Key takeaways

The best buying opportunities appear when sentiment is negative, not when everyone feels confident. Melbourne today fits this classic countercyclical setup.

Melbourne has underperformed since 2021 due to migration losses, high interest rates, and anti-investor policies. This has created a rare value gap compared to other capital cities.

Melbourne is now significantly cheaper than Brisbane, Adelaide, and even Perth, despite stronger long-term fundamentals. This pricing disconnect presents a strategic entry point.

Key fundamentals are turning: migration is recovering, supply is tightening, and demand is rebuilding. These shifts typically precede price growth.

Smart investors focus on scarce, high-demand properties in inner and middle-ring suburbs. By the time the broader market turns bullish, the best opportunities will already be gone.

In early 2012, everyone had a reason not to buy in Sydney. We know how that ended.

The best property markets rarely feel like the best property markets when you're standing in them.

And I'll be honest - for the last few years, it's been hard to make a bullish case for Melbourne without immediately getting pushback. "The landlord taxes." "Investor exodus." "Brisbane overtook it." "Everyone's leaving."

Fair points, all of them.

But here's the thing about property markets - the best time to buy is almost never when everyone agrees it's a great time. It's when the story sounds bad, but the fundamentals are quietly turning.

And I believe that's exactly where Melbourne sits right now.

How did we get here?

Since late 2021, Melbourne has been the underdog of Australian capital cities.

What was historically the nation's second most expensive residential market experienced a notable shift in both price performance and population dynamics.

A significant driver was what happened post-COVID. Victoria recorded significant net interstate migration losses, with a large share of departing residents relocating to Queensland.

Add to that rising interest rates, a wave of new housing supply, and a Victorian government that, in my view, went way too hard on investors with land tax changes and other regulatory reforms and the result was that Melbourne fell behind in almost every metric.

One of the most striking pieces of evidence of this shift was that by March 2024, Brisbane overtook Melbourne in median dwelling prices - a reversal of a long-standing market hierarchy.

Think about that. Brisbane, which was trading at a 37% discount to Melbourne pre-pandemic, is now significantly above it.

And yet, or perhaps because of that, I think Melbourne has just become one of the most compelling property opportunities in the country.

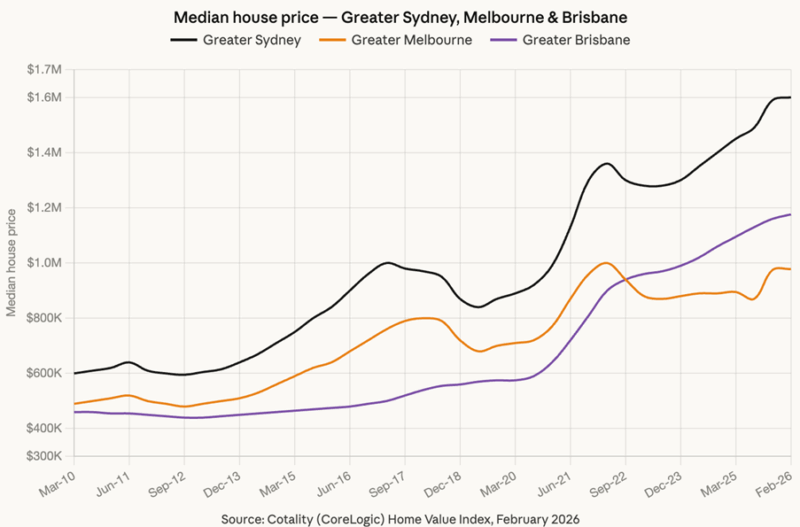

The value gap is extraordinary

The chart above tells you everything you need to know.

The latest Cotality figures show Melbourne's median house price sits at $978,000, below Perth, Adelaide, and Brisbane at $1,176,000 and Sydney at well over $1.6 million.

This is extraordinary. We're talking about Australia's second-largest city, a global financial and cultural hub, home to some of the world's best universities, healthcare, restaurants, and liveability, trading at a discount to Adelaide.

Dwelling values across Melbourne are up just 17.5% over the past five years, compared with the national average of 46.8%. Whilst that sounds like bad news, from an investor's perspective, it's the setup.

Why the story is changing

The reasons Melbourne underperformed are well-documented. But the reasons it will outperform from here are equally compelling, and starting to stack up.

- Interstate migration is stabilising. As Melbourne's relative affordability widened compared with both Sydney and Brisbane, the financial rationale for interstate relocation has weakened. Selling property in Melbourne at a relative discount only to purchase into increasingly expensive markets has become less economically attractive for many households. The exodus is slowing. And as Melbourne's economy recovers, younger professionals will be drawn back.

- International migration is surging. International migration has accelerated strongly, restoring a key pillar of housing demand for the Melbourne market. Population growth is once again contributing meaningfully to underlying demand for both rental and owner-occupied housing.

- New supply is drying up. Here's the thing that doesn't get talked about enough. Rising construction costs, financing constraints, and developer risk aversion have curtailed new project commencements across Victoria. Existing stock is expected to be progressively absorbed as population growth and confidence strengthens. Once that surplus is gone, the market will shift quickly. And FOMO has a way of arriving without warning.

- First-home buyers are back in the market thanks to various government incentives.

What the forecasters are saying

I'm not alone in this view.

Domain expects Melbourne's median house prices to increase this year and beyond. KPMG's Residential Property Outlook nominates Melbourne as the standout performer for 2026.

- Also read:Melbourne property market forecast for 2026 & 2027 | Separating the fundamentals from the sentiment

- Also read:Brisbane Property Market Forecast [2026 & Beyond] – What The Olympics Decade Means for Investors.

- Also read:Sydney property market forecast for 2026 and 2027 | Why the short-term softness is a long-term opportunity

- Also read:Latest Property Price Forecasts. Australian Property Market Outlook 2026-2027: Navigating a Market Correction

- Also read:Falling Home Prices Accelerate Over June | Latest stats from Dr. Andrew Wilson

Drivers include improved relative affordability, the return of positive interstate migration, strong auction clearance rates, and the value gap compared with Sydney and Brisbane.

From a strategic perspective, Melbourne's current position presents a potentially attractive entry point within the national housing cycle.

For both investors seeking value relative to other capital markets and owner-occupiers prioritising long-term fundamentals, Melbourne may increasingly represent one of the more compelling residential opportunities in Australia over the next phase of the cycle.

The countercyclical play

Here's what I keep coming back to.

The cities that have performed strongest - Brisbane, Perth, Adelaide - have done so in a compressed window.

Brisbane's median house value surged more than 14% during 2025, taking its median to approximately $1.17 million. Buyers who missed that run are now chasing properties in a market that's approaching its affordability ceiling.

Melbourne is the mirror image. Years of underperformance have created genuine value.

Supply is tightening. Population is growing. Confidence is returning. And the smart money - the countercyclical investors who buy when the headlines are still cautious - is starting to look very closely at inner and middle-ring Melbourne.

What I'd be focused on

Of course, not every property in Melbourne will benefit equally.

My view hasn't changed: avoid off-the-plan apartments and high-rise stock where oversupply remains a structural issue.

The opportunity is in well-located houses, townhouses and villa units in the inner and middle ring - the kinds of properties owner-occupiers compete hard for, in suburbs with genuine scarcity of supply and strong lifestyle appeal.

Think the areas that never really softened much in the first place, and are now seeing early signs of renewed competition - inner east, inner north, and pockets of the bayside.

These are the suburbs where the turning point will be felt first and most sharply.

As I see it, while the past several years have seen Melbourne underperform relative to its interstate counterparts, the underlying fundamentals are now realigning in a manner that suggests the market may be turning the corner.

And in my experience, by the time everyone agrees a market has turned, the best entry points are already behind you.

What you can do about this.

The window on Melbourne's underperformance won't stay open indefinitely.

Markets like this don't announce their turning point with a trumpet fanfare.

They quietly shift beneath the surface, and by the time the headlines catch up, the best opportunities are already gone.

If you'd like to talk through what this means for your specific situation, click here now and organise a Wealth Discovery Session with one of the Wealth Strategists at Metropole.

It's a no-obligation conversation where we look at where you are now, where you want to be, and whether Melbourne — or any other market — makes sense as your next move. You can lock in your time here.