Key takeaways

From 5 December 2025, eligible Australians can buy a home with the federal government contributing up to 30% for existing homes and 40% for new builds.

In return, the government becomes a co-owner, meaning it shares in both costs and future profits.

The scheme is capped at 10,000 places per year, with income limits of $100,000 for singles and $160,000 for couples or single parents.

Participants only need a 2% deposit and won’t pay lenders’ mortgage insurance (LMI), but they can only borrow through CBA or Bank Australia for now.

Because the government covers part of the purchase price, buyers take on smaller loans and lower repayments, making loan approval easier.

However, if their income rises above the cap for two consecutive years, they must buy back part of the government’s share, and the government will also take a share of any capital gain when the property is sold.

While Help to Buy will get some Australians into the market, it doesn’t address the underlying issue — the lack of housing supply.

Without more construction and planning reform, affordability challenges will persist. The scheme helps individuals, but not the broader market.

Starting last Friday, thousands of Australians who’ve been stuck renting might finally get a crack at owning their own home.

The Federal Government’s long-awaited Help to Buy scheme officially launched, a policy that’s been on the cards since 2022 and is being pitched as "a lifeline for those locked out of the market."

But while the headlines sound promising, it’s worth asking: how much help does this scheme really offer, and what’s the catch?

Help to Buy is designed to make ownership more accessible by allowing low and middle-income households to co-purchase a home with the government.

The government contributes up to 30% of the cost for an existing home and up to 40% for a new build.

In return, they become a co-owner, meaning they’ll share in both the costs and the profits when the property is eventually sold.

Participants only need a 2% deposit and won’t have to pay lenders’ mortgage insurance (LMI), which can often run into tens of thousands of dollars.

It’s available to singles earning up to $100,000, or couples and single parents earning up to $160,000 combined.

However, places are capped at 10,000 per year, and only two lenders, CBA and Bank Australia, are currently participating.

The upside: smaller loans and bigger opportunities

The big appeal of Help to Buy is that it dramatically reduces the size of the mortgage needed.

By having the government cover up to 40% of the property’s value, borrowers will face much smaller repayments, making it easier to get loan approval and manage repayments without overextending themselves.

As Canstar’s Data Insights Director, Sally Tindall puts it:

“Help to Buy could well be a lifeline for people who’ve been watching the first rung on the property ladder rise further out of reach.

For some, this scheme will be the difference between renting indefinitely and finally getting the keys to their own home.”

She’s right, for many Australians, particularly lower-income earners, even scraping together a 5% deposit can feel impossible.

Help to Buy provides that critical stepping stone, offering an entry point into a housing market that’s left many behind.

The flip side: strings attached

Note: However, this isn’t free money. It’s shared equity, and with that comes shared responsibility.

When the property is sold, the government will take its cut of the profit.

If your income rises above the eligibility threshold for two consecutive years, you’ll be asked to buy back part of the government’s share.

Borrowers will also face limited lender choice, given that only two banks are currently participating.

- Also read:March Home Prices Still Rising | Latest stats from Dr. Andrew Wilson

- Also read:Latest Property Price Forecasts Revealed. Australian Property Market Outlook 2026: Where To Now After The Rate Rise.

- Also read:National Weekly Auction Report – March 28th 2026 | Auction Clearance Rates Still Fading Over Super Week of Listings

- Also read:RBA raises interest rates again. Here’s what this means for property. | Property Insiders

- Also read:This week’s Australian Property Market Update – Latest Data, State by State March 24th 2026

And if property values fall, owners could find themselves stuck in a co-ownership arrangement longer than they’d like.

As Ms Tindall cautions:

“Shared equity gives people a foot in the door, but it comes with some pretty significant strings attached... It’s not going to suit everyone who’s eligible.”

That’s an important point. Many buyers focus on the dream of ownership without fully considering what co-ownership really means, especially when your “partner” in the property is the federal government.

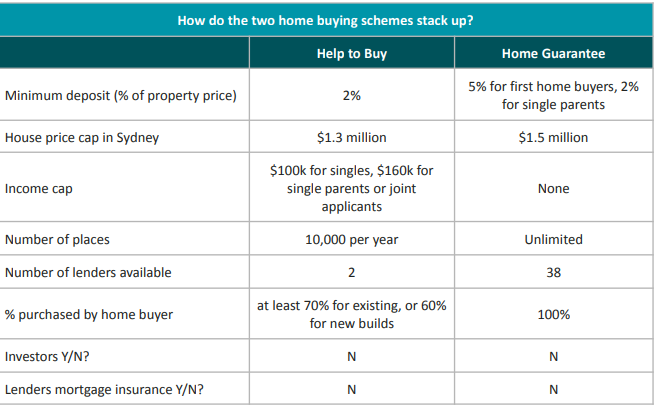

How it stacks up against the Home Guarantee Scheme

The Help to Buy program sits alongside the existing Home Guarantee Scheme, but the two work quite differently.

The key difference?

With Help to Buy, you’re not taking out a bigger loan, you’re taking on a smaller one, because the government owns part of your home. That means lower repayments, but also less autonomy.

The bigger picture: a step forward, but not a solution

There’s no doubt Help to Buy will open the door for some Australians who’ve been priced out of the market.

As Ms Tindall points out:

“Help to Buy will get more people into the market, but again, it does nothing to fix the structural affordability issues facing the country. It’s a helping hand for tens of thousands of households – not a silver bullet.”

And that’s the real story here.

While the scheme will ease the path for a small number of buyers, it doesn’t tackle the fundamental problem: housing supply.

We’re still not building enough homes where people want to live, and until we address that, affordability will remain a national challenge.

So yes, Help to Buy might help some renters finally become homeowners.

But it’s a short-term fix for a long-term crisis.

The real solution lies in tackling the planning bottlenecks, incentivising construction, and making it easier, and faster, to bring new housing to market.

Until then, schemes like this will remain just that, helpful, but not transformative.