Key takeaways

Dr Shane Oliver highlights that housing affordability has never been worse, with the ratio of home prices to incomes and the time needed to save a deposit both at historically high levels.

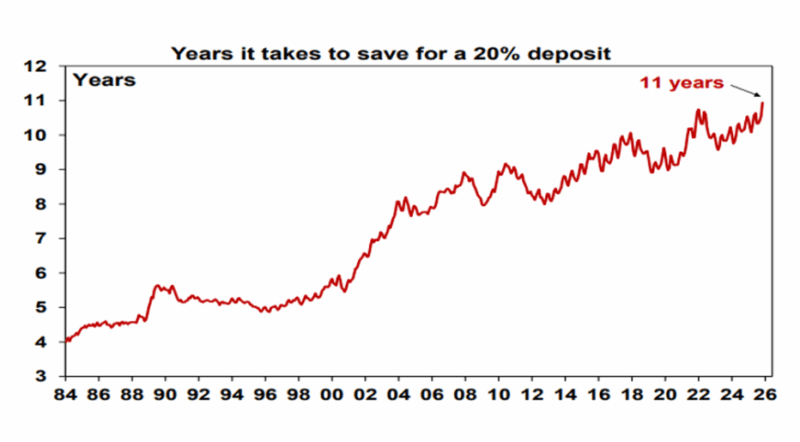

It now takes over 11 years to save a 20% deposit in many markets, double what it took in the early 1990s.

This is not just about high interest rates.

While rising rates have worsened borrowing capacity recently, the real issue is long-term: a chronic imbalance between supply and demand, caused by decades of under-building and rapid population growth, particularly through migration.

Australia’s housing construction has lagged behind population increases, especially in major cities. Dr Oliver stresses that this mismatch is a key reason prices have soared, and affordability has collapsed, over the long term.

While affordability is stretched, supply constraints will continue to support property values, especially in tightly held or growing regions.

This has implications for investor strategy, particularly around long-term capital growth and rental yield potential.

If you feel like buying a home is harder today than it was a decade ago, you’re right, and the data backs that up.

Australia’s housing affordability is now at levels that would be considered extreme in almost any advanced economy.

Prices have outpaced incomes, deposits take far longer to save, and home ownership, once the backbone of the Australian retirement system, is slipping further out of reach for younger generations.

Dr Shane Oliver, Head of Investment Strategy and Chief Economist at AMP, didn't hold back when he says housing affordability has “reached a new record low."

In his Oliver’s Insights piece, Dr Oliver breaks down why this affordability problem isn’t cyclical but structural, and why it won’t be fixed with one or two policy tweaks.

A problem that has become chronic

For years, Australians have treated housing affordability almost like a background noise, a frustrating but manageable issue tied to interest rates or short-term market swings.

But Dr Oliver points out the reality: while interest rates have certainly played a role, the affordability crisis today is something far deeper.

It’s chronic and it's now structural as it is rooted in a persistent mismatch between supply and demand that has built up over decades.

Dr Oliver explains a few key trends on how we got here:

-

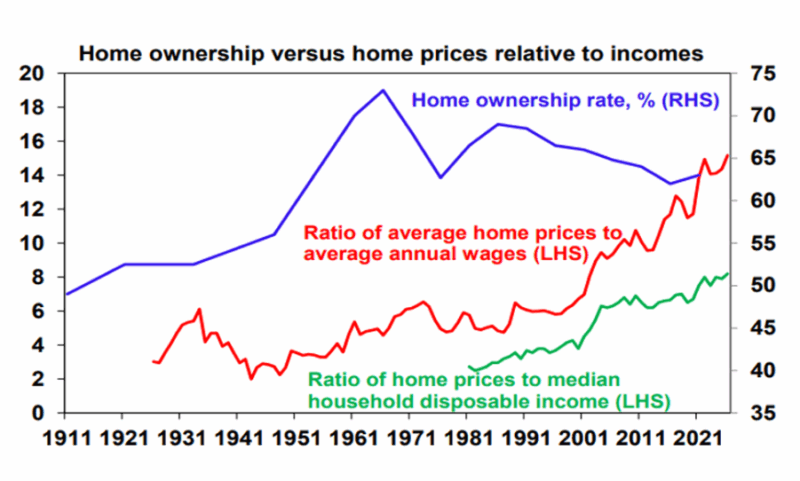

Home prices have skyrocketed relative to incomes and wages. Over the past 20 years, the ratio of home prices to income, one of the core measures of affordability, has more than doubled in Australia.

Source: AMP

-

Saving for a deposit takes far longer. The time required to save for a "traditional" 20% deposit has stretched to around 11 years, roughly double what it was 30 years ago.

Source: AMP

-

Home ownership is declining. With prices so high and alternatives like renting increasingly costly, fewer Australians are actually getting onto the property ladder.

In other words, this isn’t an overnight surprise; it’s the result of decades of supply constraints to match an ever-growing demand.

Why supply and demand got so out of whack

Dr Oliver’s analysis is helpful because it cuts through a lot of the noise.

Instead of focusing on isolated factors like foreign buyers or investor tax concessions, which often dominate media debates, he points to three broad drivers:

-

Interest rates and the affordability of debt.

Lower interest rates, especially since the early 2000s, greatly increased borrowing capacity. That helped buyers bid up prices, even though rates are now higher than the pandemic lows. -

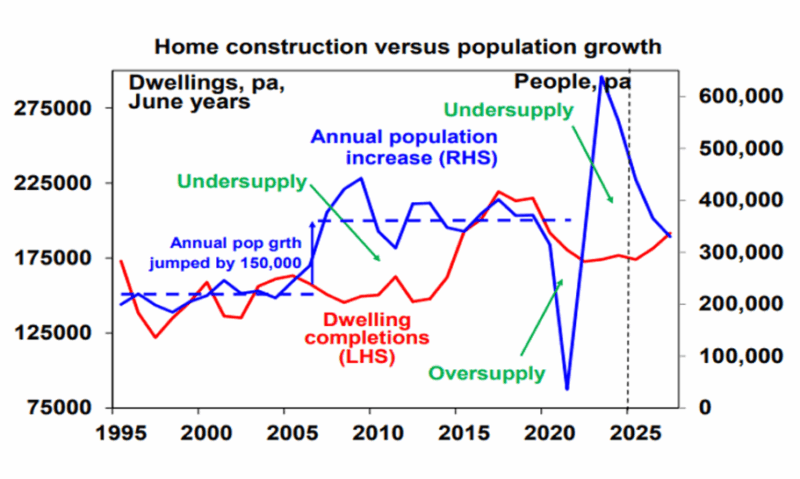

Housing supply just hasn’t kept pace.

For decades, dwelling construction has lagged behind underlying demand. Red tape, capacity constraints and production bottlenecks all contributed. As population growth surged, completions failed to keep up. -

Population is concentrated in a few cities.

Population growth has been highly concentrated in Sydney, Melbourne and Brisbane, putting additional pressure on a limited housing stock and pushing prices in these markets even higher.

Source: AMP

Dr Oliver points out that while these forces aren’t easy to reverse overnight, ignoring them has consequences.

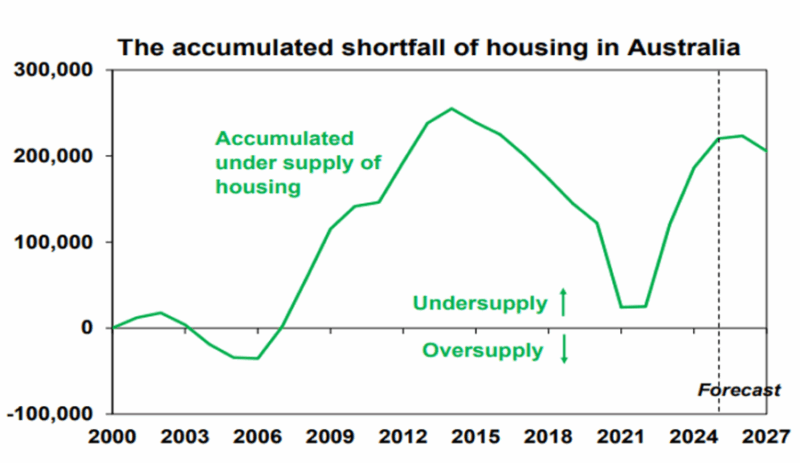

He explains that the accumulated shortfall of dwellings today is estimated in the hundreds of thousands, a structural gap that simple demand‑side solutions won’t close.

Source: AMP

Four practical paths forward

While Dr Oliver is clear that tere are no quick fixes to Australia’s affordability dilemma, he does lay out four broad policy directions that would make a meaningful difference if approached thoughtfully and over time:

1. Align immigration with housing supply

Rapid population growth, particularly from net migration, has been a major driver of housing demand without a corresponding increase in housing stock.

- Also read:Melbourne property market forecast for 2026 | Is it a good time to invest in Melbourne?

- Also read:Latest Property Price Forecasts Revealed. Australian Property Market Outlook 2026: Where To Now After The Rate Rise.

- Also read:Brisbane Property Market Forecast [2026] – What’s Ahead & Where to Invest

- Also read:Sydney property market forecast for 2026. Is it a good time to invest in Sydney?

- Also read:March Home Prices Still Rising | Latest stats from Dr. Andrew Wilson

Dr Oliver argues we need better alignment between immigration levels and the capacity to deliver new homes, otherwise shortages will persist.

This is a sensitive and politically charged conversation in Australia, but you can’t fix affordability without managing the scale and timing of demand relative to built supply.

2. Boost housing supply - everywhere

Yes, we need more supply, but it shouldn’t be limited to high‑density apartments near inner cities.

Dr Oliver emphasises the need for broader housing production across regions and metropolitan fringes.

This means:

-

Cutting red tape that slows development

-

Improving infrastructure planning to support new communities

-

Addressing skills and material shortages in construction

Without these kinds of reforms, Dr. Oliver says that supply will continue to lag demand, and affordability will get worse.

3. Encourage decentralisation

One of the lesser‑discussed but important points in Dr Oliver’s analysis is the role of geographic concentration.

Our big three cities are expensive because everyone wants to live there, and that doesn’t just raise prices, it also strains infrastructure, services, and liveability.

He suggests that supporting regional job growth, amenities and services could redistribute demand more evenly, which would ease affordability pressures in major cities.

4. Sensible tax and planning reform

Tax settings and planning systems play a huge role, according to Oliver.

Whether it’s land tax, negative gearing incentives, or stamp duties, the current regime often distorts investment decisions and housing distribution.

Dr Oliver doesn’t prescribe a specific tax overhaul, but he’s clear that targeted reform can improve allocative efficiency without destabilising market.

What this means for investors and policymakers

Here’s the practical takeaway:

Tip: The affordability issue isn’t going away any time soon.

It’s structural, deeply rooted in how we plan, build and grow our cities and regions.

Fixing it means sustained action across policy, planning and economics, not just headline‑grabbing announcements.

For investors, the imbalance between supply and demand suggests that housing values in undersupplied markets may remain supported over the long term … even as affordability challenges limit accessibility.

That, in turn, has implications for rental markets, capital growth expectations and portfolio strategy, particularly in markets outside the major capital cities.

For policymakers, Dr Oliver’s perspective should be a prompt to think beyond interest rates and incentives, and focus squarely on supply, distribution and demand alignment.

Bottom line

Housing affordability in Australia has reached historic lows.

Dr Shane Oliver’s analysis is a valuable reality check and a reminder that the problem is systemic, not temporary.

Solving it won’t be easy. It won’t come from a single policy announcement.

But thoughtful, sustained action on supply, migration balancing, decentralisation and tax reform could put Australia back on a path where the “Australian dream” doesn’t feel out of reach for an entire generation.