I get this question all the time. Most property investment commentators will tell you that a vacancy rate under 2–3% is a sign of a strong rental market.

That answer, however, is incomplete, and in some cases, dangerously misleading.

Relying on vacancy rates alone has cost many investors significant money, particularly in inner-city apartment markets where the underlying risks are not visible in headline data.

Why vacancy rates can be misleading

Vacancy rates are a useful starting point, but they do not tell you how many properties are competing for the same tenants, whether stock is diverse or largely identical and how concentrated investor ownership is in a location.

Without this context, a “low” vacancy rate can give a false sense of security.

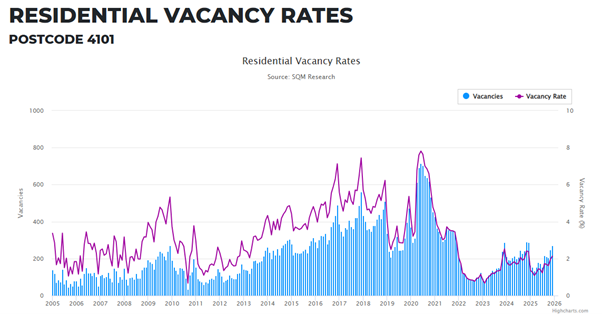

West End and South Brisbane: a vacancy rate that looks healthy on paper

Take West End and South Brisbane (postcode 4101) as an example - an inner-city area of Brisbane.

At face value, the vacancy rate looks encouraging. A vacancy rate of 1–2% typically suggests strong tenant demand and limited rental risk.

But when you scratch beneath the surface, a very different picture emerges.

This is not a short-term anomaly. It is the result of more than a decade of planning decisions, development activity and investor behaviour — and it is a pattern that still has years to play out.

How 4101 became an apartment-heavy market

Historically, West End and South Brisbane are two of Brisbane’s early inner-city areas south of the river.

They consisted largely of workers’ cottages, mixed with factories and commercial uses. By modern standards, these were relatively low-density and modest areas.

The transformation began in earnest following Expo ’88. Industrial uses declined, Brisbane’s inner-city lifestyle appeal grew, and West End evolved into a culturally diverse, vibrant urban village.

Between the early 1990s and mid-2000s, gentrification accelerated. Homes were renovated, amenity improved, and demand strengthened.

At the same time, Brisbane City Council adopted a broader strategy to increase inner-city density.

While strict controls protected heritage housing and streetscapes, large former industrial and commercial precincts, particularly in West End and South Brisbane, were opened up for medium and high-density development.

Developers responded quickly. To fund and de-risk these projects, many apartments were sold off-the-plan, predominantly to interstate investors.

When supply overwhelms demand

Between roughly 2010 and 2020, apartment construction significantly outpaced organic rental demand - you can see this in the table below, the spikes are completed buildings coming online, and happening too frequently to be absorbed into the rental market.

The consequences were predictable: - rising vacancy rates, aggressive rental incentives (discounted rent, giveaways, short-term inducements, falling rental yields and investors competing heavily on price to secure tenants

Some owners were forced to sell at a loss, compounding the financial impact.

COVID then amplified these pressures.

A large portion of the local tenant base consisted of students and casually employed renters who received limited support. Many returned to family homes, further weakening demand.

Why today’s market still isn’t “normal”

Post-COVID, Brisbane experienced strong population growth.

Work-from-home flexibility and lifestyle migration boosted demand, while construction slowed sharply due to material shortages and rising costs.

- Also read:Latest Property Price Forecasts. Australian Property Market Outlook 2026: Where To Now After The Rate Rise & Budget Changes.

- Also read:Melbourne property market forecast for 2026 & 2027 | Why the opportunity is bigger than it looks

- Also read:Sydney property market forecast for 2026 and 2027 | Why the short-term softness is a long-term opportunity

- Also read:Brisbane Property Market Forecast [2026 & Beyond] – What The Olympics Decade Means for Investors.

- Also read:Home Prices Now Falling Following Rate Rises | Latest stats from Dr. Andrew Wilson

As a result, the excess rental supply gradually diminished, and vacancy rates returned to what appears to be a “normal” range.

The key word here is “appears.’ This market is not normal - it is fragile.

What the underlying numbers really show

To understand why, we need to look beyond the vacancy rate and examine investor concentration.

Using SQM Research data for December 2025 for postcode 4101: -

- A vacancy rate: approximately 1%

- Properties advertised for rent during the month: 271

If 271 advertised properties represent 2.1% of the rental pool, this implies a total rental stock of approximately 12,900 investment properties in the postcode.

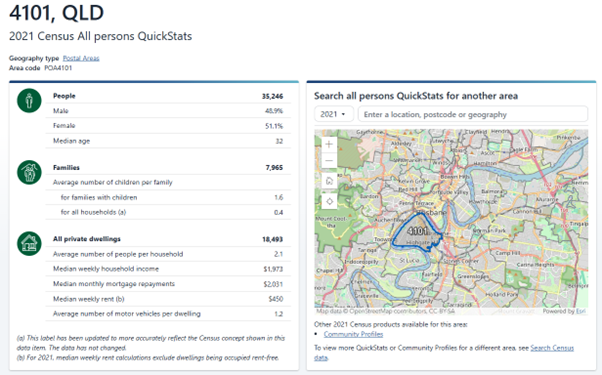

Government census data (2021) shows 18,493 total dwellings in postcode 4101. Even allowing for additional supply since then and rounding total dwellings to 19,000, this suggests that…

Roughly two out of every three dwellings in this postcode are investment properties.

In simple terms, this is an exceptionally high level of investor concentration.

Source – Australian Bureau of Statistics

Why investor concentration matters

Markets with a high proportion of investor-owned, near-identical apartments behave very differently from markets dominated by owner-occupiers or diverse housing stock.

When conditions change - interest rates, supply pipelines, employment patterns or migration flows - these markets can shift quickly.

Low vacancy rates do not eliminate risk; they simply mask it until competition re-emerges.

The forward risk investors need to understand

Thousands of additional apartment dwellings are still moving through Brisbane City Council’s planning and approval pipeline.

Construction activity is already increasing as post-COVID constraints ease.

As new stock enters the market, competition for tenants will rise again, particularly in locations where apartments are highly homogenous, owner-occupier demand is limited and rental performance relies on consistently tight market conditions.

Source https://brisbanedevelopment.com.au – Developments in various stages of planning through Brisbane City Council

The takeaway

Vacancy rates should never be assessed in isolation.

A low vacancy rate can exist in a market that carries significant structural risk, especially where investor concentration is high and future supply is substantial.

This is why experienced analysis looks beyond headline statistics and focuses on how a market is likely to behave across different phases of the cycle, not just how it looks today.

Understanding these nuances before you invest can make a material difference to long-term outcomes.