Key takeaways

First home buyer numbers lift 6.8% on back of Home Guarantee expansion.

Average new loan size for owner-occupier hits record high of $736,000.

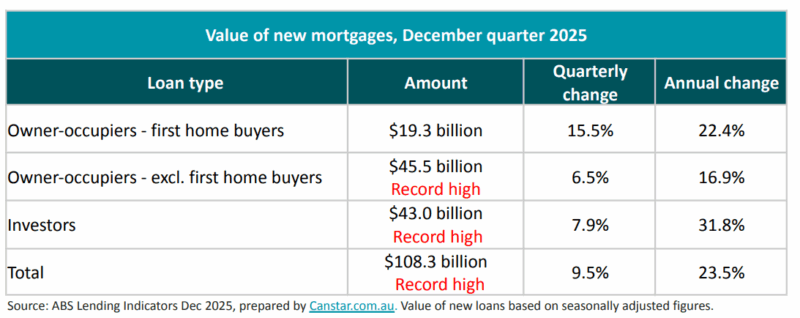

Investors break records of their own with $43 billion in loans in the quarter.

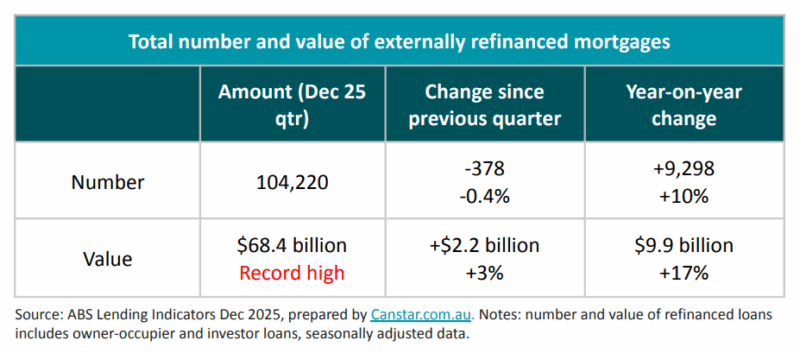

Refinancing hits new record high of $68 billion.

If you’ve been wondering who’s really driving Australia’s property market right now, the latest lending figures give us a very clear answer.

First home buyers are making a comeback.

But here’s the twist… they’re coming back armed with bigger loans than ever before, in a market where investors are also doubling down and refinancing activity has hit record highs.

In other words, this isn’t just a rebound, it’s a surge in borrowing power across the board.

Let’s look at what’s really going on and what it means for property values, investors, and the next generation trying to get a foothold.

First home buyers: a strong rebound

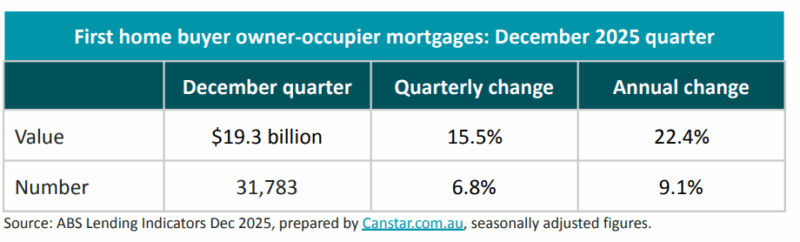

According to the latest ABS Lending Indicators, the value of first home buyer loans jumped 15.5% in the December 2025 quarter to $19.3 billion, the second-highest result on record.

The number of loans rose 6.8% over the quarter to 31,783.

That’s the highest level since March 2022, and it comes on the back of the federal government’s expansion of the Home Guarantee Scheme.

Canstar’s Sally Tindall summed it up well:

“The expansion of the Home Guarantee scheme has fired up the first home buyer market, with thousands more securing a foot on the property ladder in the space of three months."

And the impact is being felt across the states, particularly in NSW, WA and the ACT, which saw the largest quarterly lifts in first home buyer activity.

But what many commentators are missing is that this isn’t just about more buyers. It’s about more debt.

Loan sizes have smashed records

The average new loan size for owner-occupiers has reached a record $736,000. That’s up $42,000 in just one quarter

In other words, debt levels aren’t just creeping up, they’re accelerating.

NSW now has an average new loan size of $873,000

Western Australia recorded the biggest percentage jump, up 9% in a single quarter.

Ms Tindall further said:

“It’s absolutely no surprise or coincidence that the average new loan size for owner-occupiers has hit a new record high – rising by a hefty $42,000 in the space of three months.

“The average new loan size for an owner-occupier now sits at an astronomical $736,000. That’s not the property price, but the size of the debt people are agreeing to take on.”

When governments expand guarantees and the RBA cuts rates (as we saw through 2025), borrowing capacity increases.

And in property markets, increased borrowing capacity almost always translates into higher prices.

It’s not complicated.

More money chasing limited stock pushes values up.

Investors aren’t stepping back, they’re stepping in

Interestingly, investors haven’t been scared off by this wave of first home buyers.

Note: In fact, investor lending hit a record $43 billion in the quarter, up 7.9%.

Total new mortgage commitments across the market reached a record $108.3 billion.

Ms Tindall noted:

- Also read:RBA raises interest rates again. Here’s what this means for property. | Property Insiders

- Also read:This week’s Australian Property Market Update – Latest Data, State by State March 24th 2026

- Also read:Latest Property Price Forecasts Revealed. Australian Property Market Outlook 2026: Where To Now After The Rate Rise.

- Also read:National Weekly Auction Report – March 21st 2026 | Auction Markets Down Again Following Latest RBA Rate Increase

- Also read:Perth housing market update | March 2026

“Investors haven’t been deterred by this fresh wave of new property owners – they’re buoyed by it - because more buyers typically equals greater opportunity for capital growth.”

And she’s right. Seasoned investors understand market cycles.

They recognise that increased first home buyer activity often signals the early stages of broader momentum building in the market.

It improves liquidity. It underpins demand.

And in tightly held markets, particularly our major capitals, that supports capital growth.

Refinancing at record highs

Refinancing of loans also hit a record $68.4 billion in the quarter.

Even though the number of loans switching lenders dipped slightly, the value surged because Australians are carrying much larger mortgages.

As Ms Tindall pointed out:

“RBA hikes are usually an even bigger motivator than cuts. This latest increase should encourage greater switching and a corresponding step up in competition in the market."

This tells that households are actively managing debt, which is critical in a higher-rate environment.

The bigger picture: what this really means

Let me give you my take.

-

Government incentives increase demand, not supply.

Expanding the Home Guarantee scheme makes it easier to buy, but it doesn’t build more homes. -

Borrowing capacity drives price growth.

When rates fall or guarantees expand, buyers can borrow more. Prices adjust accordingly. -

Debt levels are becoming generational.

A $736,000 average loan represents a long-term financial commitment that will shape household spending, savings and investment behaviour for decades. -

Investors understand the structural drivers.

Population growth, chronic undersupply, and improved borrowing capacity form a powerful combination.

The real risk is that those who delay may find themselves further behind if prices continue rising on the back of expanded borrowing power.

A word of caution

While incentives help people get into the market with smaller deposits, they don’t reduce the size of the commitment.

As Ms Tindall warned:

“While the federal scheme makes it easier for many first home buyers to get on the ladder with a small deposit, it certainly doesn’t mean the commitment and responsibility of repayments is any easier.”

That’s an important point. Buying with a 5% deposit is not the same as buying comfortably.

Financial buffers, income resilience, and long-term planning matter more than ever.

In my view, this data reinforces a theme we’ve been discussing for some time: structural demand remains strong, and policy settings are supportive of continued growth.

The key isn’t whether the market moves. It’s whether you’re positioned correctly.

Strategic property selection, conservative debt structuring, and a long-term wealth plan will matter far more than chasing short-term headlines.

Because in the end, property markets reward preparation, not reaction.