Key takeaways

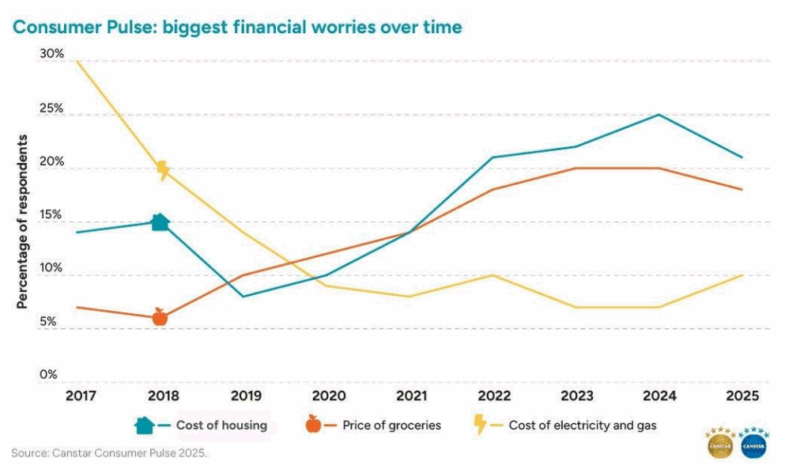

Despite three RBA rate cuts in 2025, the cost of housing, including both mortgages and rents, remains Australians’ #1 financial worry, and concern has doubled over five years.

Rate relief hasn’t undone years of higher repayments or rapidly rising rents.

Half of renters saw rents rise again in 2025, with an average increase of $62 per week.

Two-thirds of owner-occupiers feel prepared for rates to stay where they are, and 71% of investors are comfortable.

But 19% of potential sellers are considering selling because they cannot manage repayments, a sign that mortgage stress is still simmering beneath the surface.

Despite affordability issues, 56% expect house prices to rise steadily, and another 17% think they’ll surge.

Only 5% believe prices will fall. This reflects strong underlying demand and a public that recognises ongoing supply shortages.

A majority (55%) of property owners say nothing would entice them to buy another property right now, signalling a temporary pause in investor appetite.

But motivations like lower living costs, lower prices, or lower rates show investors are not bearish, they’re waiting for conditions to ease. This creates a period of opportunity for strategic buyers.

If you were hoping the three rate cuts in 2025 would finally give Australians some breathing room, you’re not alone.

Many households entered the year optimistic, believing the worst was behind them and that easing monetary policy would start to unwind several years of relentless financial pressure.

But the reality has been very different.

The latest Canstar Consumer Pulse Report, a survey of more than 2,000 Australians, reveals a confronting truth: despite falling inflation and softer interest rates, the cost of housing remains Australia’s number one financial worry heading into 2026.

And not by a small margin.

The level of concern tied to property, including mortgages and rents, has more than doubled over the past five years.

In a country where homeownership is part of our cultural DNA, this is more than just an economic issue; it’s a social one.

And the trends highlighted in this report show that the pressures Australians are facing are structural, not cyclical.

Housing costs aren’t just high, they’re reshaping behaviour

One of the most striking findings in the report is how consistently, and sharply, concern about housing has risen.

Canstar’s data insights director Sally Tindall offers one of the most succinct assessments of the situation:

“Despite three cash rate cuts this year, the cost of housing is still the nation’s biggest financial pressure.

The RBA relief has helped, but not nearly enough to unwind years of surging mortgage repayments and escalating rents.”

Across the nation, 21% of Australians say housing is their biggest financial concern, outpacing groceries, energy, and insurance.

In fact, housing has been the top-ranked worry for four consecutive years.

Even widespread cost-of-living pressures haven’t managed to knock it from the top spot.

Clearly Australians don’t believe affordability is improving.

Mortgage repayments remain significantly elevated

A typical borrower with a $600,000, 25-year loan taken out before the RBA’s rate-hiking cycle began in 2022 is still paying around 50% more per month, even after three rate cuts this year.

In other words, the cuts have slowed the bleeding but they haven’t reset the clock.

Borrowers who haven’t refinanced, and many still haven’t, are carrying the weight of years of rapid tightening interest rates.

Note: Canstar report that more than one-quarter (26%) of property owners surveyed are considering selling within the next two years.

While downsizing and upgrading are the main reasons for selling, a concerning 19% of people considering selling are doing so because they cannot afford higher loan repayments, up from 16% the year before.

This last group is the one we should watch closely.

It’s smaller than the pandemic-era mortgage cliff predictions, but still large enough to shape the market in pockets where overstretched borrowers hold similar types of properties.

Regionally, Queensland leads the country in potential sellers, followed by Victoria, Western Australia, NSW, and South Australia.

This geographic variation often reflects where borrowing increased most aggressively during the boom.

When it comes to buying, nearly two-fifths of Australians worry that the revised Home Guarantee Scheme (5% deposit for first home buyers) will either push up prices (27%) or increase market competition (12%), with only 15% viewing it as genuinely helpful for first-time buyers.

Renters are at their limits

While owners are adjusting, renters are reaching breaking point according to Canstar.

Half of all renters experienced a rent rise in 2025, with the average increase now sitting at $62 per week higher than last year.

Younger Australians, particularly Gen Z, have felt the sharpest increase, largely because many are entering the rental market for the first time.

The story behind those numbers is even more concerning:

-

42% of renters have cut back on essential spending just to afford a roof over their head

-

31% say they can only cope with very strict budgeting

-

17% have moved or are actively planning to move purely for affordability reasons

And perhaps the most significant long-term trend:

80% of renters who intend to buy a home say the cost of living is preventing them from saving a deposit.

This indicates a generational bottleneck; today’s higher rents are tomorrow’s lower homeownership rates.

What Australians really expect from house prices

Another key takeaway from the report is the public’s expectation of future price growth.

Despite affordability challenges, the majority of Australians do not believe property prices will fall.

According to the report:

-

56% expect steady price growth over the next two years

-

17% believe prices will “skyrocket”

-

Only 5% expect prices to fall

- Also read:Sydney property market forecast for 2026 and 2027 | Why the short-term softness is a long-term opportunity

- Also read:Latest Property Price Forecasts. Australian Property Market Outlook 2026: Where To Now After The Rate Rise & Budget Changes.

- Also read:Brisbane Property Market Forecast [2026 & Beyond] – What The Olympics Decade Means for Investors.

- Also read:Melbourne property market forecast for 2026 & 2027 | Why the opportunity is bigger than it looks

- Also read:Falling Home Prices Accelerate Over June | Latest stats from Dr. Andrew Wilson

- Also read:Sydney property market forecast for 2026 and 2027 | Why the short-term softness is a long-term opportunity

This sentiment aligns with what we’re seeing on the ground at Metropole: underlying demand remains strong, supply remains tight, and construction constraints are ongoing.

With rising rents, low vacancy rates, strong migration, and persistent undersupply, most Australians intuitively understand that property values are likely to continue trending upward.

This is a critical insight for investors.

Australians expect higher prices, even while feeling squeezed. That tells you how deeply entrenched the shortage of housing is.

Borrowers are adapting. Renters are not.

One of the more interesting psychological trends revealed in the report is that borrowers are becoming more resilient, while renters are becoming more stressed.

Two-thirds of owner-occupiers feel prepared for rates to hold at current levels into 2026, an increase from last year.

Investor sentiment is even stronger, with 71% feeling prepared.

This resilience isn’t surprising. Borrowers tend to have:

-

More stable incomes

-

Access to refinancing

-

Options to cut discretionary spending

-

The incentive to “hang in there”

Renters, on the other hand, face rising rents, limited housing supply, and almost no bargaining power.

This divide between renter hardship and borrower resilience is becoming one of Australia’s most significant socio-economic gaps.

Ms Tindall also highlights the contrasting resilience between borrowers and renters:

“Borrowers are gradually adjusting to current interest rate settings, but renters have far less room to move.

Almost half have had to cut back on essential spending just to keep a roof over their heads, and a growing share are relocating purely for affordability reasons.”

Australians don’t trust the 5% deposit scheme

A particularly revealing section of the report explores public attitudes toward the revised Home Guarantee Scheme.

Australians are wary:

-

27% believe it will push prices up

-

12% think it will increase competition for limited housing

-

21% fear it encourages risky borrowing

-

Only 15% think it genuinely helps first-home buyers

This scepticism underscores a broader issue: Australians clearly feel housing policy focuses too much on stimulating demand and not enough on addressing supply.

My take: what all this means for property investors in 2026

Here’s the strategic lens I’d offer:

1. The long-term fundamentals remain extremely strong

Strong population growth, chronic undersupply, rising rents, and lagging construction capacity will continue to support price growth.

2. Renters delaying homeownership extends rental demand

With 80% of aspiring buyers unable to save due to living costs, rental demand will remain elevated, benefitting well-positioned landlords.

3. The investment market is temporarily paused, not broken

While 55% of those surveyed say they’re unlikely to invest soon, this reflects economic pressure rather than a belief that property is unattractive.

5. The next upswing will reward those who prepare early

When confidence returns, and it will, the current lull in investor activity will reverse quickly.

Final Thoughts

The Canstar Consumer Pulse Report doesn’t just highlight the financial strain Australians are under. It highlights the resilience of the property market, the depth of demand, and the disconnect between affordability pressures and long-term expectations.

In other words, the challenges are real, but so are the opportunities.

Housing remains the nation’s biggest financial worry, but it also remains the foundation of long-term wealth for Australians who take a strategic, informed approach.

Smart investors will use 2026 not to retreat, but to position themselves for the next stage of growth.