Key takeaways

Apartment construction in Victoria is not keeping up with population growth.

Since 2019, adjusted for inflation, the dollar value of new apartment projects is down by 27%, but construction costs have risen sharply—suggesting even fewer actual units are being built.

Meanwhile, Victoria’s population has grown by over 500,000 in the same period.

Net result: supply is increasingly constrained, setting the stage for upward pressure on prices.

Almost five years ago, I shared evidence that pointed to investment-grade apartments entering a growth cycle within a few years.

That prediction hasn’t materialised as prices have remained relatively flat since 2020.

But could that finally be about to change?

My past work on this subject

As noted above, I published a report in October 2020 analysing the performance of investment-grade apartments, especially in Melbourne.

I subsequently updated that report in 2021.

And last year, I wrote about what investors should do if they own an underperforming property. In short, I encouraged owners of high-quality, investment-grade apartments to hold firm and exercise patience.

It is time to update this work, as I believe there are several factors that may push investment-grade apartments into a growth cycle.

Supply is certainly a lot tighter

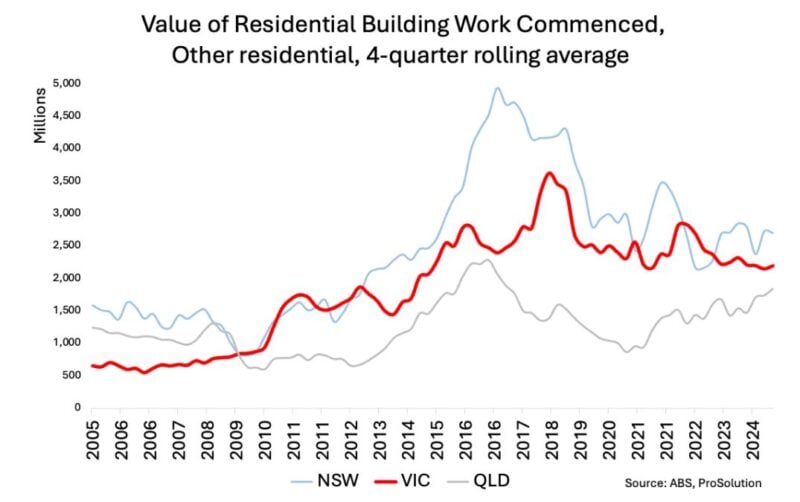

The chart below shows the total value of ‘other residential’ dwelling commencements, which includes apartments, units, and townhouses in Victoria, compared to NSW and Queensland.

At the start of 2019, the value of other dwelling commencements in Victoria was around $2.5 billion per quarter.

Adjusted for inflation, that’s equivalent to roughly $3 billion in today’s dollars.

In contrast, the current rolling average is sitting at about $2.2 billion per quarter, around 27% lower than 2019 levels.

It’s important to note that this data reflects the dollar value of commencements, not the number of dwellings.

Given construction costs have increased significantly over the past five years, it’s likely that the actual number of apartments being built has fallen by even more than 27%.

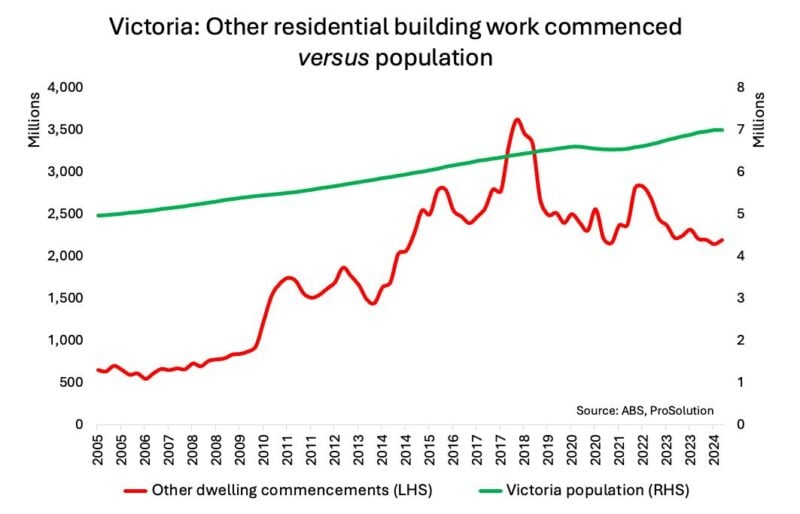

The chart above compares dwelling commencement values to Victoria’s population.

While commencements have fallen by 27% over the past six years, the population has grown by more than 500,000 people, or over 7.5%, during the same period.

In other words, apartment construction simply is not keeping up with population growth, and there are no signs of that changing in the near term.

Apartment replacement costs are much higher

Replacement cost refers to what it would cost today to buy the land and construct the dwelling from scratch.

Since the start of COVID, construction costs have jumped by around 30%.

That means developers now need to sell new apartments for more than 30% more (to also account for higher interest costs) than they did in 2020 to achieve the same profitability.

When replacement costs rise faster than market values, one of two things typically happens: developers stop building because projects no longer stack up financially.

This reduces supply and makes existing apartments relatively more attractive.

Alternatively, developers pass on the higher costs, which pushes up prices across the board, including for existing stock.

In short, rising construction costs eventually put upward pressure on prices in the established apartment market.

First homebuyer government stimulus

From 1 January 2026, the government will expand the First Home Guarantee (FHBG) to all first homebuyers.

Under this scheme, first-time buyers only need a 5% deposit, with the government guaranteeing the remaining 15% to satisfy the bank and avoid the need for mortgage insurance.

Previously, the scheme was capped at 35,000 places and subject to income limits, but both restrictions will be removed.

In addition, the government will increase the property price caps, making the scheme even more attractive.

The government expects over 80,000 buyers to take advantage of the FHBG, equivalent to around 11% of all property purchases, which means it’s likely to have a substantial market impact.

There’s little doubt this will fuel demand, particularly in the sub-$1 million segment (and sub-$1.5 million in Sydney).

Most investment-grade apartments will fall within the eligibility thresholds.

Falling interest rates are most useful to FHB

Money markets are now pricing in at least a 1% cut to official interest rates over the remainder of 2025.

If that plays out, we can expect home loan rates to fall below 5% and investment loan rates to drop under 5.5% by the end of the year.

- Also read:Melbourne property market forecast for 2026 | Is it a good time to invest in Melbourne?

- Also read:Latest Property Price Forecasts Revealed. Australian Property Market Outlook 2026: Where To Now After The Rate Rise.

- Also read:Brisbane Property Market Forecast [2026] – What’s Ahead & Where to Invest

- Also read:Sydney property market forecast for 2026. Is it a good time to invest in Sydney?

- Also read:March Home Prices Still Rising | Latest stats from Dr. Andrew Wilson

Lower interest rates improve affordability and effectively increase how much buyers can borrow – a 1% rate cut typically boosts borrowing capacity by more than 10%.

Buyers in the sub-$1 million price bracket tend to be particularly rate-sensitive, so a reduction of this size is likely to fuel further price growth in that segment of the market.

HELP debt to have a lower impact on borrowing capacity

The banking regulator has directed lenders to take a more flexible approach when assessing HELP debt.

If the debt is expected to be repaid within 12 months, lenders can ignore it entirely.

Some may also reduce the assessed repayment if it is likely to be cleared within five years.

Now that the FHBG is available to all first-time buyers, some may choose to use part of their savings to pay down their HELP debt to improve their borrowing capacity, particularly if doing so means the lender will disregard it altogether.

This is the first time the government has directly addressed how HELP debt affects borrowing power, and while the impact may be more modest than other changes above, it’s still likely to support demand for property.

Further, with the government introducing a 20% write-off of HECS debts, this will also drive FHBG borrowing capacity.

Relative value compared to other states and houses

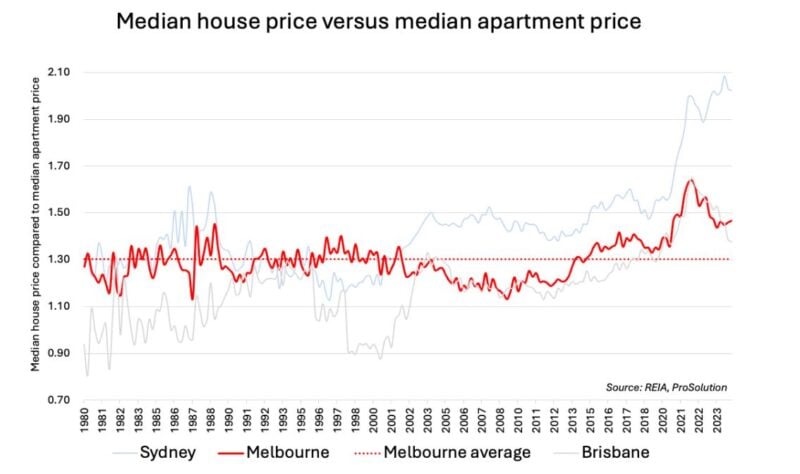

The chart below compares median house prices with median ‘other dwelling’ prices, which include apartments, units, and townhouses.

Melbourne is shown in red.

Historically, since 1980, the median house price in Melbourne has been 1.3 times the median price of apartments.

Today, that ratio has stretched to 1.5 times, after peaking at 1.64 times in March 2022.

Since March 2022, house prices have fallen by 18.6% according to the REIA, while apartment prices have only fallen by just under 9%.

Arguably, both houses and apartments in Melbourne offer good value at current levels.

However, the key takeaway is this: the price gap between houses and apartments in Melbourne has not been this wide in 45 years.

Therefore, on a relative basis, investment-grade apartments look like great value.

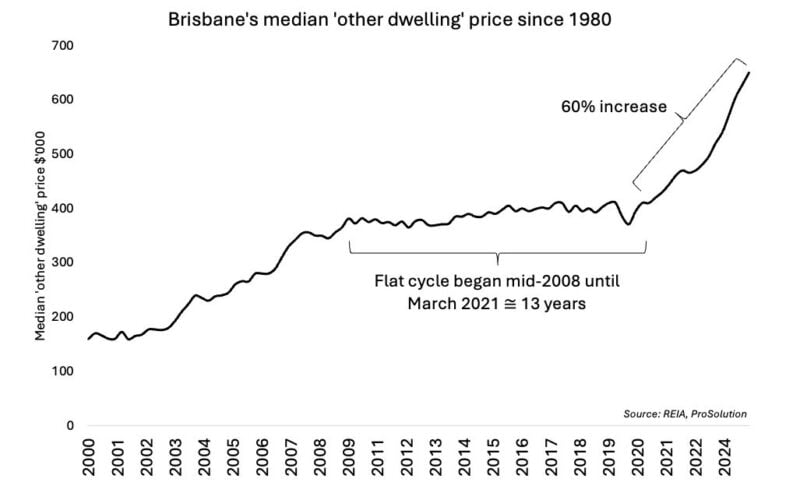

Brisbane apartments are case in point

The Brisbane apartment market endured a stagnant 13-year period from 2008 to 2021, primarily due to an oversupply of new apartments sold to overseas and interstate investors.

However, from March 2021 to December 2024, the median apartment price in Brisbane surged by nearly 60%.

This pattern is typical in property cycles: a flat phase lasting 7 to 15 years is often followed by a growth phase lasting approximately a decade.

Melbourne’s flat cycle

REIA data suggests Melbourne’s apartment market entered a flat cycle around June 2017, so it’s already been 7 years.

But that data includes all apartments, both new and established.

I would argue from my observations that the flat cycle for established apartments began more than 15 years ago, following the GFC.

That view is supported by the data: between mid-2009 and the end of 2024, Melbourne’s median apartment price has only increased by 3.1% p.a., which is barely above inflation at 2.7% p.a.

I hypothesise that the small amount of growth over this period was driven by the new apartment sales, not existing ones.

This prolonged 15-year period of underperformance suggests a turning point could be near.

A new growth cycle could be triggered by a combination of factors: strong relative value compared to houses and interstate markets, lower interest rates, and government incentives for first-home buyers.

A recent story from Jarrod McCabe’s podcast was quite intriguing.

He discussed a one-bedroom apartment in Hawthorn initially listed in the high $400,000s to low $500,000s.

Surprisingly, the auction drew a crowd of 60 people and concluded with a sale price of $670,000.

This transaction stands out because it’s one of the strongest results for an apartment sale that I can recall over the past decade.

While it’s just one sale, it could signal a shift in the market.