The expanded First Home Guarantee Scheme (FHGS) is certain to increase first home buyer demand.

The scheme will also cause a largely unanticipated property market boom in first home buyer suburbs.

Aspiring first home buyers have to overcome two huge barriers.

They must raise a deposit of at least twenty percent of the purchase price, and they need to qualify for a home loan to secure the balance.

Imagine the consequences if the required deposit fell to just five per cent while falling interest rates increased the amount that first home buyers could secure?

Yet, that is exactly what is about to occur.

The new FHGS is a game changer

The Federal Government has brought forward the FHGS rollout, with no place limits and no income caps, but the real game changer is that property price caps have been dramatically increased.

Put simply, it means that first home buyers can compete with each other to buy homes with just five percent deposit until the price caps have been reached.

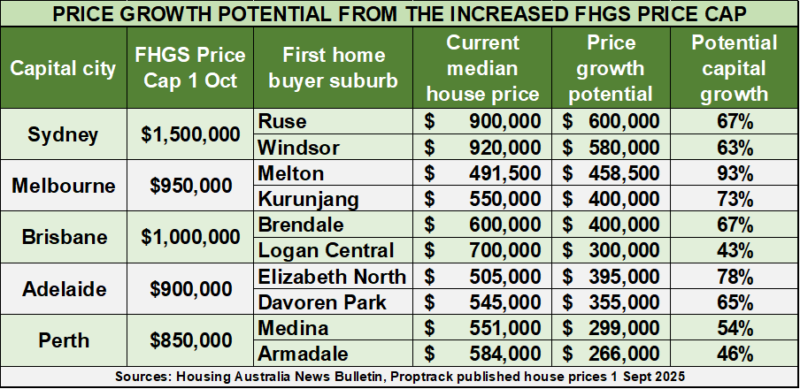

This table shows you how much buy prices in typical first home buyer suburbs could increase before they reach the new caps, with most suburbs potentially rising by over fifty percent.

- Also read:Melbourne property market forecast for 2026 | Is it a good time to invest in Melbourne?

- Also read:Latest Property Price Forecasts Revealed. Australian Property Market Outlook 2026: Where To Now After The Rate Rise.

- Also read:Brisbane Property Market Forecast [2026] – What’s Ahead & Where to Invest

- Also read:Sydney property market forecast for 2026. Is it a good time to invest in Sydney?

- Also read:Perth housing market update | March 2026

Incredibly, some first home suburbs in Melbourne could nearly double in price before capping out.

Lower interest rates increase borrowing power

Of course, lower deposits mean bigger mortgages, so prices can only rise if the borrowing power of first home buyers dramatically increases.

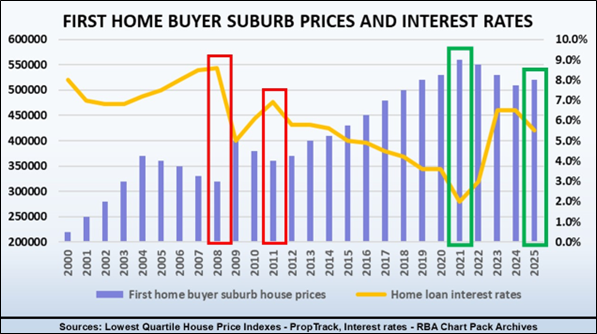

But, that’s exactly what is happening - we have had three rate cuts this year, with the RBA forecasting at its latest Monetary Board Meeting in August that another two cuts are anticipated by early next year.

This graph shows you how prices in lower priced suburbs have reacted to interest rate increases (red outline) and falls (green outline) over the last twenty five years, clearly showing that first home buyer suburbs tend to boom when rates fall.

The increase in first home buyer demand will see prices rise in many affordable locations and prices in some of those suburbs are set to boom.

But, this speedup of the expanded FHGS also means that time is running out for you to take advantage before the price growth really kicks in.