Key takeaways

Australia’s property market has fractured into dozens of micro-markets, with different cities, suburbs, and price points moving in opposite directions. Broad market averages are now far less useful for investors.

Affordable housing is outperforming premium property as government incentives and shrinking supply drive strong demand from first-home buyers. Lower-priced homes are now leading growth in many markets.

Supply shortages remain one of the biggest drivers of future price growth, with entry-level houses becoming increasingly scarce across Australia. Demand continues to outpace new housing construction.

The “easy money” era created by falling interest rates, booming migration, and cheap property prices has ended. Future success will depend far more on strategic property selection and strong finance structures.

Investors are likely to achieve better long-term results by focusing on high-quality properties in established inner and middle-ring suburbs with strong owner-occupier demand. Quality and scarcity matter more than ever in the next phase of the market

A few years ago, you could buy almost anything in a reasonable suburb of a capital city or major regional centre, hold it through a cycle, and come out well ahead.

The rising tide did most of the heavy lifting. Selectivity mattered, but it wasn't make-or-break.

Today it is.

The market has splintered into dozens of micro-markets moving in completely different directions at the same time, and the gap between the best and worst performing assets is wider than I've seen in a very long time.

I'm not saying property is a bad investment - far from it.

In fact, I'd argue there's still enormous opportunity ahead for those who approach it with the right strategy.

But the broad, rising-tide conditions that rewarded average decisions are giving way to something more selective, more fragmented, and more demanding of genuine skill.

The market has splintered - and many investors haven't noticed

The phrase "the property market" has always been a simplification, but it's become increasingly misleading.

Today, saying you're investing in "the Australian property market" is a bit like saying you're investing in "the share market" without specifying whether you mean tech stocks, mining companies, or dividend payers.

The category is so broad as to be almost meaningless.

The Australian property market has never been “one market”, and it's really the same with Melbourne, Sydney, or Brisbane, there's not one capital city, market.

They are fragmented into multiple micro-markets, even within the same suburb, making broad assumptions genuinely dangerous for investors.

We're seeing capital cities move in completely different directions. Perth posted a staggering 22% annual gain while Brisbane followed with 17.3% annual growth, yet higher interest rates, increased listings, and affordability constraints are cooling demand in parts of Sydney and Melbourne, leading to more modest price growth and some short-term declines in those markets.

That's several markets operating under completely different conditions at the same time.

Even within cities, the split is remarkable

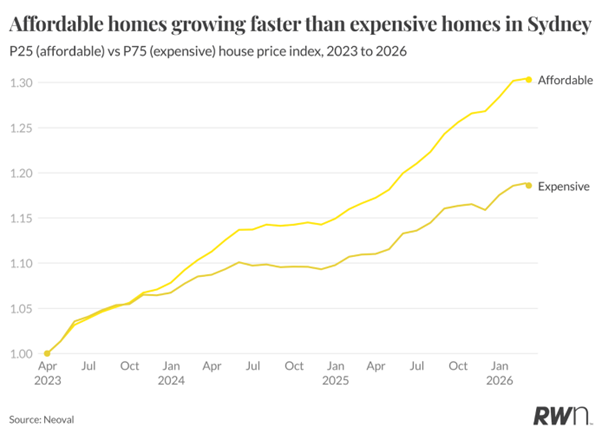

Recently, Ray White Chief Economist Nerida Conisbee identified a "K-Shaped" dynamic playing out in Australian housing.

Since late 2023, house prices at the 25th percentile of the Sydney market have risen around twice as fast as those at the 75th percentile - creating a widening gap between the cheaper and more expensive ends of the market.

In previous cycles, the top end of the market typically led price growth, with cheaper properties following. Now it's running in reverse.

The expanded first home buyer deposit guarantee scheme, which was significantly broadened in October 2025, triggered a 10.9% rise in first-home buyer loans in New South Wales in the December quarter alone - roughly double the growth recorded for investor lending over the same period.

Government policy has effectively turbocharged demand at the affordable end of the market, and that tailwind isn't going away anytime soon.

The supply squeeze is real and structural

One of the most powerful forces shaping property values right now isn't glamorous - it's just basic supply and demand.

Over the past decade, national house sales under $750,000 have fallen from about 248,000 in 2015 to roughly 153,000 in 2025.

Entry-level detached homes are simply disappearing from the market.

Australia remains significantly undersupplied, with an estimated shortfall of over 200,000 homes and declining dwelling approvals highlighting the ongoing gap between supply and demand.

When you combine shrinking supply with surging demand from first home buyers armed with government guarantees and recovering borrowing capacity, you get what we're seeing - strong price growth at the affordable end, even as affordability gets worse overall.

The median is lying to you

One thing that consistently misleads investors is the way we talk about property prices.

The median is not the market. It's the midpoint of the market, and as conditions fragment, the gap between what's happening at different price points widens considerably.

The national dwelling value-to-income ratio reached 8.2 in September 2025, compared with a 20-year average of 6.8, and it now takes 11 years to save a standard 20% deposit.

Despite those headline numbers, buyers are still finding ways into the market - they're just adjusting where and what they buy, shifting toward units and smaller homes in more accessible price ranges.

Investors who are still making decisions based on city-wide medians are effectively flying with outdated instruments.

The regional story has also matured

For a long time, regional property was considered the riskier, lower-quality alternative to capital city investing. That view deserves some revision, though selectivity matters more than ever.

Between 2015 and 2025, regional house prices grew 98.8% to $688,000, while national house prices grew only 84.7% to $950,000.

The lifestyle migration shift that accelerated through COVID has had lasting structural effects. And commodity-driven markets in WA and Queensland have added further momentum through mining and agriculture cycles.

Note: But - and this is important - not all regional markets are created equal.

The commodity-driven markets of WA and Queensland are behaving very differently from lifestyle markets in coastal NSW or Tasmania, and South Australia is increasingly functioning as an affordability escape valve for buyers priced out of other states.

Selecting a regional market now requires the same rigour as selecting a suburb in a capital city.

- Also read:Melbourne property market forecast for 2026 & 2027 | Separating the fundamentals from the sentiment

- Also read:Brisbane Property Market Forecast [2026 & Beyond] – What The Olympics Decade Means for Investors.

- Also read:Sydney property market forecast for 2026 and 2027 | Why the short-term softness is a long-term opportunity

- Also read:Latest Property Price Forecasts. Australian Property Market Outlook 2026-2027: Navigating a Market Correction

- Also read:Falling Home Prices Accelerate Over June | Latest stats from Dr. Andrew Wilson

The days of regional markets simply rising together are over.

What "easy money" actually looked like - and why it's gone

Looking back, a lot of the wealth created in property over the past 20 years came from three sources that were, to varying degrees, outside investors' control.

The first was the long decline in interest rates from the early 1990s through to 2021.

Falling rates lifted borrowing capacity, pushed more buyers into the market, and expanded price-to-income multiples almost continuously.

That tailwind is now gone. The RBA is likely to raise interest rates again this year, and they will remain higher for quite some time.

The second was the period of extraordinary population growth following the reopening of borders post-COVID.

That surge in immigration drove demand across almost every market and compressed vacancy rates to historically low levels. Population growth has moderated from its peak, and its distribution is becoming less uniform.

The third was simply the benefit of low starting prices.

Investors who bought in the 1990s or 2000s had the wind at their backs in a way that today's buyers don't.

The key risks for 2026 centre on affordability and household borrowing capacity, with further growth depending on income gains, additional rate relief or meaningful improvements in housing supply.

Note: None of this means property stops working. It means property stops working automatically. The difference matters enormously.

What actually drives performance from here

The investors who will do well over the next decade are those who understand that correct property selection is now the primary driver of returns.

The broad market will continue to grow - undersupply, population growth, and construction costs all point in that direction.

But in 2026 and 2027, our property markets will be shaped by fundamentals, with demand still outstripping supply, costly construction, sticky inflation and policy settings that continue to push prices higher.

But within that broadly positive environment, the variance between the best and worst performing assets will be wider than ever.

What this means is that the inner and middle-ring suburbs of major capital cities - where land is genuinely scarce, owner-occupier demand is strong, and infrastructure is established - remain my preferred territory.

These areas have demonstrated the ability to attract both owner-occupiers and upgraders across multiple cycles, which is the most reliable demand profile an investor can target.

Properties that appeal to a wide pool of buyers and tenants - not niche properties that depend on a narrow group - are the ones that hold their value and attract reliable tenants through different market conditions.

And perhaps most critically, finance structure matters more than ever.

With borrowing costs higher than they were three years ago, and the RBA signalling caution, an investor's ability to hold through periods of short-term weakness is a genuine competitive advantage.

A great property that gets sold under pressure because of a cash flow squeeze is a failed investment, regardless of how good the asset fundamentally is.

The opportunity is real - it just requires more skill

In case you got me wrong, I want to be clear about something.

I'm not pessimistic about property. I've never been more convinced that well-selected property in the right locations remains one of the most powerful wealth-building tools available to ordinary Australians.

Australia's property market closed 2025 on a broadly positive footing, with overall very strong growth. However, the conditions moving forward suggest that while price growth is going to slow, opportunities remain - particularly in markets where growth is being driven by genuine demand rather than speculation.

But "genuine demand" is the key phrase there.

Markets driven by FOMO, cheap credit, or short-term data patterns are the ones that will disappoint.

Markets underpinned by long-term demographic fundamentals, constrained supply, and strong economic drivers are the ones that reward patient investors decade after decade.

The threshold for good decision-making has simply risen.

Generic strategies, average properties, and set-and-forget thinking carry more risk than they did before.

The investors who treat this moment as a reason to do more homework, build a clearer strategy, and focus on quality over quantity are the ones I'd be backing.

The easy money era may be over, but the smart money era is just beginning.

If you'd like help building a property strategy that's built for the way markets actually work today - not the way they worked a decade ago - the team at Metropole can help.

We work with investors at every stage to identify the right properties in the right markets, structure finance appropriately, and build portfolios designed to compound wealth over the long term.

Whether you're just starting your property investment journey or looking to take your portfolio to the next level, we’re here to help. At Metropole, we’ve helped thousands of Australians grow, protect, and pass on intergenerational wealth through strategic property advice - and we’d love to help you too.

This isn’t about a one-size-fits-all solution. It’s about understanding your unique situation, goals, and concerns - then giving you clear guidance on what your next move should be.