There’s a lot of talk about interest rates in the media recently isn’t there?

On the one hand, the Reserve Bank is saying rates are not going up any time soon.

On the one hand, the Reserve Bank is saying rates are not going up any time soon.

And on the other hand, rising property prices and decreasing housing affordability are causing many commentators to suggest interest rates are going to rise sooner rather than later.

But recently RBA Governor Phillip Lowe asserted (once again) that rates won’t rise any time soon.

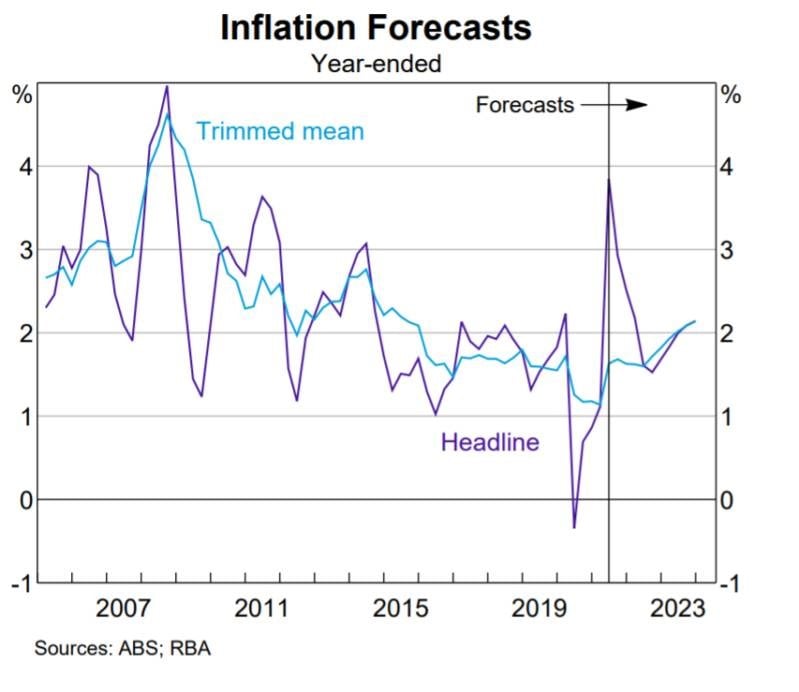

He said he finds it difficult to understand why the market is pricing in rate action 2022 and 2023 and confirmed that interest rate will only rise when inflation hits the target of between 2.5% to 3% and stays there for some time.

Clearly, our rising house prices are not going to affect the RBA’s interest rate decisions and Governor Lowe confirmed that house prices and housing affordability are not the domain of the RBA.

“ …the Board has said that it will not increase the cash rate until actual inflation is sustainably within the 2–3 per cent target range.

"It won’t be enough for inflation to just sneak across the 2 per cent line for a quarter or two.

"We want to see inflation around the middle of the target range and have reasonable confidence that inflation will not fall below the 2–3 per cent band again.”

RBA Gov Lowe: Delta, the Economy, and Monetary Policy

TAKE OUR 3-MINUTE SURVEY: How do you compare to other property investors?

Why are interest rates so low?

We know that the Reserve Bank lowered interest rates to bolster Australia’s economy as we headed into a recession caused by the Covid lockdowns last year.

But interest rates have been heading lower for quite a few years and Australia was late to the party.

Interest rates have been low around the world for some time.

Now there are various explanations for why interest rates are as low as they are around the world.

A cynic would say that it suits central banks to hold rates below the rate of inflation, thereby eroding the value of government debt and increasing asset values.

But there are less cynical explanations available…

One is that the aging and declining populations of Western countries are reducing demand.

One is that the aging and declining populations of Western countries are reducing demand.

Because there will be fewer people’s needs to cater for in the future, there’s less need for investment now – and therefore there’s less need to motivate people to save (by paying them interest) so others can borrow.

Another explanation is that low rates are driven by increasing inequality.

Mathew C Klien explains this much better than I could here.

- Also read:Brisbane’s property market forecast for 2025

- Also read:Melbourne property market forecast for 2025

- Also read:Latest property price forecasts for 2025 revealed. What’s ahead in our housing markets in the next year or two?

- Also read:Sydney property market forecast for 2025

- Also read:Home Prices Surge Following Rate Cut | Latest Housing Market Stats Dr. Andrew Wilson

Here are three facts about the recent history of the world:

- Income has become more concentrated within societies.

Both the shares of household income going to the top 1%and corporate profit shares have increased dramatically since the 1970s. - Inflation-adjusted interest rates are much lower now across much of the world than they were in the early 1980s.

That’s contributed to a surge in asset values relative to incomes — and likely means that future investment returns will be much lower than in the past. - The human population has aged rapidly, with the global median age rising by about ten years since the early 1980s.

The share of the population aged 65 and older in the high-income countries and China, which together account for the vast majority of global economic output, has already jumped from less than 7% in the 1970s to 13% today—and the United Nations projects that share will rise to 25% by 2060.

Research suggests that these facts are directly connected: the drop in interest rates has been caused by changes in population structure and by shifts in the distribution of income.

Research suggests that these facts are directly connected: the drop in interest rates has been caused by changes in population structure and by shifts in the distribution of income.

Lower expected returns on investment are just another consequence of deeper forces holding back economic dynamism.

Central banks have also been keeping interest rates low for years to try and boost inflation and increase wages.

This hasn’t worked in Australia, and it hasn’t worked overseas either.

Then of course during the pandemic, many Government’ responses have been to lower rates further to stimulate their economies.

By the way…It doesn’t really matter why interest rates are low.

I’ve found that when there are multiple explanations all pointing to the same outcome, you can have a good level of confidence about what’s going to happen.

I’ve found that when there are multiple explanations all pointing to the same outcome, you can have a good level of confidence about what’s going to happen.

None of the factors leading to the current low level of interest rates are going to be reversed any time soon: debts are still growing, population decline takes decades to turn around, and addressing inequality in a meaningful way will take enormous structural change.

I know many people are concerned about inflation rising, and I agree if inflation does rise sustainably, the RBA will raise interest rates a little slow the economy down.

But before that happens inflation will need to remain in the range of 2.5-3% for some time; wages will need to rise and our economy will need to be booming.

And of course, that means the value of assets including real estate will have gone up between now and then (when interest rates eventually rise.)

And when the RBA does increase interest rates we are likely to get a few small increases – rates are not going to go up to 6 or 7%.

The RBA won’t want to smash the economy.

And rising rates won’t mean that scores of Aussies will fall into mortgage default like some of the scaremongers are suggesting.

And rising rates won’t mean that scores of Aussies will fall into mortgage default like some of the scaremongers are suggesting.

Remember banks are currently stress testing serviceability for new loans at interest rates of more than 5% to ensure borrowers won’t get caught out.

So I’d plan for low-interest rates to persist until something significant changes.

This means that for those who have steady jobs and good cash flow, borrowing makes sense in today’s low-interest-rate environment.

In fact, good debt is an asset today when you can borrow at 3% and buy an investment-grade property that will increase in value at 7-10% per annum over the long term.

How are you going to take advantage of this low-interest-rate environment?

TAKE OUR 3-MINUTE SURVEY: How do you compare to other property investors?