Key takeaways

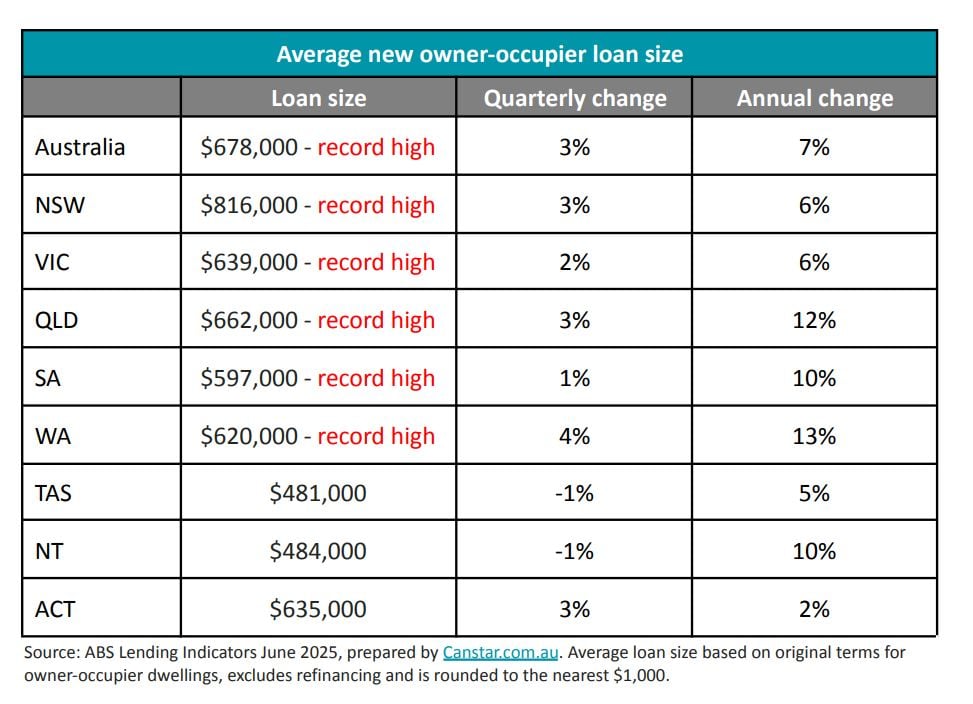

The average new owner-occupier loan size in Australia has hit a record $678,000, up $18,000 in just three months, equivalent to an extra $198 a day in borrowing capacity.

NSW remains the highest at $816,000, while WA saw the fastest growth (+4% to $620,000).

Increased borrowing power doesn’t always mean you should borrow to the max.

Always stress-test repayments at rates 3% higher than current to account for future rate rises.

A mortgage is a 30-year commitment, so factor in long-term financial stability.

The property market is getting a fresh shot of adrenaline.

According to new ABS Lending Indicator data, compiled by Canstar, the average new loan size for Australian owner-occupiers has hit a record high of $678,000, up $18,000 in just three months.

That’s effectively an extra $198 a day in borrowing power added over the June quarter.

NSW still leads with an average of $816,000, while Western Australia posted the fastest growth, up 4% in the quarter to $620,000.

Victoria, Queensland, and South Australia also set new records for average loan size.

Why borrowing power is climbing

The Reserve Bank’s February and May rate cuts were already pushing loan sizes higher, and the latest August 0.25% cut is set to turbocharge the trend.

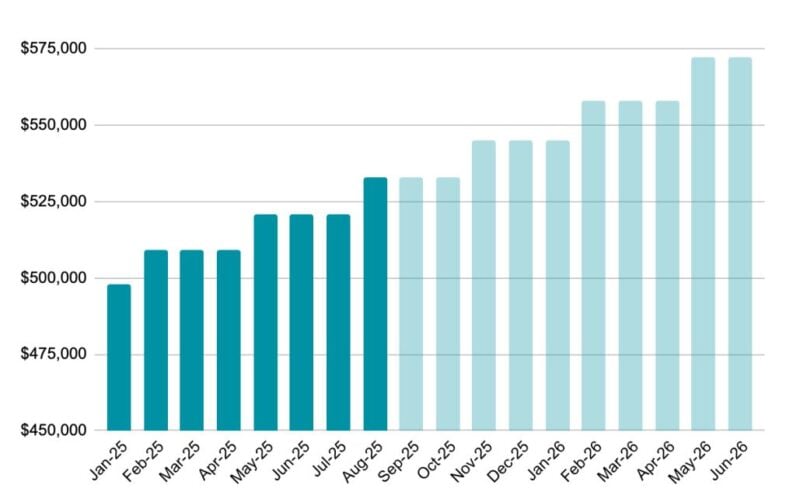

Canstar’s analysis shows a single person on the average full-time wage can now borrow around $12,000 more than before the cut.

Stack all three cuts together, and the average borrower has seen their borrowing capacity climb by $35,000 in just six months.

If Westpac’s forecast of three more rate cuts plays out, that could swell to $74,000 over the next 16 months.

More buyers, more competition

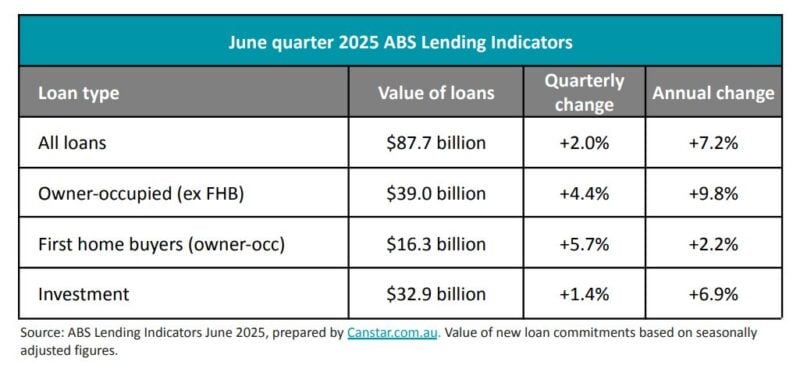

The total value of new housing loans rose to $87.7 billion in the June quarter, up 2% from the March quarter.

First-home buyers led the growth with a 5.7% increase, followed by upgraders (+4.4%) and investors (+1.4%).

And here’s the catch, when borrowing gets cheaper, people don’t just buy, they bid higher.

As Sally Tindall, Canstar’s data insights director, puts it:

- Also read:RBA raises interest rates again. Here’s what this means for property. | Property Insiders

- Also read:This week’s Australian Property Market Update – Latest Data, State by State March 24th 2026

- Also read:Latest Property Price Forecasts Revealed. Australian Property Market Outlook 2026: Where To Now After The Rate Rise.

- Also read:National Weekly Auction Report – March 21st 2026 | Auction Markets Down Again Following Latest RBA Rate Increase

- Also read:Perth housing market update | March 2026

“The RBA’s rate cuts are helping push new loan sizes to eye-watering levels…

When the cost of borrowing falls, some buyers use it to bid higher at auction, particularly in sought-after property hotspots. This is exactly what we’re seeing play out in the latest ABS data.”

She also cautions buyers not to get carried away:

“Just because the bank says you can borrow more money, doesn’t automatically make it a good idea.

Before you take out a new mortgage, check what your repayments might look like if interest rates rose by 3 percentage points… a home loan is for up to three decades and a lot can happen in this time.”

Investor takeaways

As borrowing power grows, so does competition for quality assets.

Strategic investors should act before the full impact of these cuts filters through prices, but with discipline.

Now’s the time to:

-

Focus on investment-grade properties in high-demand, supply-constrained locations.

-

Stress-test your finances at rates 3% higher than today’s.

-

Be prepared for competition from first-home buyers and upgraders flush with extra borrowing capacity.

With rate cuts back on the table, it’s clear we’ve entered a new phase of the property cycle.

The opportunity is real, but so is the risk if you stretch too far.

As always, those with a long-term strategy and a clear understanding of the market will be the ones who come out ahead.