Key takeaways

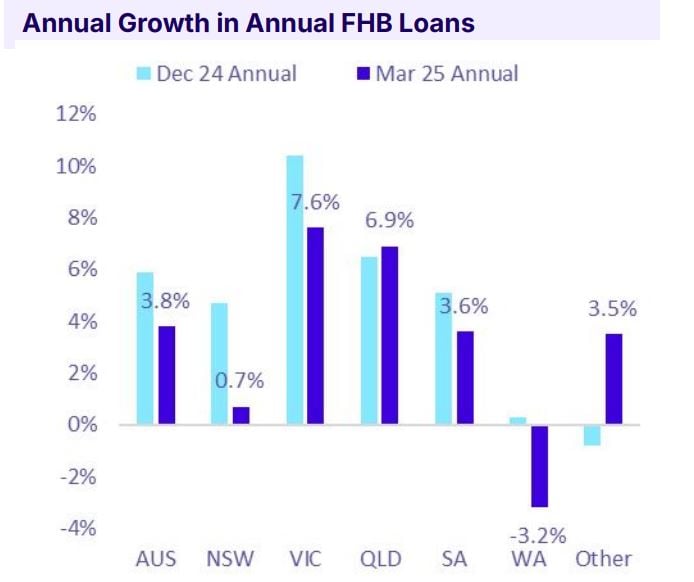

National FHB loan activity rose 3.8% year-on-year to March 2025, totalling 125,036 loans.

Although this growth is slower than the 5.9% gain to December 2024, it's still significant given ongoing affordability pressures and higher interest rates.

FHB loan volumes are now 9.1% above the September 2023 trough, which occurred during the RBA’s aggressive rate hikes — a signal that sentiment is stabilising.

Queensland was the only major state to see acceleration in FHB loan growth, up from 6.5% to 6.9%.

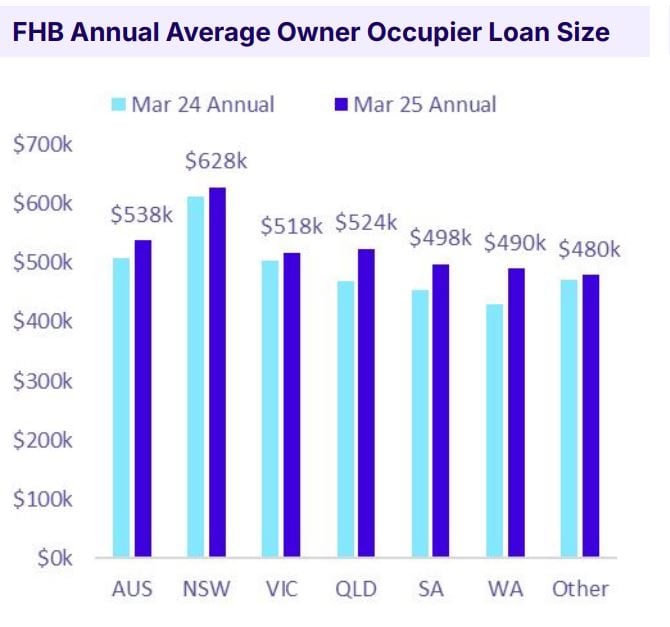

The average FHB loan size in Queensland rose by nearly $55,000 to $524,169, overtaking Victoria’s average of $517,930.

Despite the ongoing headwinds facing Australia’s housing market, particularly for first home buyers (FHBs), new data shows a flicker of resilience, and Queensland is leading the charge.

According to Money.com.au’s latest Mortgage Insights report, while FHB activity has slowed from the pace we saw last year, we’re still seeing signs of renewed momentum.

Across the country, 125,036 FHB loans were issued in the year to March 2025, a 3.8% rise on the previous year.

Yes, that’s softer than the 5.9% recorded to December 2024, but the fact that we’re even seeing growth is telling.

And here’s the most surprising part: FHB loan numbers are still sitting 9.1% above the low point recorded in September 2023, a time when the RBA was mid-cycle in its aggressive rate hiking agenda.

What’s driving the rebound?

The answer lies, at least in part, in government policy.

As Victoria McGavin from Money.com.au rightly pointed out:

"When governments put their money where their mouth is — via larger grants, broadened stamp duty concessions, or targeted schemes — it makes a genuine difference.

These incentives provide a much-needed tailwind for aspiring homeowners trying to crack into a tough market.

And while nationally the pace may be slowing, Queensland is bucking the trend in style.

Queensland emerges as a quiet achiever

According to the report, Queensland was the only major state to increase its annual FHB loan growth rate, from 6.5% to 6.9%.

That’s not just a statistical quirk, it’s a reflection of broader shifts we’re seeing on the ground.

Affordability in QLD remains relatively attractive compared to Sydney and Melbourne, and interstate migration continues to bolster demand.

Buyer sentiment is also stabilising as more first-timers adjust to the ‘new normal’ of higher rates.

Interestingly, Queenslanders are now borrowing more than their southern counterparts.

The average first home buyer loan in QLD has jumped nearly $55,000 in just a year, now sitting at $524,169, leapfrogging Victoria’s $517,930.

That’s a significant 11.7% increase year-on-year.

While Western Australia still leads in growth (up 14.1%), QLD’s rise in both volume and loan size suggests confidence is returning.

- Also read:RBA raises interest rates again. Here’s what this means for property. | Property Insiders

- Also read:This week’s Australian Property Market Update – Latest Data, State by State March 24th 2026

- Also read:Latest Property Price Forecasts Revealed. Australian Property Market Outlook 2026: Where To Now After The Rate Rise.

- Also read:National Weekly Auction Report – March 21st 2026 | Auction Markets Down Again Following Latest RBA Rate Increase

- Also read:Perth housing market update | March 2026

Victoria still tops the growth chart

Despite Queensland’s upswing, Victoria still holds the crown for overall FHB activity.

With 40,063 loans over the year (a 7.6% lift), it leads the pack, although growth has cooled from 10.4% previously.

Victoria also boasts the highest market share of FHBs among owner-occupiers, at 40.7%.

It’s clear that Victoria’s broad range of grants and incentives, along with a steady pipeline of new supply, is keeping the market appealing for young buyers.

A quiet revolution: the rise of first-time investors

One of the most fascinating shifts highlighted in the report is the growing appetite for rentvesting, where first-time buyers purchase an investment property while continuing to rent where they live.

While still a relatively small slice of the market, investor loans by FHBs now make up 6.3% of the total and are projected to hit 10% by 2035.

NSW is the hotspot for this strategy, accounting for over a third (34.7%) of all FHB investor loans, despite the growth rate cooling from last year’s highs.

This tells us something important — younger buyers are increasingly savvy.

They recognise that ownership doesn’t have to mean living in the property.

They’re looking at the tax advantages, the rental income potential, and the flexibility that comes with starting as an investor.

So, what does all this mean?

There’s no denying it, getting onto the property ladder remains a serious challenge for many Australians.

But this data shows that where opportunity exists, first home buyers are responding.

Queensland’s performance is a case study in how relative affordability, strong interstate migration, and a confidence rebound can combine to defy national trends.

Meanwhile, Victoria shows the enduring strength of policy support and demand fundamentals.

And as more young Aussies explore rentvesting and strategic investing as a pathway to wealth, we’re seeing a subtle, but important, evolution in how the next generation approaches property.

For seasoned investors, this shift should be on your radar.

Today’s first home buyers are tomorrow’s competition for quality assets, and increasingly, they’re entering the market with sharper strategies, bigger loans, and greater resilience.