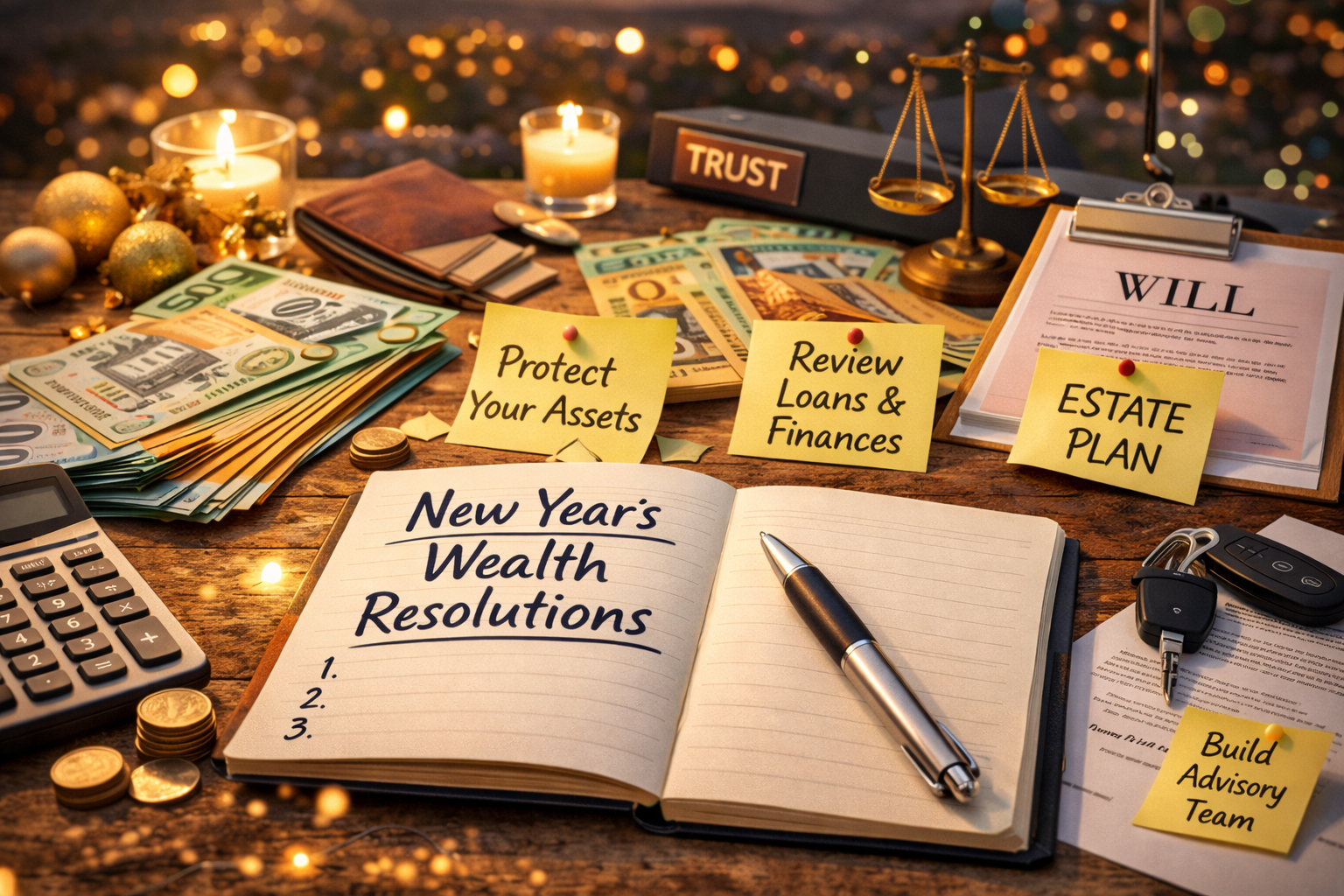

Key takeaways

Get intentional about your plan – Start your year by actually writing down what you want to achieve with your wealth instead of hoping things just happen.

Build a team you trust – Surround yourself with advisers and experts who fill the gaps in your knowledge and help keep your decisions smart.

Protect what matters – Take a good look at risk, insurance and your ownership structures so life’s surprises don’t wipe out your progress.

Sharpen your finance strategy – Review your loans, borrowing capacity and cash flow to ensure your money is working for you, not against you.

Sort your will and estate plans – Having a current will and clear legacy strategy isn’t just sensible, it’s essential if you want your family to benefit smoothly long-term.

Look at the details most people avoid – Things like power of attorney, guardianship and how superannuation passes on can make a massive difference to how your wealth is preserved for the next generation.

I’ve always believed that the start of every year is the ideal time to consider your wealth creation goals.

So, why don’t you ask yourself this question:

Will this be like most other years where good intentions are forgotten or put aside because of the pressures of everyday life?

As the saying goes:

Why put off until tomorrow what you can do today!

To ensure you start this new year as one full of opportunity, here are six top tips to help you grow, protect, and pass on your wealth.

1. Plan

As we always say in this business, a failure to plan is a plan to fail.

So, it’s vital that you have a plan for your financial future, which must start with a critical – but realistic review – of what you currently have and require in the future.

If you’re in a relationship, then your plan must take all party’s considerations into account.

Of course, that’s because “You can’t row a boat straight if only pulling on one oar!”

Plus, with multiple people, having additional input from your partner also makes decision-making much easier.

It’s also wise to take the time to assess your current position and take into account the need to change tact to achieve your end game.

Life does not always go straightforward, so be prepared to be flexible, make incremental improvements, and reward yourself at each milestone – of course, while keeping your eye on the prize.

2. Surround yourself with smart people

They say life was not meant to be easy, but it can be a whole lot easier with the decision to put yourself in control of your financial future.

One of the simplest ways to do this is to gather a team of people around you to help with the details as well as the areas that you are not expert in.

That’s because we all need help to implement our plans as well as to take emotion out of financial decisions.

Remember, it’s never wise to be the smartest person on your team!

The truth of the matter is that buying investment-grade assets, while obvious to some, unfortunately, is not widely implemented.

What usually happens when people go it alone is that they buy the wrong assets and therefore saddle themselves with poor-performing ones instead.

Of course, that will ultimately mean that their financial freedom goal becomes ever more elusive.

3. Minimise risk

Everyone starts the year full of hope and excitement about the year ahead.

Alas, some of us won’t make it to see another full calendar year – which is not something anyone wants to think about.

However, you need to ensure you and your family are protected against the unknowns such as in this scenario.

Take the time to look at your various insurance needs, which will not only help pay your loans but also maintain your family’s lifestyle.

If you’re in business with others, check that your key insurances and buy/sell agreements are up to date as well as if your business is using the optimal structure.

Another risk minimisation strategy is to consider which name you use to hold assets.

- Also read:6 Lessons from Robert Kiyosaki’s Rich Dad Poor Dad to Build Wealth and Financial Independence

- Also read:Retirement might not be as enjoyable as you expect

- Also read:3 Lessons I learned at Wealth Retreat

- Also read:How does my super get taxed?

- Also read:Why Testamentary Trusts Aren’t Just for the Rich: A Guide to Safeguarding Your Legacy Introduction

This is especially important if you are exposed to unscrupulous and even unjustified litigation, which could wipe out all your hard work.

It’s also important to consider whether your property ownership structures maximise tax benefits, including land tax.

Another way to reduce risk is to always only buy investment-grade assets, because adopting such a savvy strategy could help you achieve your financial goals up to 50 per cent faster!

4. Finance strategy

At the start of the year, you should also look at your borrowing capacity as well as current loan requirements.

By doing this, you can start to work with an expert to develop a finance strategy to help you achieve your goals.

This strategy can include assessing whether your loans are effectively set up, especially in relation to a redraw or offset facility.

These can produce vastly different tax outcomes, which is why it’s so critical to get the correct loan structure in place.

In Australia, the beginning of each year is summer, so we don’t like to think about the seasons that follow that.

However, you must be prepared for rainy days (metaphorically speaking) by creating a financial safety net that you can draw upon in times of unexpected job loss or illness.

5. Wills and risk

As I mentioned earlier, no one likes to think about the day they are no longer around.

It really is the elephant in the room, which is why most of us try and avoid considering how our wealth will be distributed after our death.

However, it seems pointless to have been working your whole life to have it all disappear as soon as you have passed on.

You see, most people do not have a will and if they do then it normally only focuses on who and what their dependents will receive, which are emotional decisions.

Of critical importance is how the distribution from your will is made as this can significantly influence whether your dependent will retain the wealth in the family, or have it exposed in a family break down where the assets could go to people who aren’t your direct descendants.

The “how” will also impact the tax that is paid on income generated from these assets.

So, depending on how you hand down your assets, it can trigger many tens of thousands of dollars, on even modest estates, of additional taxes that could have been avoided.

Wills should also look at non-estate assets, such as superannuation, which require different paperwork as they can’t be part of our will.

Again, different tax liabilities will arise depending on different superannuation distributions.

A number of other important areas to consider include power of attorney, guardianship and medical authorities to name just a few.

While most assets can be shifted on death, without capital gains tax or stamp duty, this won’t always be the case – especially if the recipient is living overseas – so your will should take this into account.

At the end of the day, and the end of your days, not having a will – which is called dying intestate – can mean your wealth may not be distributed according to your wishes.

No one wants their loved ones to be mourning their loss at the same time as undergoing unnecessary financial heartache, do they?

Disclaimer

This article is general information only and is intended as educational material. Metropole Wealth Advisory nor its associated or related entitles, directors, officers or employees intend this material to be advice either actual or implied. You should not act on any of the above without first seeking specific advice taking into account your circumstances and objectives.