Why the opportunity is bigger than it looks

- Also read:Sydney property market forecast for 2026 and 2027 | Why the short-term softness is a long-term opportunity

- Also read:Brisbane Property Market Forecast [2026 & Beyond] – What The Olympics Decade Means for Investors.

- Also read:This week’s Australian Property Market Update – Latest Data, State by State May 26th 2026

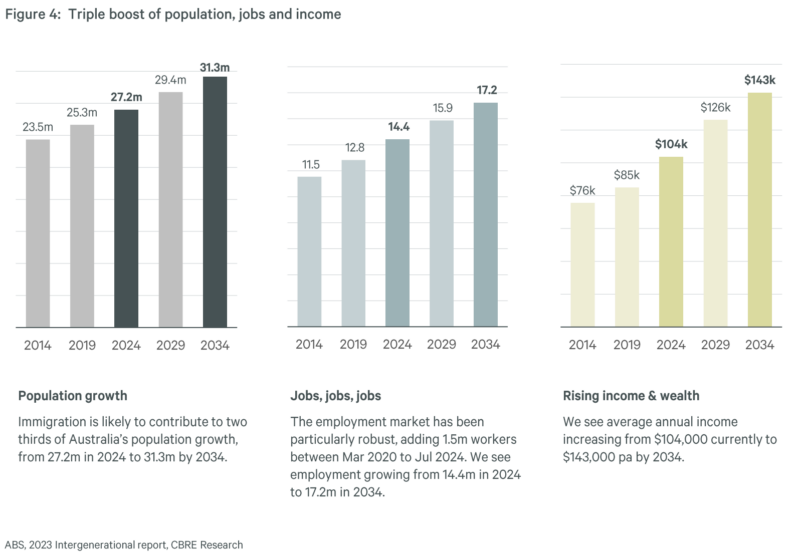

- Population: Immigration will add over 2 million people by 2030, mostly into Sydney, Melbourne, and Brisbane

- Incomes: Household incomes are projected to rise from $110,000 to $140,000 by 2030, boosting borrowing power.

- Rents: Median apartment rents are tipped to grow another 24% by 2030, pushing Sydney two-bedders past $1,000 a week

- Vacancy rates: Already at a record-low 1.1%, they’re forecast to fall further toward 1.0%

Put simply, more people with more income are chasing fewer homes.

Source: CBRE

Why developers aren’t building

You’d think that with so much demand, developers would be scrambling to build. But the system is broken in several ways.

- High costs: Materials, trades, and land remain expensive.

- Financing barriers: Presale hurdles lock up new projects before they even start.

- Profitability: Traditional margins of 20% are impossible.

- Government charges: Taxes and levies add another layer that tips projects over the edge.

Fact is, this isn’t the pre-pandemic market anymore. Trade-offs will be needed: banks may have to relax financing requirements, governments may need to defer charges, and developers may need to accept slimmer returns

But even with compromise, the economics still demand one thing – higher sale prices.

The geography of the shortfall

The supply gap isn’t evenly spread across Australia – but every major city faces challenges according to CBRE:

- Sydney: Deliveries will average 17,000 apartments per year from 2025–30, while demand exceeds 20,000 annually. Vacancy could fall to 1.2%.

- Melbourne: Supply will average just 30,000 per year, 25% below Sydney, despite similar demand

- Brisbane: Delivery will average 6,000 fewer apartments annually than required

So no matter where you look, the shortage is baked in.

What this means for investors

If you’re an investor, the message is clear.

- Rents will keep rising: Scarcity guarantees upward pressure.

- New apartments will command premiums: New stock already rents for 10–20% more than older stock and buyers also pay extra for newly built units .

- Established apartments will gain value: As replacement costs climb, established apartments look cheaper by comparison.

- Countercyclical builders will win: Developers who can push through now will have stock ready by 2027–28, when demand is still surging but supply is tight.

The surprising solution: prices must rise

And this brings us back to the uncomfortable truth.

Our housing system is market-led. Developers won’t build unless it’s profitable. And right now, it isn’t.

So what’s the solution? Prices must rise.

Only when apartment values climb closer to construction costs will more projects stack up. Only then will banks finance them, developers commit, and builders break ground.

It’s a bitter pill, because higher prices make affordability worse in the short term. But without it, supply will keep shrinking – and the crisis will get worse.

The bottom line

The surprising solution to our housing crisis isn’t more supply because, at current economics, we simply won’t build enough.

Instead, the only way to unlock more supply is for prices to rise, closing the gap between costs and values.

That’s bad news for affordability but good news for those who already own property.

For investors, it means scarcity and rising prices will continue to fuel capital growth and rental returns throughout this decade.