Key takeaways

Each round of rate cuts since 2015 has benefited entirely different segments of the housing market, depending on affordability, demographics, and economic conditions.

Rate cuts alone don’t guarantee growth everywhere. The winners shift based on affordability, stimulus, and buyer profiles.

Smart investors look beyond history and focus on who stands to gain in the current environment.

If there’s one thing property investors learn over time, it’s that no two cycles are ever the same.

The past decade has reminded us of this lesson again and again.

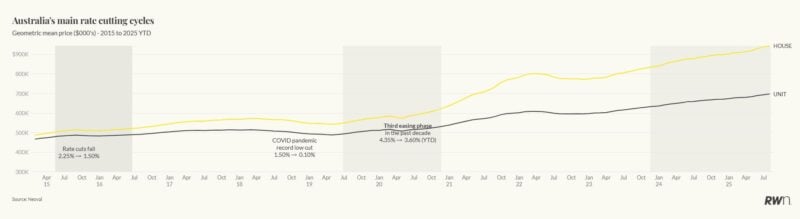

Since 2015, Australia has been through three major interest rate cutting cycles.

Each of these has played out very differently, with entirely different market segments benefiting depending on the broader economic backdrop and who was active in the market at the time.

As Ray White's Chief Economost Nerida Conisbee has noted: “Every cycle is different.”

And the way buyers respond to interest rate cuts is shaped just as much by affordability and demographics as it is by the cost of money itself.

Let’s take a look at a recent report by Nerida Conisbee explaining how these cycles unfolded—and more importantly, what lessons we can draw for the future.

Source: Ray White

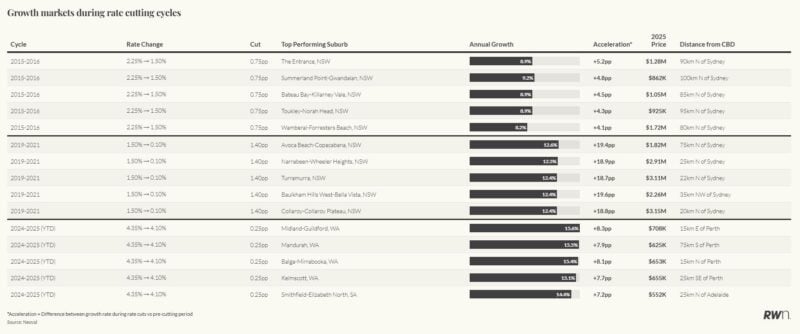

The First Cycle (2015–2016): coastal lifestyle markets rise

When the RBA eased rates from 2.25% down to 1.50% between May 2015 and May 2016, the biggest winners weren’t blue-chip suburbs but affordable coastal lifestyle locations close to Sydney.

The Central Coast was the standout, with Avoca Beach–Copacabana (8.0%), Wamberal–Forresters Beach (8.2%), and The Entrance (8.9%) all showing strong growth.

Conisbee explains:

“This was when the lifestyle shift really began.

People were seeking coastal living within commuting distance, and cheaper borrowing costs made that possible well before COVID accelerated the trend.”

These markets, priced between $800,000 and $1.2 million at the time, highlight how rate cuts can amplify emerging lifestyle preferences.

The next phase was far more aggressive according to Conisbee.

From mid-2019 through the pandemic, rates plunged from 1.50% to just 0.10%.

This time, the response was concentrated in Sydney’s premium suburbs.

Castle Hill, Baulkham Hills West–Bella Vista, and Northern Beaches areas like Collaroy and Freshwater all recorded double-digit growth.

Baulkham Hills West–Bella Vista alone swung from -7.2% to +12.4% growth, a 19.6 percentage point acceleration.

According to Conisbee:

“Ultra-low rates and fiscal stimulus created a pronounced wealth effect.

Established property owners, particularly in Sydney’s premium markets, were able to upgrade or expand their portfolios.

It wasn’t first home buyers driving this cycle, it was the affluent.”

This was a clear reminder that rate cuts don’t always make property more accessible, they can just as easily amplify demand where wealth is already concentrated.

Source: Ray White

The Third Cycle (2024–2025): affordable outer suburbs take the lead

Fast forward to today, and we’re in another cutting cycle; this time from the highest interest rates seen in over a decade.

But instead of boosting premium markets, affordability has become the driving factor.

Perth’s Midland–Guildford (15.6%), Mandurah (15.5%), and Balga–Mirrabooka (15.4%) are leading national growth.

In Adelaide, Smithfield–Elizabeth North is up 14.4%.

These are outer suburban markets priced between $550,000 and $750,000—very much first home buyer territory.

- Also read:Melbourne property market forecast for 2026 | Is it a good time to invest in Melbourne?

- Also read:Latest Property Price Forecasts Revealed. Australian Property Market Outlook 2026: Where To Now After The Rate Rise.

- Also read:Brisbane Property Market Forecast [2026] – What’s Ahead & Where to Invest

- Also read:Sydney property market forecast for 2026. Is it a good time to invest in Sydney?

- Also read:March Home Prices Still Rising | Latest stats from Dr. Andrew Wilson

Conisbee notes:

“Unlike the COVID cycle, today’s cuts are most effective for buyers on the margins of borrowing capacity.

Affordable outer suburbs are where interest rate reductions translate directly into stronger demand.”

In other words, the affordability crisis has fundamentally reshaped who benefits when monetary policy loosens.

The consistent performers

While the beneficiaries have shifted from lifestyle seekers, to wealthy upgraders, to first home buyers, some regions have shown enduring sensitivity to rate cuts.

Conisbee highlights:

“The Central Coast is fascinating. Across all three cycles, it’s shown consistent growth.

That tells us some markets retain a structural advantage, whether that’s lifestyle appeal, location, or ongoing affordability relative to Sydney.”

Key lessons for investors

What should investors take away from this decade-long story?

-

Each cycle has its own winners. As Conisbee says, “We can’t assume that because one group benefited in the past, they’ll benefit again.”

-

Affordability now matters more than ever. Today’s rate-sensitive suburbs are not the million-dollar enclaves, they’re the $550k to $750k markets.

-

Some markets have lasting resilience. Places like the Central Coast show that structural appeal can cut across multiple cycles.

-

Context is everything. Fiscal stimulus, global shocks like COVID, and demographic shifts shape how rate cuts flow through the market.

Final thoughts - a new window of opportunity

The past decade of rate cycles proves just how dynamic and unpredictable Australia’s property market really is.

Conisbee sums it up well:

“Every cycle is different.

The beneficiaries shift depending on affordability, economic conditions, and who’s active in the market.

Understanding that context is critical for investors.”

As we look ahead, it’s clear that today’s easing is delivering the greatest benefits to outer suburban, affordable markets.

That’s a profound shift from the wealth-driven gains of the COVID cycle, and a reminder that strategy, not just timing, is what separates smart investors from the rest.

However, one thing is clear: there's currently a window of opportunity for property investors with a long-term focus.

Right now, we’re seeing what some would call a “perfect storm” of fundamentals that are aligning to support strong property markets in the years ahead:

- Continued rapid population growth is putting pressure on housing.

- An acute undersupply of dwellings,

- A chronic shortage of skilled labour, making new development slower and more expensive.

- Inflation has moderated, now sitting within the RBA’s target range.

- Interest rates will keep falling – bringing more buyers into the market

- Government first homebuyer incentives will pour fuel on the flames of our undersupplied housing market.

As interest rates keep falling and confidence returns among both buyers and sellers, we’ll enter the next phase of the property cycle.

And historically, this stage has delivered some of the best capital growth for those who act early.

Are you clear on how to take advantage of these market conditions — or are you still waiting for "certainty"?

That’s where our Complimentary Wealth Discovery Chat comes in. We’re offering you a 1-on-1 chat with a Metropole Wealth Strategist to help you:

- Clarify your financial goals

- Understand how macro trends affect your position

- Build a personalised, data-driven property strategy

- Get ahead of the curve — before everyone else piles in

There’s no cost, no obligation — just practical, tailored guidance based on decades of experience.

Click here now to book your free Wealth Discovery Chat