I recently ran a LinkedIn poll asking a simple question:

What is actually driving Australia’s new housing stress?

LinkedIn only gives you four options. So I went with what I thought were the big ones:

• Lack of new housing supply

• Planning approvals and delays

• Interest rate settings

• Population growth

The result?

42% said planning approvals and delays.

34% blamed lack of supply.

21% population growth.

Just 3% pointed at interest rates.

So according to the industry cohort that follows me, planning is the biggest bottleneck.

That gave me an excuse to dust off a few of my helicopter charts. But before we accept that town planning is largely to blame, it is worth revisiting what actually happened over the past five years.

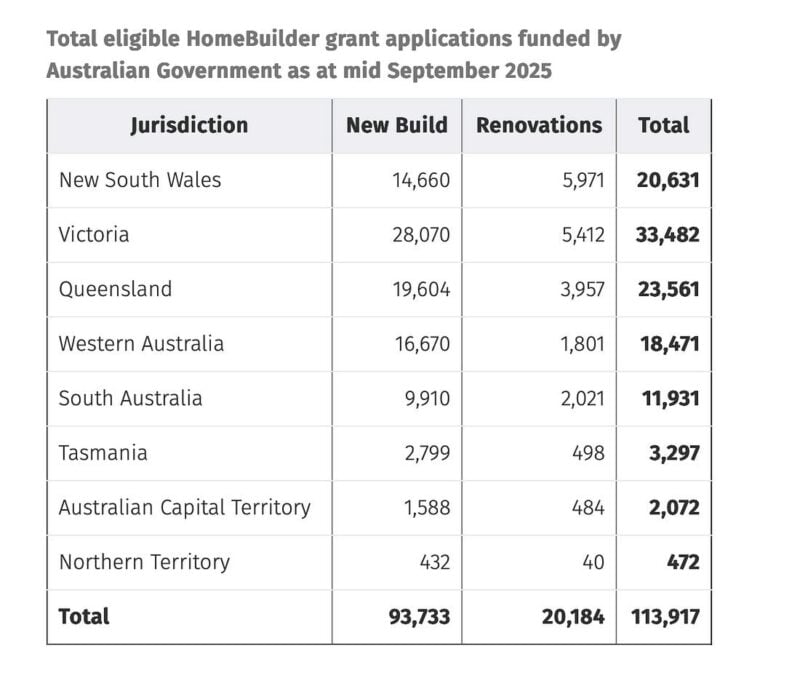

Start with HomeBuilder

Announced in June 2020, the program offered eligible owner occupiers a $25,000 grant, later reduced to $15,000, to build a new home or undertake substantial renovations.

It was extended several times through to March 2021 as governments attempted to sustain construction momentum during Covid.

In total, more than 113,000 applications were approved nationally.

Over 93,000 of those were for new builds and just over 20,000 for renovations.

Victoria led the pack followed by Queensland and then New South Wales. Around $2.64 billion was distributed.

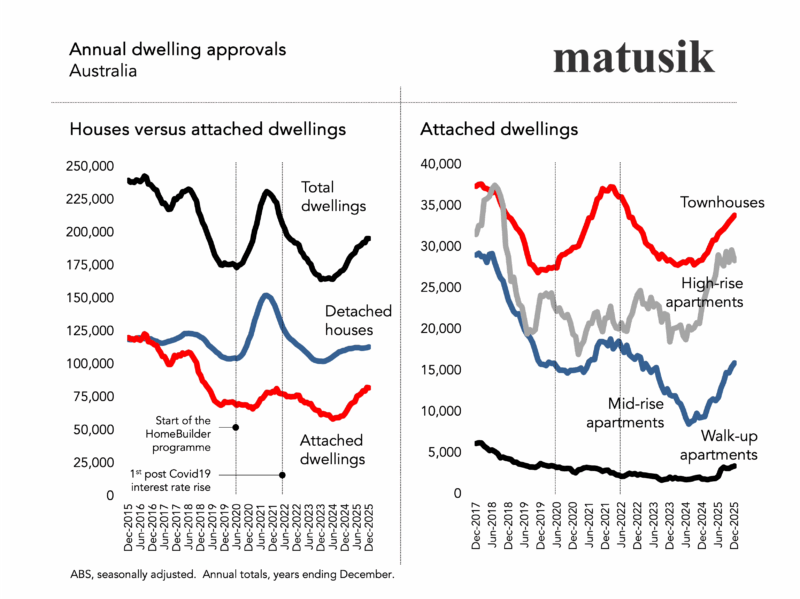

Dwelling approvals

And the impact is visible in the approvals data.

Detached housing approvals surged as HomeBuilder landed. Why? Because the scheme was perfectly structured for detached product.

Owner occupiers could sign a building contract quickly, the product is relatively simple to price and commence, and there is no presale hurdle. Once approved, a house typically proceeds.

Then interest rates rose.

As stimulus rolled off and rates lifted, detached approvals eased.

The shift was almost symmetrical. What fiscal policy giveth, monetary policy can taketh away.

Now look at the attached dwelling market.

Recent data shows attached approvals lifting again, particularly townhouses. High rise has stabilised. Mid rise is attempting a recovery. There is movement across the board.

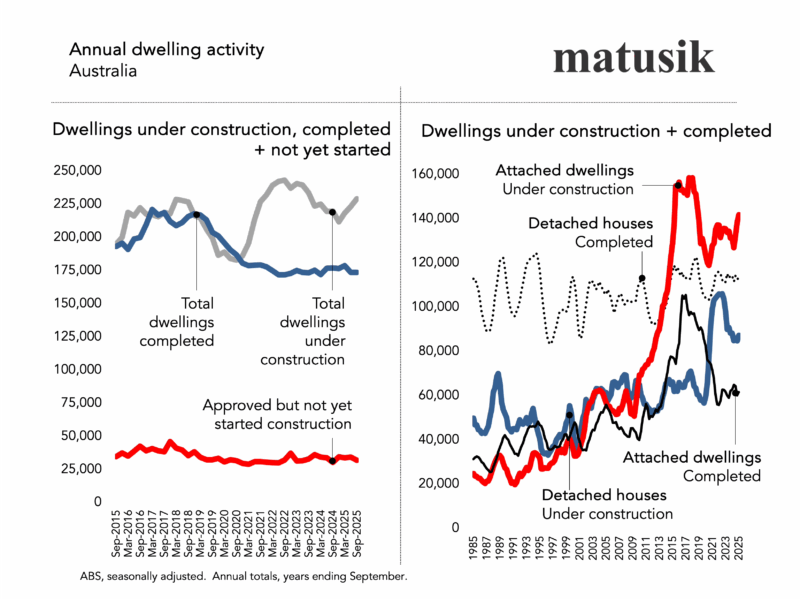

Approved but not yet started

But here is the crucial point.

- Also read:Melbourne property market forecast for 2026 & 2027 | Separating the fundamentals from the sentiment

- Also read:Latest Property Price Forecasts. Australian Property Market Outlook 2026-2027: Navigating a Market Correction

- Also read:Sydney property market forecast for 2026 and 2027 | Why the short-term softness is a long-term opportunity

- Also read:Brisbane Property Market Forecast [2026 & Beyond] – What The Olympics Decade Means for Investors.

- Also read:Falling Home Prices Accelerate Over June | Latest stats from Dr. Andrew Wilson

Overall the stock of approved but not yet commenced dwellings is not especially large. But my work shows that detached houses have a build conversion rate of roughly 95% nationally. If a house is approved, it almost always gets built.

Attached dwellings convert at closer to 60%, even less in some regional markets and smaller capitals.

So when town planners argue that approvals are not the issue because “we approve plenty”, the detached data largely supports them. Once green lit, houses move.

Apartments are a different story. Finance, pre-sales, construction cost volatility, builder risk and feasibility margins all intervene between approval and commencement. An approval does not guarantee delivery. Far from it.

Structural shift?

Yet the dwellings currently under construction nationally are now predominantly attached rather than detached. Is there a structural shift in the new housing supply pipeline?

This raises another important question. If planning approvals are a core problem, are they more acute for detached estates on the urban fringe, or for medium and higher density infill in established areas?

As noted above outer suburban detached supply tends to respond quickly when economics stack up. Infill density often faces longer assessment pathways, community objection, redesign and profit margin compression.

I reckon we are simultaneously constraining urban sprawl and infill medium density.

We should approve more detached digs and do more to get the approved attached product actually built.

Three things we could we actually do about it?

First, separate detached and attached dwelling policy responses. They behave differently and should not be treated as one market.

Detached housing largely needs serviced land, infrastructure sequencing and finance stability.

If a greenfield project is approved, it gets built.

So the focus there should be faster infrastructure delivery, predictable and sensible developer charges, and coordinated land release.

Attached housing is where the real friction sits.

The answer is not just more, or even, faster approvals, but better feasibility settings. That means realistic infrastructure levies, consistent height and density rules, and fewer information requests mid assessment.

If a project complies with the code, it should be approved within fixed timeframes. Certainty is more valuable than speed alone.

Second, reduce pre-sale risk.

Governments could underwrite a portion of pre-sales for build to sell projects that meet affordability criteria, similar to how HomeBuilder reduced risk for detached builders.

Alternatively, expand institutional build to rent settings to include a range of product types and funding options.

Third, address construction productivity. Standardised designs, modular pathways and pattern book approvals for townhouses and low rise apartments would reduce cost volatility and improve conversion rates.

Stripping back union heavy handed rules and behaviour would also have big positive impact.

Encourage major banks lend 80% on modular builds.

In short, I think we should stop arguing about whether we approve enough and start aligning planning, finance and feasibility so approvals - especially attached dwellings - actually turn into homes.