Key takeaways

Cotality Home Value Index surged 8.6% higher in 2025, adding approximately $71,400 to the national median dwelling value.

This marks the strongest calendar year gain in home values since 2021, when the market rose a stunning 24.5% amid emergency low interest rates and record-high levels of purchasing activity.

But signs of softening are appearing.

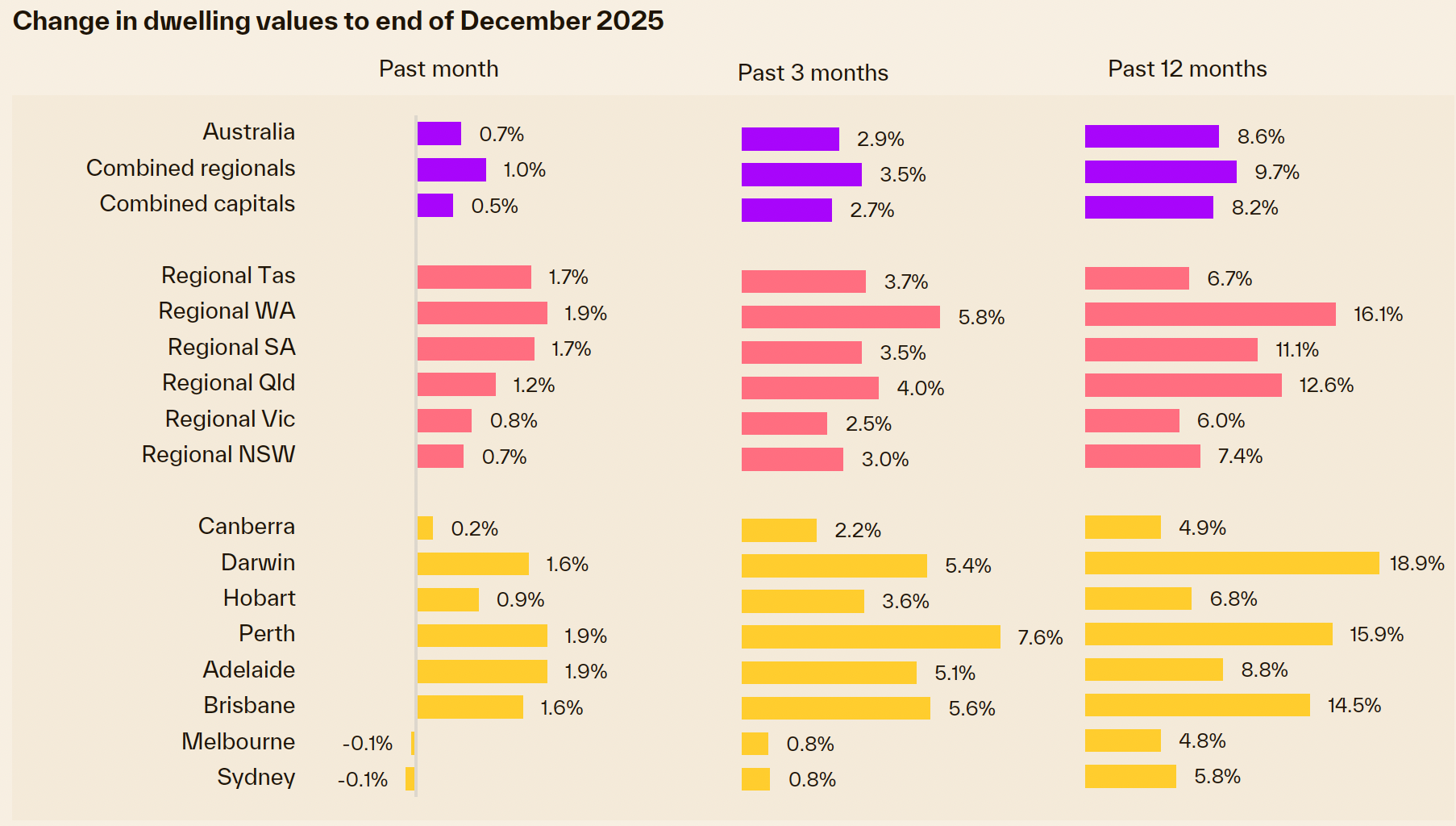

December saw the smallest monthly increase in five months (0.7%), with Sydney and Melbourne posting slight declines, signalling a softer start to 2026 as rate hike fears and affordability pressures weigh on confidence.

Outlook for 2026 - modest and uneven growth expected: The report forecasts a less optimistic housing outlook for 2026 due to inflation risks, higher interest rates, and stretched affordability.

Affordability pressures are shifting demand downmarket as buyers are pushed toward the lower and middle price points.

Regional markets outperformed capitals, with combined regional dwelling values rising 9.7% over the year, outpacing the 8.2% growth in capital cities.

Cotality Home Value Index surged 8.6% higher in 2025, adding approximately $71,400 to the national median dwelling value.

But recorded the smallest gain in five months in December, with value rising 0.7%.

Sydney and Melbourne were the biggest drag on the headline growth outcome with values sliding -0.1% lower.

The subtle decline in values across Australia’s two largest cities marked the first month-on-month decline since January last year, prior to rate cuts which commenced in February.

Every other capital and broad rest-of-state region recorded a rise in values through December, although most saw some momentum leave the market.

This softening hints at a weaker start to housing trends in 2026.

Renewed speculation that the rate-cutting cycle is over and the next move from the RBA could be a hike has dented housing confidence.

A ‘higher for longer’ setting on interest rates, alongside a resurgence in cost-of-living pressures and worsening affordability pressures, looks to have taken some heat out of the market.

Despite the softer December outcome, the Home Value Index surged 8.6% higher in 2025, adding approximately $71,400 to the national median dwelling value.

Note: This marks the strongest calendar year gain in home values since 2021, when the market rose a stunning 24.5% amid emergency low interest rates and record-high levels of purchasing activity.

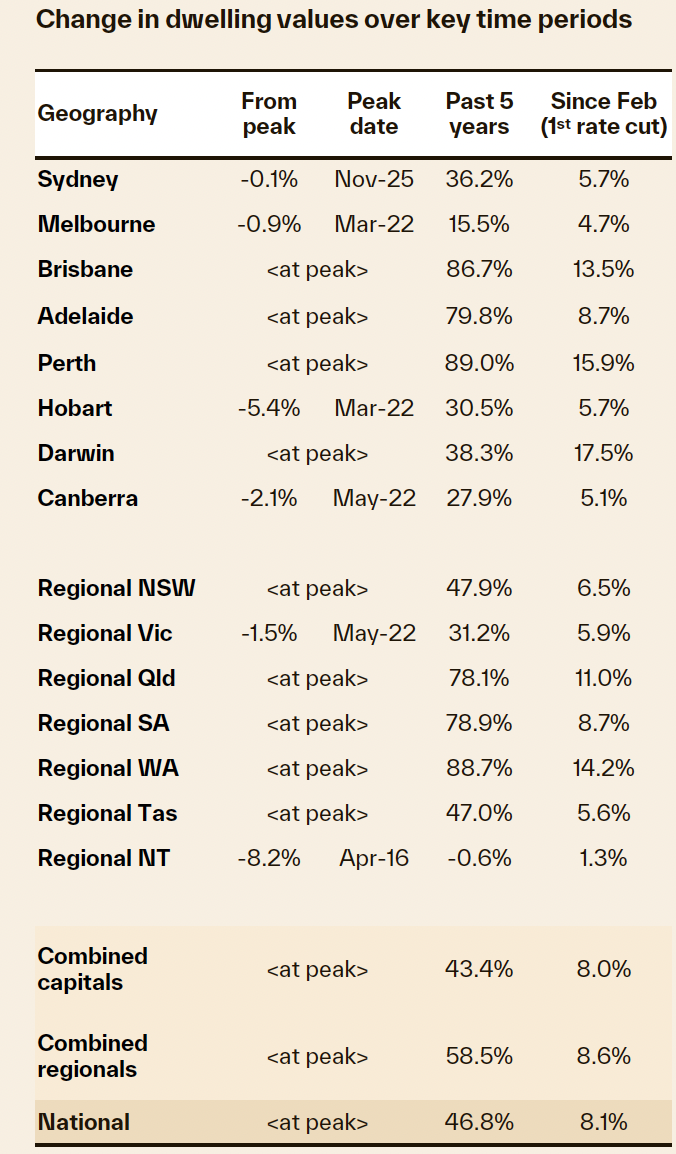

Every capital city and rest-of-state region recorded an increase in dwelling values over the year, bookended by Darwin, up 18.9% and Melbourne with a milder 4.8% gain.

The upper quartile of the market continues to weigh on growth outcomes.

At a national level, upper quartile dwelling values were up 0.2% in December, while values across the lower quartile and middle of the market were 1.1% higher.

This trend, where upper quartile values have recorded a lower rate of growth, has played out across every capital city through the year, as affordability and serviceability pressures deflect demand towards the lower price points.

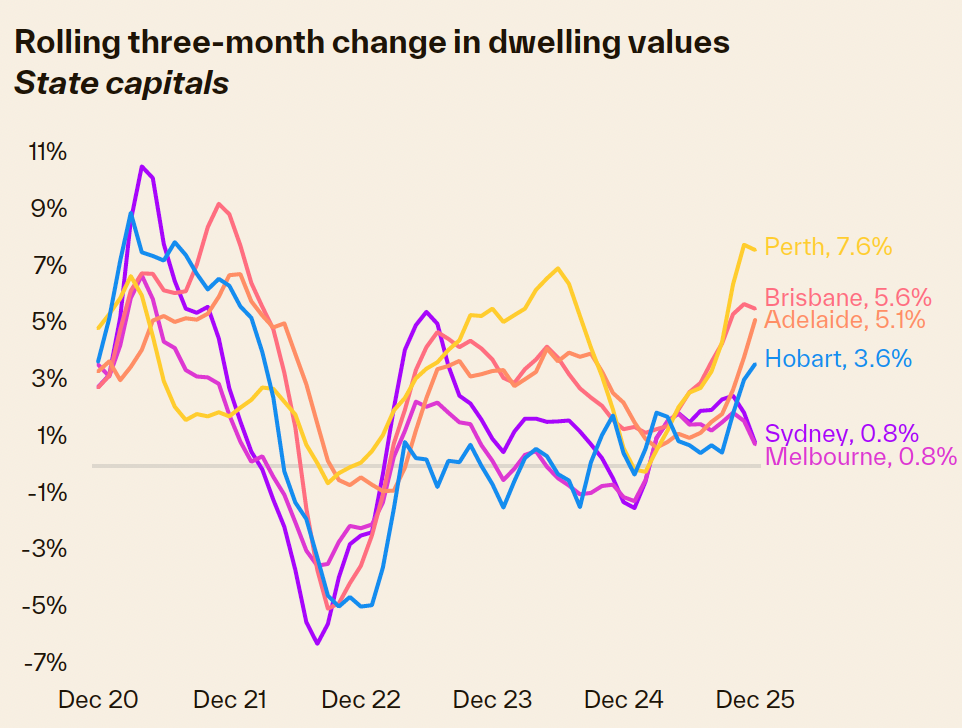

Regional markets have been more resilient to a slowdown, but not completely immune.

The monthly pace of growth across the combined regional markets of Australia slowed from 1.2% in November to 1.0% in December.

Despite the easing, the monthly pace of gains was double the combined capital city growth trend, where values rose by 0.5% in December.

Over the calendar year, regional dwelling values rose by 9.7%, outpacing the 8.2% rise recorded across the combined capital cities.

Across the rest-of-state regions, Western Australia stood out with a 16.1% annual increase, followed by regional Queensland, up 12.6%.

Regional Victoria recorded the lowest growth outcome over the year, with values up 6.0%.

Looking ahead to 2026, the housing outlook is less optimistic than 2025.

Uncertainty around inflation and interest rate settings is likely to weigh on housing confidence, along with ongoing affordability challenges and renewed focus on household debt and credit policy.

However, we are unlikely to see a material supply response in 2026 either, which should help to offset any downside risk to home values trending substantially lower.

- Also read:Something strange is happening in Australia’s housing market right now | Property Insiders

- Also read:Latest Property Price Forecasts Revealed. Australian Property Market Outlook 2026: Where To Now After The Rate Rise.

- Also read:National Weekly Auction Report – March 7th 2026 | Auction Clearance Rates Ease as Listings Fall Over Holiday Weekend

- Also read:Latest Property Asking Prices State by State | National Listings Rebound Strongly in February as New Supply Surges

- Also read:Booming Housing Markets Rise Over February | Latest stats from Dr. Andrew Wilson

Macro factors, including inflation, interest rates, and credit policy, alongside affordability challenges, are likely to be the primary headwinds facing housing conditions through the year.

Inflation risks are back on the radar, implying a ‘higher for longer’ interest rate setting as the RBA focuses on getting inflation back to target.

All eyes will be on the monthly CPI update, due on January 7th, to see where the inflation trend is heading.

The latest update, to October 2025, showed annual headline inflation rising to 3.8%, with core inflation lifting to 3.3%.

The risk of a rate hike remains elevated, especially if core inflation proves stubborn, holding above the RBA’s 2-3% target range.

The heightened risk scenario is already weighing on confidence, with the Westpac-MI monthly consumer sentiment index dropping 9% in December, and the ‘Time to Buy a Dwelling’ index down a larger 10.6%.

At 3.6%, the cash rate remains a full percentage point above the pre-pandemic decade average of 2.5%.

With housing prices at record highs and interest rates above average, mortgage serviceability remains stretched.

Even with the 75-basis points of rate cuts last year, a typical household purchasing the median-priced dwelling would be dedicating 45% of their pre-tax income to service a mortgage1.

With APRA focused on household debt levels and watchful for any slippage in lending standards, mortgage serviceability factors are likely to continue funnelling housing demand towards the lower-to-middle price points.

This is where housing prices have been rising the fastest, as mainstream demand competes with a pickup in first home buyers and elevated levels of investor activity.

Beyond the macro factors, housing affordability barriers should naturally put the brakes on the pace of housing growth.

Based on data to September, housing affordability metrics are stretched to record levels.

The national dwelling value to income ratio is at 8.2, it would take a household on the median income 11 years to save a 20% deposit, and renters are dedicating a record high 33.4% of their annual pre-tax income to pay their rent.

That said, the market is not without support.

Persistently low levels of stock, both from new builds and existing listings, should act as a buffer against price falls.

Government incentives aimed at first-home buyers should also help maintain some momentum at the entry level, even as broader market conditions remain tough.

Overall, the outlook points towards modest but uneven growth in home values through 2026.

The balance between inflationary pressures, RBA policy decisions, and ongoing supply shortages will be critical.

While downside risks are more pronounced, structural undersupply and targeted stimulus should help stave off a material correction, leaving the market resilient in many areas despite the headwinds.