Interesting how the talk about us falling over the fiscal cliff in September has disappeared.

But now some property pessimists are suggesting we have just kicked the can down the road and mortgage stress is going to hit hard next year.

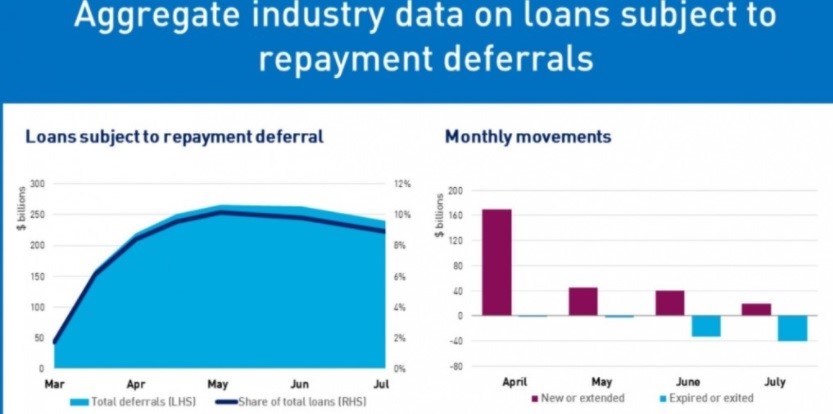

That's because many banks have granted temporary relief to borrowers impacted by COVID-19, allowing them to defer loan repayments for a period of time.

APRA report that there are $160 billion worth of housing loans that have deferred, being 9% of the $1.8 trillion in total housing loans.

However there is no real need to worry about these deferred loans according to leading commentator Pete Wargent.

While some believe that mortgage stress will have a major negative impact on the housing market, according to Wargent deferrals are now clearly in decline, and Australia’s high level of loan repayment deferrals is unlikely to prevent a housing market rebound in 2021, .

APRA’s latest figures reported housing loan deferrals decreased to $167 billion in July from a total $1.8 trillion loan book for authorised deposit-taking institutions (ADIs), representing about 9 per cent of loans still subject to housing loan deferrals.

Source: APRA

Wargent explains that “there is a significant ongoing improvement underway, although clearly 9 per cent of loans subject deferral is still an elevated number, and significantly higher than what would be considered a typical figure for mortgages in arrears”.

Source: APRA

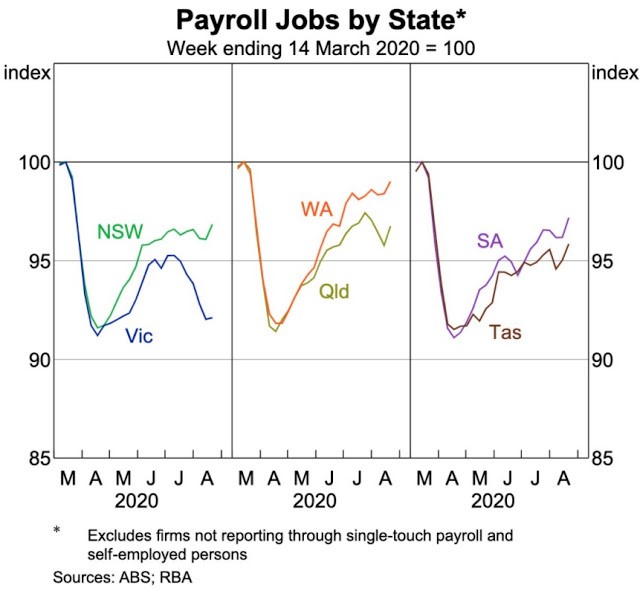

Even in Melbourne, consumer confidence has increased recently as demonstrated by Victorian reporting a sharp increase on ANZ-Roy Morgan’s latest survey, as signs have emerged that newly confirmed COVID-19 cases have been brought under control, implying that restrictions on movement may be relaxed sooner than previously feared.

However, some risks remain, especially relating to landlords with rental apartments in the major capital cities.

For example, the continued impact of the COVID19 has led to the extension of an eviction freeze out until March 2021 in New South Wales.

This applies further cash flow pressure on landlords, who very often rely on the rental income to service their mortgage.

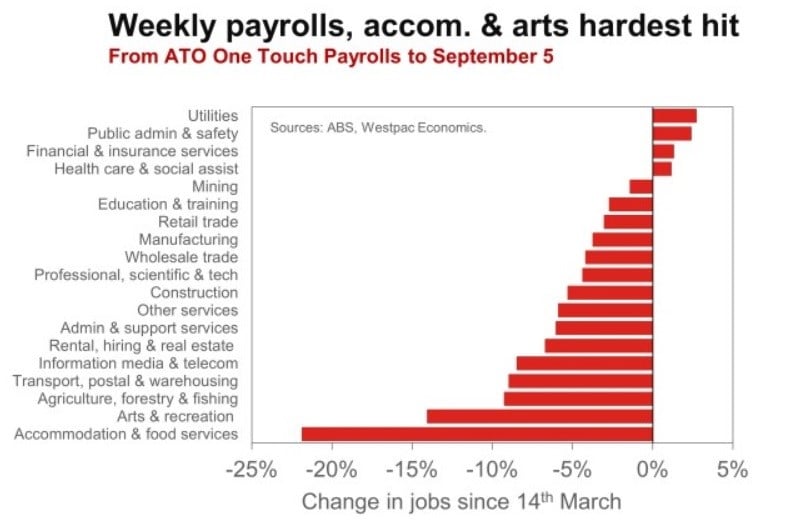

The weekly payroll figures suggested that between mid-March to mid-May, some of the most significant declines in payrolls occurred in sectors such as accommodation & food services (–29 per cent), arts & recreation (–26 per cent), administration & support services (–10 per cent).

By the first week of September there had only been a modest recovery in accommodation and food services (still -22 per cent) and arts & recreation (-14 per cent).

“This is materially higher than the normal acceptable rate of arrears which might be around 1 to 2 per cent, and in the range of 2 to 3 per cent in states and territories which have been struggling economically” Wargent said.

Doron Peleg of Riskwise Property Research said

“Banks have a very clear strategy to minimise forced sales as much as possible.

We’re seeing lenders, who are our clients, assessing the risks and opportunities for price increases at the individual loan level, before making specific decisions regarding the extensions of holiday repayments and flexible arrangements with borrowers.

“The significant improvement in buyer sentiment in relation to dwelling prices, (as demonstrated by preliminary auction clearance rates that are consistently above the 70 per cent mark for houses in Sydney), show that the risk associated with the vast majority of the deferred loans is lower than expected” Mr Peleg said.

Many borrowers had opted to defer repayments without necessarily being at risk of default according to Wargent.

- Also read:Everything you need to know about the state of Australia’s property markets in 20 charts – April 2025

- Also read:Sydney property market forecast for 2025. Is it a good time to invest in Sydney?

- Also read:Brisbane Property Market Forecast [2025] – What’s Ahead & Where to Invest

- Also read:Melbourne property market forecast for 2025 | Is it a good time to invest in Melbourne?

- Also read:Latest property price forecasts for 2025 revealed. What’s ahead in our housing markets in the next year or two?

“Mortgage brokers have signalled that many borrowers elected to take a repayment holiday in order to maintain a financial buffer, as a form of insurance policy, rather than through genuine duress. And targeted stimulus measures providing income support have been very effective, as has been borne out by the lowest bankruptcy and insolvency figures in a quarter of a century”.

“Moreover, banks have reported lately that increasingly owners are beginning to make repayments again, with about 109,000 loans being repaid again by the end of July, suggesting that the figures will continue improve over the coming six months” Mr Wargent said.

Risk areas remain but employment is recovering

The recovery in employment was comfortably stronger than expected through August, despite being held back by Victoria.

Mr Peleg of RiskWise said “we’ve seen that the shutdown measures have disproportionately impacted lower income occupations, and as such there is a risk of rental arrears continuing to rise over the coming year. And this is a time when inner city unit vacancy rates have been at record highs, including in Sydney, Melbourne, and Brisbane”.

“Therefore, we expect that some landlords will experience cashflow pressures in 2021, as previously projected in our Top 10 Unit Oversupply Areas report”.

Regulatory monitoring

The regulator APRA is keenly aware of the risks when mortgage holidays end, and issued a letter to deposit-taking institutions following a review of plans for the assessment and management of loans with repayment deferrals.

ASIC noted that some plans included reference to borrowers accessing their superannuation as an option that could potentially be considered if borrowers are unable to resume repayments.

Mr Peleg of RiskWise said that

“overall, there is a very low incentive for lenders to push stressed borrowers into default leading to a wave of forced sales or foreclosures, and practical solutions are likely to be found”.

“When a risk becomes well known and widely discussed it rarely blows up into the major outcome that is feared, at least in part because when risks are discussed so openly solutions are found.”

Wargent said:

“we have seen a similar dynamic previously with the feared interest-only loan reset in recent years, which did not lead to widespread arrears or defaults, despite much breathless reporting.

“This is a different and somewhat unique situation, but we expect lenders to work with borrowers and regulators to smooth the transition, especially at a time when mortgage rates are at record lows and interest serviceability has improved so significantly”.

“Overall, borrowers are now beginning to make repayments again, employment is generally recovering steadily, at least outside Victoria, there is a noticeable improvement in housing measures and projections, and we expect lenders to work closely with borrowers in the first quarter of 2021 to manage the transition, with regulatory oversight”

Fewer forced sales

Mr Peleg said

“the upcoming changes to responsible lending, could significantly decrease the number of forced sales. Responsible lending obligations have created a supply barrier of credit from the banks to lenders and particularly for property investors.”

“The upcoming changes will simply enable banks, that have been experiencing a fierce competition from non-bank lenders, to compete more aggressively, i.e. to simply write more loans.

“Obviously, this can have a clear flow-on effect on the aggregate demand for property, and therefore on property prices. The likely increase in property values make the current deferred loans less risky, as borrowers have properties with higher likelihood to increase in value in the future. “

The announced changes may also provide a variety of re-finance options for borrowers.

“Consequently, the number of forced sales is likely to be low, and it is highly unlikely that forced sales will have a macro impact on the property market” Mr Peleg said.

Now is the time to take action and set yourself for the opportunities that will present themselves as the market moves on

If you're wondering what will happen to property in 2020–2021 you are not alone.

You can trust the team at Metropole to provide you with direction, guidance and results.

In challenging times like we are currently experiencing you need an advisor who takes a holistic approach to your wealth creation and that's what you exactly what you get from the multi award winning team at Metropole.

If you're looking at buying your next home or investment property here's 4 ways we can help you:

- Strategic property advice. - Allow us to build a Strategic Property Plan for you and your family. Planning is bringing the future into the present so you can do something about it now! This will give you direction, results and more certainty. Click here to learn more

- Buyer's agency - As Australia's most trusted buyers’ agents we've been involved in over $3Billion worth of transactions creating wealth for our clients and we can do the same for you. Our on the ground teams in Melbourne, Sydney and Brisbane bring you years of experience and perspective - that's something money just can't buy. We'll help you find your next home or an investment grade property. Click here to learn how we can help you.

- Wealth Advisory - We can provide you with strategic tailored financial planning and wealth advice. Click here to learn more about we can help you.

- Property Management - Our stress free property management services help you maximise your property returns. Click here to find out why our clients enjoy a vacancy rate considerably below the market average, our tenants stay an average of 3 years and our properties lease 10 days faster than the market average.