The Senate committee reviewing the CGT discount released its final report yesterday. Commentators are now suggesting the government could reduce the CGT discount for property investors and potentially cap negative gearing to two or three properties.

Let’s look at the impact a change to the CGT discount could have.

Why is CGT under the microscope?

The government agreed to establish a Senate committee to investigate how the capital gains tax (CGT) discount operates.

The Greens have made three main claims about the discount.

Claim 1: Is the CGT discount inflating house prices?

The argument is that the discount attracts more investors, which increases competition for homes and, in turn, pushes up prices for owner-occupiers.

Independent modelling from institutions like the Grattan Institute conclude that tax settings like CGT (including the discount) can be price-inflationary, but only at the margin.

The dominant driver of property price inflation is the structural imbalance between housing supply and population-driven demand.

In other words: tax policy can move the dial a little, but supply constraints are the main cause of price inflation.

Claim 2: Does the discount mainly benefit the top 1%?

The Greens claim around 60% of the benefit of the CGT discount goes to the richest 1% of Australians, and the Parliamentary Budget Office has reportedly supported that data.

High-income Australians receive most of the “benefit” because they also pay most of the CGT in the first place.

Lower-income earners generally do not realise any material taxable capital gains, so they do not pay much CGT, and therefore do not “benefit” much from a discount on a tax they rarely incur.

Claim 3: The $247b “cost” – why headline numbers are misleading

The Greens also argue the CGT discount will cost $247 billion over the next decade in forgone revenue, implying that money could instead fund social and affordable housing.

The problem is that headline “cost” numbers assume the discount is reduced to zero and that behaviour does not change in response to removing the discount. That is not a realistic assumption.

If you materially increase CGT, people respond such a defer sales and reduce the amount of new capital they invest in the property market. Any serious estimate needs to incorporate those second-order effects.

If this reads like I am taking aim at the Greens’ assertions, that is because I am. Not for political reasons, but because I want this blog to stay anchored to evidence.

I have said before that Australia needs serious tax reform. And there are real levers government can pull to improve housing affordability.

The most important one is still the least glamorous: take meaningful steps to increase housing supply.

What is the likely impact of taxation changes

If the government changes CGT and that genuinely deters investors from owning residential property, the fallout is likely to land hardest on the people who can least absorb it.

Around a third of Australians rent. Not all renters can buy, and not all want to. Even with the most ambitious housing reforms, Australia will always have a large cohort of renters.

That matters because private investors supply 80%-85% of dwellings to renters.

If policy settings meaningfully reduce investor participation, the pool of dwellings available to rent is likely to shrink or at least grow more slowly than it otherwise would.

When rental supply tightens while demand stays broadly intact, the usual outcome is higher rents.

And renters are often highly sensitive to rent increases.

What happened in the UK provides a useful case study of how investor-focused tax changes can flow through to the rental market, which I’ll get to below.

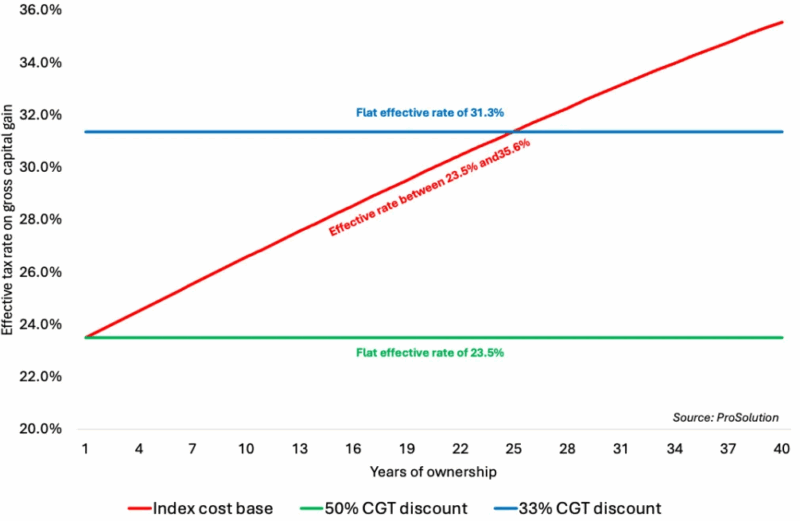

Comparing three CGT regimes

The chart below compares the effective tax rate on a gross (nominal) capital gain under three CGT regimes: the current discount model, a hypothetical 33% discount model, and the old cost-base indexation model that applied between 1985 and 1999.

The key assumptions are 6% p.a. for property price growth and 3% p.a. for inflation.

The key distinction is how each regime treats time.

Under the 33/50% discount models, the effective tax rate on the gross gain is essentially flat once the asset qualifies for the discount.

In other words, the tax outcome (as a share of the gain) does not materially change whether the property is held for a few years or a few decades.

Under the indexation model, the effective tax rate changes with the holding period because the cost base is adjusted for inflation; in the scenario illustrated in the chart, the effective rate increases the longer the investor holds the property.

This is a double-edged sword.

On one hand, it can disincentivise long-term investors who provide stable, long-term rental accommodation.

On the other hand, long-term investors are also the ones who benefit most from compounding capital growth.

They can arguably afford to pay a higher share of tax over time and still retain most of the capital growth in after-tax terms (often still around two-thirds, in broad terms).

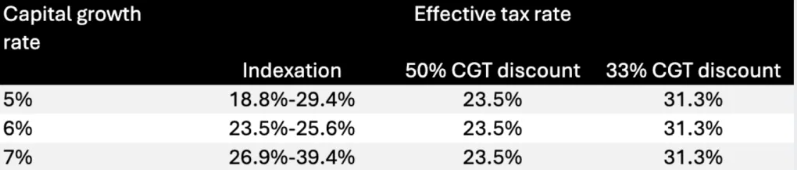

While the 33/50% discount models produce a flat effective tax rate, the indexation model behaves very differently depending on the assumed rate of property price growth.

The indexation model in place when CGT was first introduced in 1985 with a clear objective: tax people on real gains, not inflation.

In other words, it aimed to strip out the inflation component of asset price rises. That is a defensible approach, and it is why it is a useful benchmark to compare against.

What the indexation model shows is intuitive. When property price growth is low, the effective CGT rate is also low.

But as capital growth rises, the effective CGT rate increases as well, because more of the gain is “real” and therefore taxable.

This behaves much like the marginal income tax rate system.

To my mind, that does not feel unfair. If anything, it is arguably more rational than a flat effective tax rate that applies regardless of how strong the underlying capital growth has been.

Cutting the discount to 33%: how much does it really change?

I have used two measures to assess the impact of reducing the CGT discount from one half to one third.

The first is the internal rate of return (IRR). IRR tells you the after-tax return you earned relative to the cash you had to put in to keep the property running.

In my model, the investor borrows 100% of the purchase price.

- Also read:Melbourne property market forecast for 2026 | Is it a good time to invest in Melbourne?

- Also read:Latest Property Price Forecasts Revealed. Australian Property Market Outlook 2026: Where To Now After The Rate Rise.

- Also read:Brisbane Property Market Forecast [2026] – What’s Ahead & Where to Invest

- Also read:Sydney property market forecast for 2026. Is it a good time to invest in Sydney?

- Also read:Perth housing market update | March 2026

The only out-of-pocket cash contribution is covering the negative cash flow (after tax) across the entire holding period.

Therefore, the IRR is the return generated on the capital the investor has progressively contributed through those holding costs.

The second measure is the net present value (NPV) of the after-tax cash flows.

Put simply, it is the value today of what you end up with after selling the property in 30 years after subtracting how much the property has cost you to hold.

To calculate this, I start with the expected sale price in 30 years’ time, then subtract capital gains tax and the outstanding loan to arrive at net sale proceeds.

From that, I subtract the present value of the negative cash flow holding costs (the cash you contributed along the way).

In other words, NPV translates the whole investment into today’s dollars and shows how much profit it is expected to produce.

Here are the results:

- The IRR declines by 0.5% p.a. from 12.6% p.a. to 12.1% p.a., which is a 4% decline.

- The NPV declines by $180,000 from $1.535 million to $1.355 million, which is a 12% decline.

I think the most important measure is the NPV, because it is expressed in dollar terms and, at the end of the day, retirement is funded with dollars, not percentages.

On that basis, the change represents a meaningful reduction of around 12%.

That said, the case for borrowing to invest in property still largely holds.

The strategy works primarily because you are using leverage and benefiting from compounding capital growth, and those forces are still likely to make property an attractive long-term investment for many investors.

The key assumptions in my modelling were an $850,000 investment property, a starting 4% gross rental yield, and ongoing property expenses equal to 35% of gross rent.

I have assumed rental income grows at 4% p.a. and the property value grows at 7% p.a.

To compare apples with apples, I modelled the same leveraged strategy but, instead of buying a property, the investor borrows and invests in the share market.

To keep it like-for-like, I assumed the same return profile: 4% income and 7% capital growth.

I should add that an 11% total return assumption for shares is aggressive because they are more volatile, but that is not really the point, the goal is comparability so we can isolate the impact of tax.

On those assumptions, and assuming shares still retain the 50% CGT discount, the net present value was more than $2.3 million, substantially higher than the property outcome.

A big reason for this is that the portfolio income grows to cover the full interest cost after about 8 years, meaning the strategy becomes self-sustaining from that point.

Using more realistic rent assumptions, such as 2% income and 8% capital growth (which is not an unreasonable long-run expectation for a mostly global index portfolio), the net present value did not change much, coming in at around $2.4 million.

The difference is the cashflow profile: under these assumptions, the portfolio remains negatively geared for the first 16 years.

Of course, this all assumes an investor is willing to borrow $850,000 and invest it into the share market relatively quickly.

That is exactly what I will cover in a few weeks, including what the evidence says about lump-sum investing versus phasing in over several months, and practical ways to execute a plan like this.

Even with those caveats, the conclusion is clear: if the CGT discount is reduced for property, borrowing to invest in shares becomes materially more attractive than, particularly if the portfolio is structured to minimise income and maximise capital gains.

The company structure potential solution

Last year I wrote a blog about using a company to invest in property.

I outlined a structure that can still allow investors to benefit from negative gearing, while also changing how and when the capital gain is taxed.

The key advantage of a company is it can effectively allow a capital gain to be spread across multiple tax years.

In my modelling, that reduced the effective tax rate on the capital gain to around 14%, which is better than in personal names, even with the 50% discount.

The trade-off is complexity: borrowing through, or involving, a company is more difficult and not every lender will support it.

That said, the right structure could be a practical way to navigate any future reduction to the CGT discount.

The UK warning: tax policy that backfires on renters

A useful case study is the UK, where government intervention aimed at improving affordability has ended up squeezing private landlords.

First, the government reduced the tax value of interest deductions for landlords. Instead of deducting mortgage interest at your marginal tax rate, tax benefit was effectively capped at 20% of the interest cost.

That change makes negative gearing far less tax effective.

Second, it introduced a stamp duty surcharge on second homes and buy-to-let purchases of 5%, increasing the upfront cost of investing.

Third, tenancy rules have been tightened in ways that materially reduce a landlord’s control and certainty, like they have here.

The direction of reform has been to make tenancies more open-ended and to restrict a landlord’s ability to end an agreement.

No-fault evictions have been wound back, meaning landlords generally need a specific reason to regain possession (for example, selling the property, moving in, or responding to a serious breach such as persistent rent arrears), and notice requirements have become more onerous.

The practical effect is simple: more risk, less flexibility, and less confidence about whether your property will be occupied, and on what terms.

Put those together and the investment equation changes. After-tax returns are lower, transaction costs are higher, and regulatory risk is higher.

It is not surprising that many private investors have exited the market, shrinking the supply of rental properties.

In 2025, an average of 21 prospective tenants reportedly competed for each available rental in the UK, and rents rose a total of 18% between 2017 and 2023.

The kicker is that home ownership has not meaningfully improved. Over the past decade it has remained relatively stagnant, despite all the policy effort aimed at “affordability”.

Let us be honest: this is about revenue, not home ownership

If the government reduces the CGT discount, it will reduce the effectiveness of borrowing to invest in property as a wealth-building strategy. B

ut it is unlikely to be enough, on its own, to make the strategy unattractive.

For investors who are comfortable borrowing meaningfully and can tolerate market volatility, gearing into the share market can become comparatively more compelling, particularly when it is implemented with proper portfolio construction, risk management and the guidance of a reputable financial adviser.

Now, let us be frank about what tax changes are likely to achieve.

They will almost certainly not lift home ownership rates in Australia in any meaningful way.

What it is more likely to do is reduce the supply of rental housing over time and consequently push rents higher.

So, let’s be frank about the real motivation: the primary effect of these measures is higher tax revenue to help fund ever-expanding government spending.