If you are contemplating investing in property, should you buy now or wait?

What if prices fall?

Maybe you would be better off waiting?

As my analysis below reveals, buying for less than market value or at the bottom of the market (i.e. buying well), has very little impact.

The price we pay for a property has little impact on our success as investors.

So, the desire to buy below market is probably driven more by ego than fundamentals.

Timing the market is a flawed strategy

No one in the world has developed a reliable system for predicting how asset classes will change in the short term.

As Mr Buffett says; “forecasters will fill your ears but never your pockets.”Therefore, if you think you can implement a strategy that involves picking the bottom of the market, think again!

Not only is it impossible to do, but many of the indicators used to measure the health of the property market are lag indicators.

That is, by the time the indicators change, prices would have already rebounded somewhat.

How important is it to buy well?

This is a good question and one that I have spent a lot of time analysing.

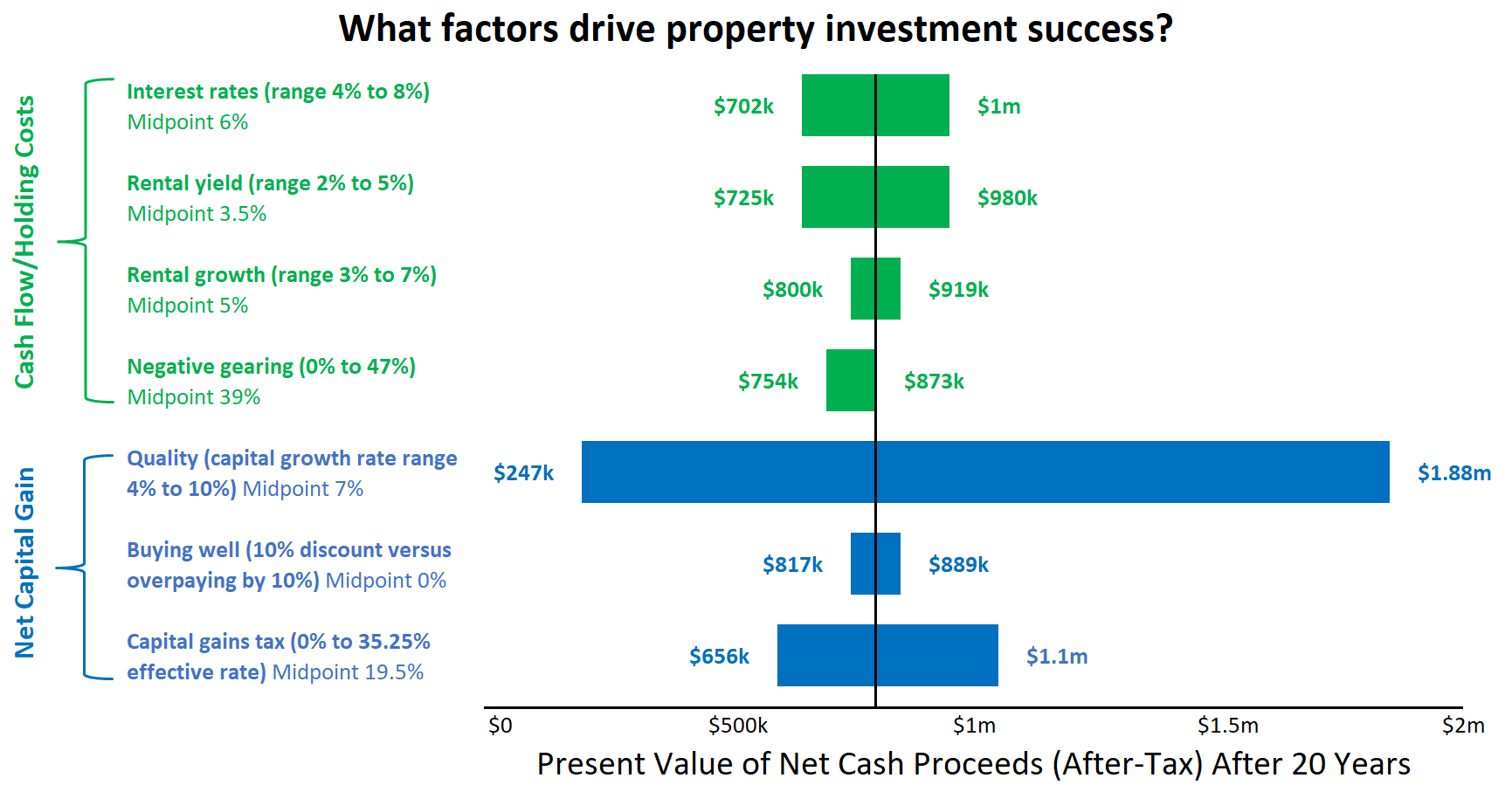

I financially modelled a $750,000 property investment and measured the sensitivity to the following factors/assumptions:

-

Capital growth – this is the average rate of appreciation in value over the next 20 years.

My base case assumption is a nominal rate of 7% p.a. (assuming an inflation rate of 2.5% p.a.).

The range I used was 4% (being only 1.5% above inflation) and 10% (which I have observed in blue-chip locations over the past 30 years). - Buying above or under fair market value – I measured the impact of buying 10% below market value versus over-paying by 10%.

- Capital gains tax (CGT) – I measured the impact of paying no CGT (e.g. owning in an SMSF) versus paying the maximum CGT (e.g. the ALP’s policy is to halve the CGT discount).

The midpoint I assumed is based on current laws at a tax rate of 39% p.a. - Interest rates – my midpoint is 6% but I sensitised using a range of 4% to 8% p.a.

- Rental yield – this is the amount of gross rental income you will receive compared to the property's value (expressed as a percentage). I have assumed a normalised mid-point of 3% but then also tested a range of 2% to 5%.

- Rental growth rate – this is how much the rent will increase by on average each year.

I have used a growth rate range of 3% – being slightly above CPI and 7% – which is relatively high. - Negative gearing – as has been well publicised, the ALP will ban negative gearing on existing properties (if you own existing investments, these are excluded, so you won’t be impacted).

As such, I sensitised the impact of negative gearing on an investment.

I compared no negative gearing versus maximal benefit at a tax rate of 47%. The midpoint was 39%.

What I did is held all factors the same (i.e. at the midpoint/base case) and changed one variable from high to low to measure the impact on after-tax cash (assuming you hold the investment property for 20 years and then sell it).

This included the cash flow cost plus the after-tax sale proceeds.

And the winner is…

As the chart below illustrates, buying under fair market value has very little impact on the success of your investment.

A property’s capital growth rate is by far the most important factor.

- Also read:Melbourne property market forecast for 2026 | Is it a good time to invest in Melbourne?

- Also read:Latest Property Price Forecasts Revealed. Australian Property Market Outlook 2026: Where To Now After The Rate Rise.

- Also read:Brisbane Property Market Forecast [2026] – What’s Ahead & Where to Invest

- Also read:Sydney property market forecast for 2026. Is it a good time to invest in Sydney?

- Also read:March Home Prices Still Rising | Latest stats from Dr. Andrew Wilson

A distant second is capital gains tax, then the interest rate and finally rental income.

What steps should you take as a result of this?

What steps should you take as a result of this?

If you are investing in property, forget about the timing, just focus on the quality of the asset.

To do that, I always recommend engaging the services of a reputable buyer’s agent.

Never, ever compromise on quality.

Secondly, think about capital gains tax – especially if you plan to (or already) own multiple investments.

People who own multiple investment properties might need to sell one in the future to assist with debt reduction and/or increase liquidity.

Take this into account before you invest and seek advice from a financial advisor and tax agent.

Thirdly, actively manage your property portfolio.

Keep on top of your property manager to ensure they are reviewing your rental income and recommending if you can make any minor or cosmetic improvements to maximise your income.

Also, make sure your mortgage broker is reviewing your loan structure and lenders – as this can have a big impact on your interest rate.

Number one: put your ego and fear aside

Maybe the most valuable takeaway from this analysis is to let go of the desire to try and time the market.

This desire is usually driven by fear or ego and frankly, neither are very useful emotions when making important investment decisions.

Instead, stick to the fundamentals.

The above analysis is simple math.

There’s no smoke or mirrors or subjectivity.

It clearly demonstrates that timing has had little impact on your success.