Key takeaways

There's growing political and media noise around property investors being blamed for housing affordability issues.

But much of this narrative doesn’t hold when you examine the actual data.

Facts, not opinions, reveal a more nuanced and grounded reality.

Most property investors in Australia are everyday people—working Australians building financial security.

The idea that they're to blame for housing unaffordability is not just wrong, it’s counterproductive. Policy responses should be based on facts, not populism.

There’s a lot of noise about property investment at the moment.

No surprises here, really.

The recent federal election results, the chronic tightness in Australia’s rental market, and the looming spectre of changes to property taxation from the Labor government (with the Greens cheering them on and a weak opposition offering little resistance) have turned property investment into a political football.

I don’t want to join the noise.

But when the air is thick with speculation and misinformation, I like to cut through it by returning to the numbers.

Because numbers don’t have a political agenda.

So let’s ask the question: just how many Australian households own an investment property? And who are these people, really?

The big picture: property ownership in Australia

According to the latest ABS and ATO data:

- Australia has approximately 10 million dwellings

- Of these, around 2.2 million dwellings are held by property investors.

- This means roughly 22% of Australian households own at least one investment property, while 78% do not.

In other words, despite the political narrative that investors are snapping up all the homes and driving up prices, four out of five households aren’t even in the game.

Who are these property investors?

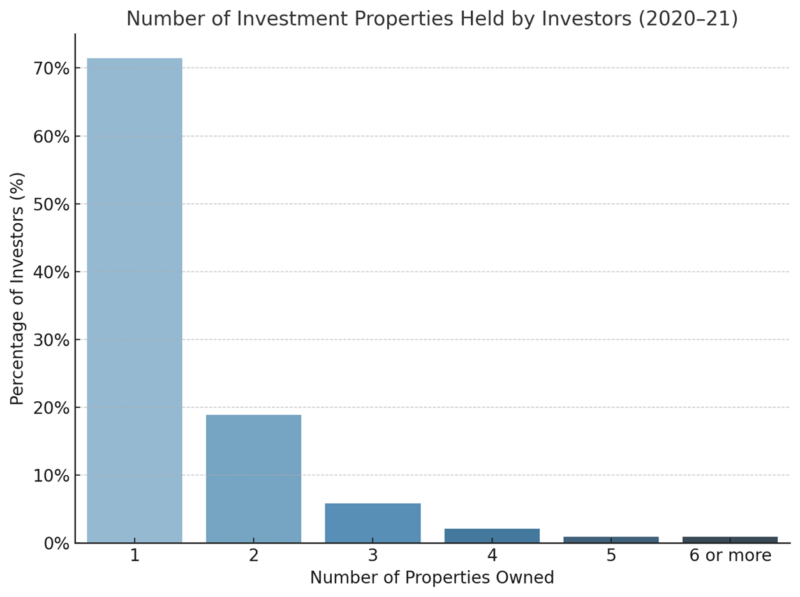

Total Number of Property Investors:

Approximately 2,245,539 Australians owned at least one investment property in 2020–21, according to the ATO.

- 71.48% of investors hold 1 investment property

- 18.86% of investors hold 2 investment properties

- 5.81% of investors own 3 investment properties

- 2.11% of investors own 4 investment properties

- 0.87% of investors own 5 investment properties

- 0.89% (or 19,920) of investors hold 6 or more investment properties.

These figures indicate that the majority of property investors in Australia are small-scale, with nearly three-quarters owning just one investment property.

Only a small fraction (less than 1%) own six or more properties, challenging the perception that most investors are large-scale landlords.

By Household Income

- Also read:March Home Prices Still Rising | Latest stats from Dr. Andrew Wilson

- Also read:Melbourne property market forecast for 2026 | Is it a good time to invest in Melbourne?

- Also read:Latest Property Price Forecasts Revealed. Australian Property Market Outlook 2026: Where To Now After The Rate Rise.

- Also read:Brisbane Property Market Forecast [2026] – What’s Ahead & Where to Invest

- Also read:Sydney property market forecast for 2026. Is it a good time to invest in Sydney?

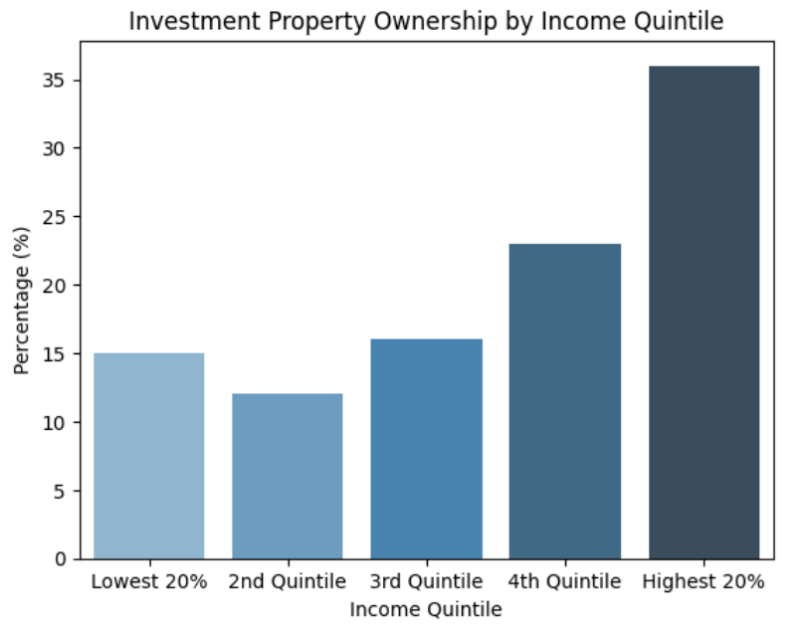

Property investment isn’t just the domain of the ultra-wealthy:

- 15%are in the lowest 20% income bracket.

- 12% in the second quintile (20-40%).

- 16% in the middle (40-60%).

- 23% in the fourth quintile (60-80%).

- 36% are in the highest 20% of income earners.

Yes, higher-income Australians are more likely to invest in property, but over half of all investors are outside the top 20%.

By Age

Property investment also skews towards older Australians, which makes sense given equity and borrowing capacity:

- 25% of investors are aged 55-64.

- 23% are 45-54.

- 22% are 35-44.

- 13% are under 34 years of age.

This highlights that property investment is often a long-term play, with most investors entering the market later in life.

This shows that most investors are ‘mum and dad’ types with just a single property.

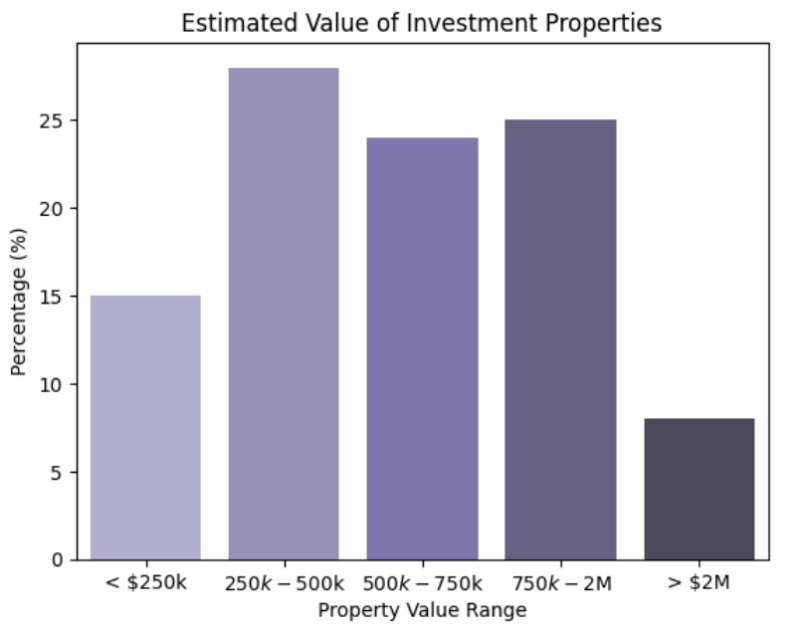

What are their properties worth?

In today’s dollars, investors perceive their property values as:

- 15% under $250,000.

- 28% between $250,000 - $500,000.

- 24% between $500,000 - $750,000.

- 8% over $2 million.

So the majority of investment properties sit in the lower to mid-price ranges, not luxury homes.

Cutting through the noise

When politicians or commentators suggest investors are the villain of the housing market, remember:

- Most investors only own one property.

- A large portion are middle-income earners.

- Many are approaching retirement age and building a nest egg.

The narrative that investors are hoarding homes and pushing prices out of reach for first-home buyers just doesn’t stack up against the numbers.

What’s really needed is a nuanced conversation about housing supply, planning reform, and incentivising the right kind of investment to grow our rental stock.

Because as always, the numbers tell a different story than the headlines.