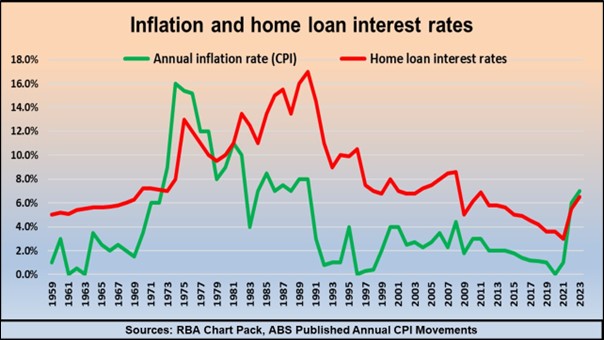

The lag in interest rate rises shows how the Reserve Bank has reacted to changes in inflation rather than trying to anticipate them – except for the last nine rate rises.

This time around, interest rate rises have coincided with increases in inflation.

- Also read:July Home Prices Sharply Down as Winter Freeze Bites | Latest Property Market Stats

- Also read:Melbourne property market forecast for 2026 & 2027 | Separating the fundamentals from the sentiment

- Also read:53 years of valid reasons not to invest

- Also read:Brisbane Property Market Forecast [2026 & Beyond] – What The Olympics Decade Means for Investors.

- Also read:Sydney property market forecast for 2026 and 2027 | Why the short-term softness is a long-term opportunity

This could mean that the bank believes that interest rates are far too low, or it may be that the RBA expects inflation to rise more quickly than previously anticipated, or it could signify both.

The graph also demonstrates that since the nineteen seventies, home loan interest rates have always been higher than the prevailing inflation rate – except for right now.

This also means that interest rates may rise further, at least until the rate of inflation reduces.