Australians have long prided themselves on enjoying the good life—sun-soaked holidays, sparkling new cars in the driveway, freshly renovated homes, and indulgent weekends out.

But underneath this polished surface, a troubling financial reality is emerging.

A recent report from Finder paints a worrying picture: over 6.3 million Australians are falling into debt just to keep up appearances.

The social pressure to keep up with the Joneses is leading to a financial trap that threatens the long-term wealth and security of many Aussie households.

The cost of social pressure

We all know the feeling—seeing the neighbours drive a new car or friends flaunt their latest overseas vacation on Instagram.

The temptation to match those around us can feel overwhelming.

But as Sarah Megginson, Senior Editor at Finder, explains, this pressure is driving people to make poor financial decisions.

She further said:

“Australians are increasingly using debt to maintain a lifestyle that they can’t really afford.

It’s a worrying trend, and many don’t realise the long-term impact this could have on their financial wellbeing.”

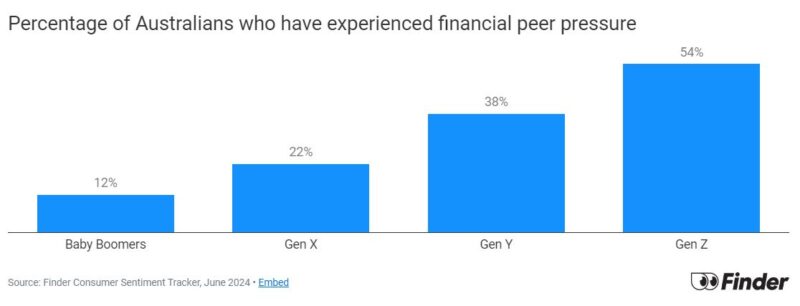

According to the Finder report, nearly 40% of Australian adults admit they have gone into debt to fund their lifestyle, with younger Australians—Millennials and Gen Z—being particularly vulnerable.

A staggering 64% of these younger generations confess to using credit to keep pace with their peers.

The need to fit in socially is pushing people to stretch beyond their financial means, often leading them down a dangerous path of debt accumulation.

The debt cycle: when debt becomes a trap

This isn’t just about one-off indulgences. It’s a systemic issue where debt becomes a crutch to fund everyday expenses and luxuries alike.

Whether it’s using credit cards, buy-now-pay-later schemes, or personal loans, the reliance on debt to keep up with lifestyle inflation is a growing concern.

Megginson highlights the dangers:

“Using debt to cover expenses may seem harmless at first, but it can quickly spiral out of control.

The compounding interest on debt can turn what started as a small splurge into a much bigger financial burden.”

Australians are already among the most indebted households in the world, and this lifestyle-driven debt only exacerbates the problem.

- Also read:6 Lessons from Robert Kiyosaki’s Rich Dad Poor Dad to Build Wealth and Financial Independence

- Also read:Retirement might not be as enjoyable as you expect

- Also read:3 Lessons I learned at Wealth Retreat

- Also read:How does my super get taxed?

- Also read:Why Testamentary Trusts Aren’t Just for the Rich: A Guide to Safeguarding Your Legacy Introduction

The average household debt in Australia sits at over 180% of disposable income, meaning that many Australians owe nearly twice as much as they earn.

When you add non-essential debt to that, the pressure becomes unsustainable.

The psychology behind debt: why are we doing this?

So why are so many Australians falling into this trap?

The answer lies in the psychology of social comparison.

In today’s hyper-connected world, it’s easier than ever to see how others live, thanks to social media platforms that amplify the best bits of people’s lives.

What we often forget is that social media only tells half the story.

As Megginson notes:

“Social media can create an illusion of success, where people only show their best moments—new cars, fancy holidays, and home renovations.

What you don’t see are the credit card bills piling up or the sleepless nights spent worrying about how to make the next payment.”

The fear of missing out (FOMO) plays a huge role in this behaviour.

We compare ourselves to our peers, and if we feel like we’re falling behind, the natural response is to try to catch up—often at the expense of our own financial health.

How to Break Free From the Debt Cycle

The good news is that this cycle can be broken. Here are some key strategies to protect your financial future and resist the pressure to keep up with the Joneses:

- Live within (or below) your means: One of the most powerful wealth-building habits is living within your means. This doesn’t mean depriving yourself of all luxuries, but rather making sure you’re spending mindfully. Prioritise saving and investing over consumer spending.

- Focus on long-term wealth creation: Every time you feel the pull to make a purchase because of social pressure, ask yourself: does this help me reach my long-term financial goals? Whether it’s building a property portfolio, funding your retirement, or creating an emergency buffer, keeping your eyes on the bigger picture will help curb impulsive spending.

- Avoid debt for discretionary spending: If you need to take on debt to afford something, reconsider whether you truly need it. Debt should be reserved for investments in your future, such as property or education, rather than items that will depreciate in value.

- Educate yourself on financial independence: Knowledge is the best defence against financial pitfalls. Take the time to understand the principles of wealth creation—whether it’s through property, shares, or other investments. The more you know, the less likely you’ll fall prey to the consumerism trap.

Final Thoughts

Australia’s debt crisis is about more than just numbers.

It’s a reflection of the pressure we put on ourselves to keep up with others—often at the expense of our own financial well-being.

As Sarah Megginson wisely points out:

“Real wealth comes from making smart financial decisions, not from trying to match someone else’s lifestyle.”

Breaking free from the debt cycle isn’t easy, but it’s essential if you want to build lasting wealth.

The key is to shift your mindset from short-term gratification to long-term financial security.

It’s time to stop worrying about keeping up with the Joneses and start focusing on building the financial future you truly deserve.