Key takeaways

New research shows the average Australian spends six years renting before buying their first home, with South Australians waiting up to seven years, and NSW and Queensland renters close behind at 6.5 years.

With the median house price now $935,000 and the median unit $700,000, even someone earning the median wage and saving 10% of their income needs four to five years just to build a 5% deposit, assuming no financial setbacks.

The data reveals that while around half of first home buyers rent for 1–6 years, a concerning 12% rent for over 10 years before buying — highlighting the growing divide between renters and homeowners.

A major shift is underway: some lenders now accept consistent rent payments as evidence of “genuine savings,” allowing disciplined renters to qualify for loans sooner, provided they can prove at least six months of on-time rent payments.

Despite soaring prices, smaller deposits, government schemes, and support from the Bank of Mum and Dad are helping more young Australians break into the market and many are skipping renting altogether by staying with parents until they buy.

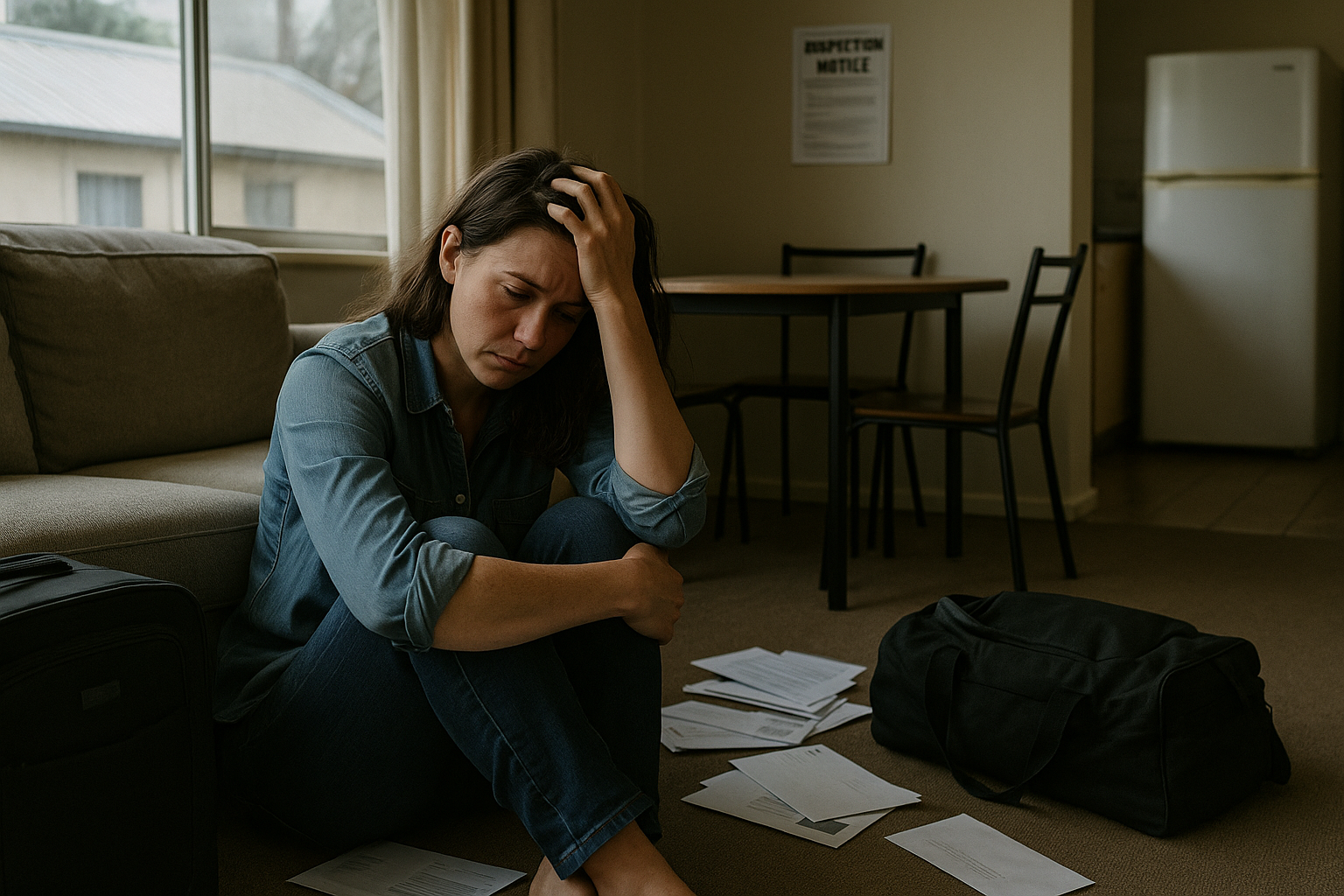

For decades, owning a home has been the great Australian dream, a symbol of stability, security, and success.

But for many would-be homeowners today, that dream feels like it’s slipping further away with every rent payment.

And now, fresh research from Money.com.au has laid bare just how tough things have become.

The average Aussie is stuck renting for six long years before they can scrape together enough for a deposit on their first home.

Yes - 6 years of paying off someone else’s mortgage before you can even start your own.

But the story doesn’t end there, the pain isn’t evenly spread across the country.

The state of play: where renters wait the longest

If you’re in South Australia, you’ll need the most patience; renters there spend an average of seven years before making the leap into homeownership.

In New South Wales and Queensland, the average renter is stuck for about 6.5 years, while Victorians and Western Australians are slightly better off, taking around six years to buy.

And all this is happening while home prices continue to hit new highs.

In September, the national median house value hit $935,000, while the typical unit is nudging $700,000.

Now, let’s put that into perspective.

Someone earning the median full-time wage of about $90,000 and saving 10% of their income each year would still need just over five years to save a 5% deposit on a median-priced house, and around four years for a unit.

That’s assuming nothing goes wrong along the way, no surprise rent hikes, no cost-of-living blowouts, no broken car or medical bill derailing the plan.

The survey also found that:

-

26% of first home buyers rented for 1–3 years,

-

21% rented for 4–6 years,

-

9% rented for 7–10 years, and

-

12% were renting for over a decade before finally buying.

Only a lucky 9% managed to escape the rental cycle within a year.

Interestingly, almost a quarter (22%) of respondents skipped renting altogether, choosing to live with their parents until they could afford to buy.

While this might have been frowned upon a generation ago, it’s increasingly becoming a smart wealth strategy today, especially when you consider the savings boost it offers.

A glimmer of hope: when rent counts as savings

But here’s the silver lining that many aspiring buyers might not know about.

According to Money.com.au’s mortgage expert Debbie Hays, your rental history could now count as part of your “genuine savings”, potentially helping you get a foot on the ladder sooner.

She explains:

“By counting regular rent payments as genuine savings, lenders are giving reliable tenants a bridge into homeownership. In their eyes, a reliable tenant is likely to be a reliable borrower too.”

- Also read:Rents Keep Rising While Auction Markets Cool – What It Means for Property Investors | Property Insiders

- Also read:National Property Listings Ease in June While Annual Supply Continues to Strengthen | Latest SQM Listing Data

- Also read:Latest Property Price Forecasts. Australian Property Market Outlook 2026-2027: Navigating a Market Correction

- Also read:National Weekly Auction Report – July 4th 2026 | Auction Markets Remain Subdued as School Holidays Commence

- Also read:Falling Home Prices Accelerate Over June | Latest stats from Dr. Andrew Wilson

This policy shift from some lenders is a game-changer.

It recognises that many renters are demonstrating financial discipline, just not in the traditional way.

After all, making rent payments on time, month after month, shows consistency and reliability, even if you’re not stacking cash in a savings account.

How renters can use this to their advantage

So, how can renters actually leverage this?

Typically, to qualify for a mortgage, you’ll need:

-

A 5% deposit (held in a bank account for at least three months), and

-

Proof of genuine savings.

However, if you’ve been renting for six months or more, and can show a consistent track record of on-time payments, some lenders will consider that as part of your genuine savings.

To qualify, you’ll usually need:

-

A copy of your lease agreement,

-

A rental ledger or reference letter from your property manager confirming your payment history.

It’s not a universal policy, different banks have different rules, but for disciplined renters struggling to save while paying high rents, it’s an opportunity worth exploring.

Why the next generation might still have an edge

Despite the headlines, today’s first home buyers do have a few advantages their parents never did.

-

Smaller deposit requirements: Most lenders now accept a 5% deposit, compared to the traditional 20% of decades past.

-

Government support: Schemes like the First Home Guarantee and Home Buyer Fund are helping buyers get in sooner with smaller deposits.

-

Flexible lending criteria: Many lenders are assessing applications more holistically — not just by looking at savings, but also rent history and spending habits.

-

Parental support: The “Bank of Mum and Dad” remains one of the largest lenders in Australia, whether it’s via a gift, a family guarantee, or shared ownership structures.

The Bottom Line

Australia’s rental trap is real, and for many, it’s lasting longer than ever.

But it’s not hopeless. If you’re renting and dreaming of owning your first home, don’t underestimate the value of your rent history.

With the right strategy, the right lender, and the right guidance, your years of consistent rent payments could actually help you buy sooner.

At the end of the day, the key is to turn your financial reliability as a tenant into a powerful argument for your financial reliability as a homeowner.

Because while the journey to homeownership may be longer and tougher than it once was, those who play smart, not just hard, will still find their way through Australia’s brutal rental maze and into a home of their own.