APRA - the financial regulator for the big banks - has introduced a policy initiative designed to reduce perceived emerging risky lending.

APRA is concerned that because of our recent strong housing market activity, home loan sizes are increasing faster than incomes, potentially increasing the debt load for new borrowers.

APRA is concerned that because of our recent strong housing market activity, home loan sizes are increasing faster than incomes, potentially increasing the debt load for new borrowers.

This could become an issue for banks if official interest rates rise – although the RBA has consistently stipulated that this is unlikely to happen until at least 2024.

Reflecting these concerns, APRA has instructed the big banks to raise the repayment risk buffer from 2.5% to 3% above the headline rate secured by new borrowers.

The tightening of lending conditions will impact all new borrowers regardless of the “risk” circumstances of local housing markets.

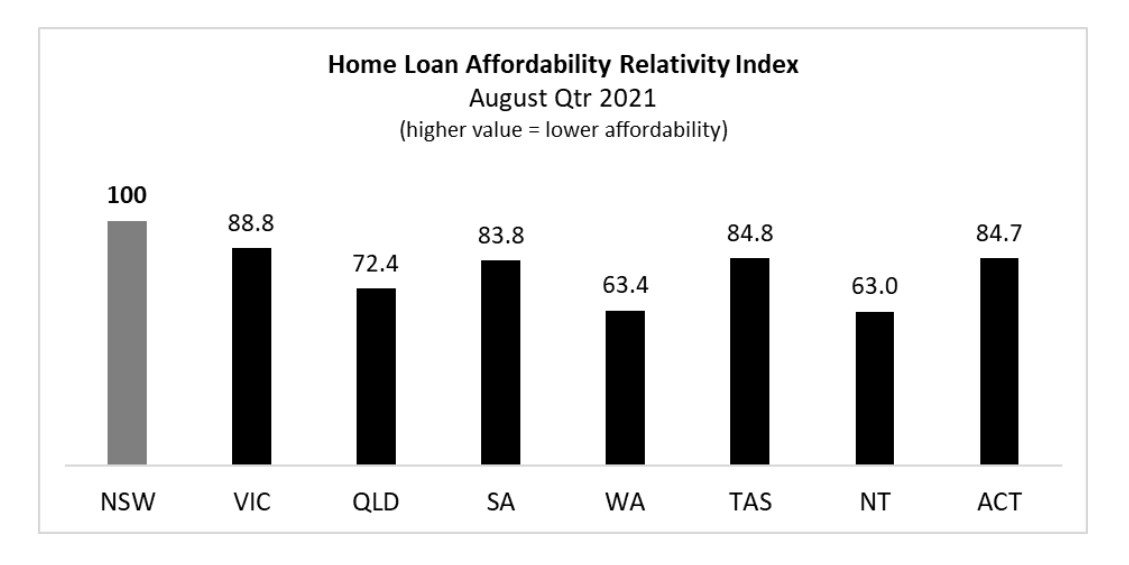

The latest Home Loan Affordability Index published in the September Bluestone Home Loan Market Report (that measures the repayment proportion of average incomes for newly approved home loans), reveals a significant disparity between the current level of loan affordability between states.

No surprise that NSW and VIC have reported sharp declines in home loan affordability over the past year, reflecting boomtime prices growth in Sydney and Melbourne.

By comparison, affordability has declined at lower rates in other states and with all significantly below the NSW result.

- Also read:Everything you need to know about the state of Australia’s property markets in 20 charts – May 2025

- Also read:Latest property price forecasts for 2025 revealed. What’s ahead in our housing markets in the next year or two?

- Also read:Perth housing market update | May 2025

- Also read:Where should I buy my next investment property in Australia?

- Also read:Brisbane Property Market Forecast [2025] – What’s Ahead & Where to Invest

Sydney and Melbourne median home prices remain well above those of the other state capitals, with the gap widening over the past year.

With similar income levels, those capitals retain significant home loan affordability advantages.

NSW clearly retains substantial home loan affordability constraints compared to the other states, reflecting the high-priced Sydney market.

The latest action by APRA is designed to restrict perceived risky home lending is a blunt, one-size-fits-all approach that does not account for the clear affordability disparities of local housing market conditions.

And clearly reflects the market power wielded through the big banks.

ALSO READ: What our biggest lender’s chief economist thinks about APRA’s changes