Key takeaways

Nationally loan numbers remain below pre-rate-hike peaks, but the average loan size has risen 8% year-on-year, showing buyers are borrowing more even though there aren’t more of them.

Queensland is the clear standout, recording the highest growth in both homebuyer and investor loans. Growth is broad-based across all categories, signalling genuine, sustainable demand rather than speculative activity.

New South Wales: Still the nation’s largest loan market, with investors driving demand. Investor lending is growing six times faster than homebuyer lending, highlighting affordability pressures for first-home buyers.

Victoria: Showing modest, steady growth. Lending for land and new builds has dropped sharply, suggesting buyers prefer established properties. Price growth here is less volatile, offering more stability for long-term investors.

South Australia: Leading in construction and new dwelling loans, with lending for new homes surging over 50%. Strong activity in both owner-occupier and investor segments shows robust demand.

Western Australia: After years of strong growth, the market is cooling and consolidating. Lending volumes are flat, but refinancing, land, and renovation loans remain strong as homeowners optimise and improve existing properties.

Over the years, I've found that lending activity often reveals more about the direction of our property markets than price movements alone.

And right now, the latest state-by-state mortgage lending report from Money.com.au reveals some fascinating insights.

While Queensland continues to lead the charge with broad-based growth, Western Australia is showing signs of slowing after several years of substantial gains.

Understanding these shifts is crucial for both investors and homebuyers, because lending growth (or contraction) is often the early signal of where the next opportunities, and risks, may lie.

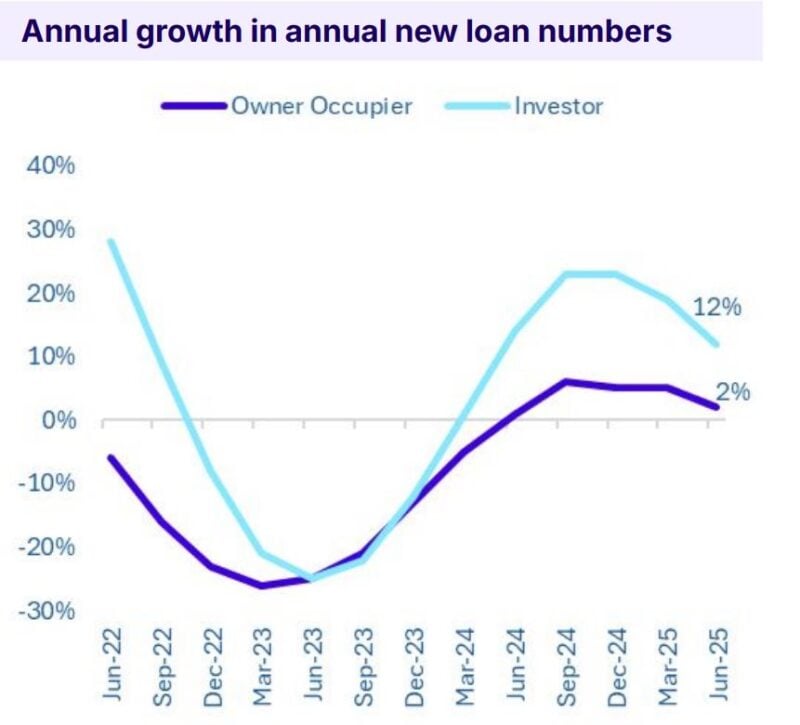

The national picture: bigger loans, not more loans

According to the Money.com.au report, loan numbers across Australia remain well below the highs we saw before the Reserve Bank’s aggressive rate hikes.

Owner-occupier loans are still down by almost 20% compared to mid-2022, and investor loans are only just below their previous levels.

But here’s the kicker: while volumes are sluggish, loan sizes are on the rise—up 8% nationally over the past year.

In other words, people are borrowing more, but there aren’t necessarily more buyers in the market.

This indicates that affordability pressures are still affecting buyers, yet demand remains strong enough, especially from investors, for them to stretch further. That’s especially evident in the eastern states.

New South Wales: investor-driven market

NSW remains the big-ticket market, with the largest average loan sizes in the country.

Investor appetite is outstripping homebuyer demand by a wide margin, with investor lending growing at six times the pace of owner-occupier loans.

What does this mean?

Investors remain confident in the long-term fundamentals of NSW, citing tight supply, economic resilience, and ongoing population growth.

However, for first-home buyers, it means increased competition and greater pressure on affordability.

Victoria: modest and stable

Victoria is moving at a slower pace.

Growth is steady but unspectacular, with modest increases in both owner-occupier and investor loans.

Interestingly, lending for land and new builds has dropped sharply, an indication that buyers are leaning toward established homes rather than committing to construction in an uncertain cost environment.

For investors, Victoria remains a market that is “slow and steady.”

It’s less prone to sharp upswings, which can provide confidence for those who prefer long-term stability over chasing momentum.

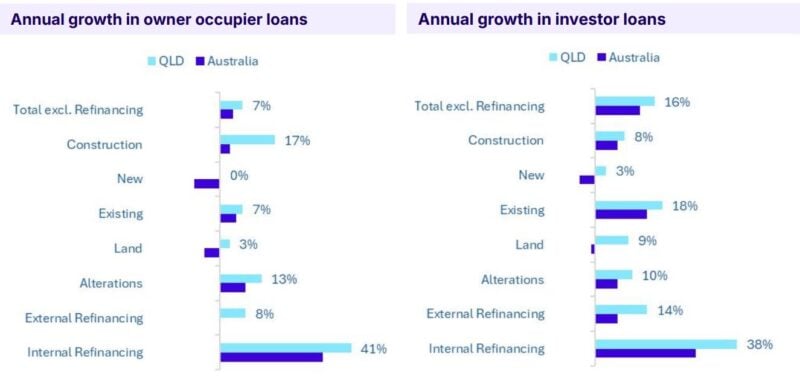

Queensland: the standout performer

Queensland is again proving to be Australia’s property hotspot.

Both owner-occupier and investor lending recorded the strongest growth among major states, supported by population growth, lifestyle appeal, and a resilient economy.

- Also read:RBA raises interest rates again. Here’s what this means for property. | Property Insiders

- Also read:This week’s Australian Property Market Update – Latest Data, State by State March 24th 2026

- Also read:Latest Property Price Forecasts Revealed. Australian Property Market Outlook 2026: Where To Now After The Rate Rise.

- Also read:National Weekly Auction Report – March 21st 2026 | Auction Markets Down Again Following Latest RBA Rate Increase

- Also read:Perth housing market update | March 2026

Crucially, this growth is broad-based.

Every loan category, from construction to existing dwellings, is in positive territory. That suggests Queensland’s momentum isn’t a speculative bubble but reflects genuine, sustainable demand.

Investors should take note: when growth is spread across categories, it signals depth in the market.

South Australia: building boom

South Australia is leading the nation when it comes to construction and new dwellings.

Lending for new homes surged more than 50%, while construction loans climbed 20%.

This signals a market underpinned by new supply, which could help ease future affordability pressures.

For investors, it presents opportunities in new builds and development, although careful due diligence is required due to building cost volatility.

Western Australia: cooling after the boom

After years of rapid gains, WA is cooling.

Homebuyer lending was flat, and investor activity has slowed compared to the national average.

But it’s not all doom and gloom.

WA leads the nation in refinancing activity, as savvy owners and investors optimise their loans in a higher-rate environment.

There’s also strength in land and alteration loans, which suggests locals are investing in improving or expanding their existing homes rather than entering new purchases.

It’s a classic consolidation phase after a boom, where the smart money quietly repositions.

Tasmania: a mixed story

Tasmania is showing an interesting split.

Owner-occupier lending is up strongly, with double-digit growth, but investor lending lags well behind.

Still, niche opportunities exist, particularly in land loans, which recorded the strongest growth of any state.

Selective investors may still find value here, but it’s not a broad-based growth story.

The bottom line

This report paints a clear picture: Queensland and South Australia are markets of genuine demand, NSW is still dominated by investors, Victoria offers stability, while WA is entering a consolidation phase.

For savvy investors, the lesson is clear: follow the lending trends, because they often foreshadow price movements.

Right now, Queensland stands out as the state with the strongest fundamentals, not just hype.

And as always, those who buy strategically, with a long-term view, will be best positioned to ride the next wave of growth.