The latest housing market scare campaign focuses on questionable analysis of household debt levels.

Sharp declines in mortgage rates since 2011 have predictably activated housing markets with prices rising.

Higher prices reflect higher mortgages with borrowers taking on more debt as prices rise and enabled by lower mortgage rates allowing purchasers to borrow more with a given income

.

Although debt has risen with houses prices, the proportion of household income required to service higher debt has fallen over recent years despite low incomes growth and low real wages.

Despite this, current scaremongering speculates on the impact of higher interest rates on households paying a higher proportion of mortgage repayments from incomes.

- Also read:Latest Asking Prices State by State | Winter Lull takes Affect with Huge falls in Home Listings

- Also read:What does median home price really mean?

- Also read:Brisbane’s property market forecast for 2024

- Also read:Melbourne property market forecast for 2024

- Also read:Sydney property market forecast for 2024

Notwithstanding the remote chance of Big Banks lifting rates significantly in the near-term, the impact of higher rates would be marginal relative to the number of households affected.

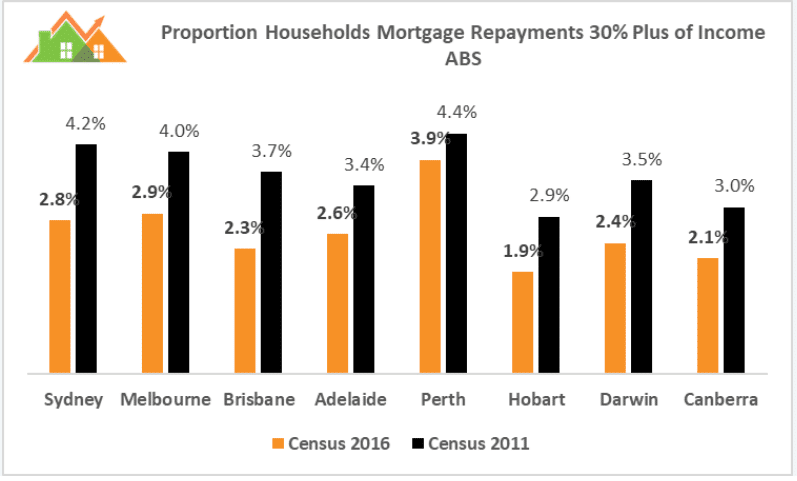

Census data reveals the proportion of households paying more than 30% of income in mortgage repayments fell below 3% in most capitals and in all capitals is well down on the previous Census.

And since the last Census, wages are up 4.1% and mortgage rates are down 0.5% with house price growth dissipating.

Enough said.