Key takeaways

Australia's top marginal tax rate of 47% is one of the highest in the developed world, yet it was designed in 1915 as a temporary wartime measure targeting only the ultra-wealthy.

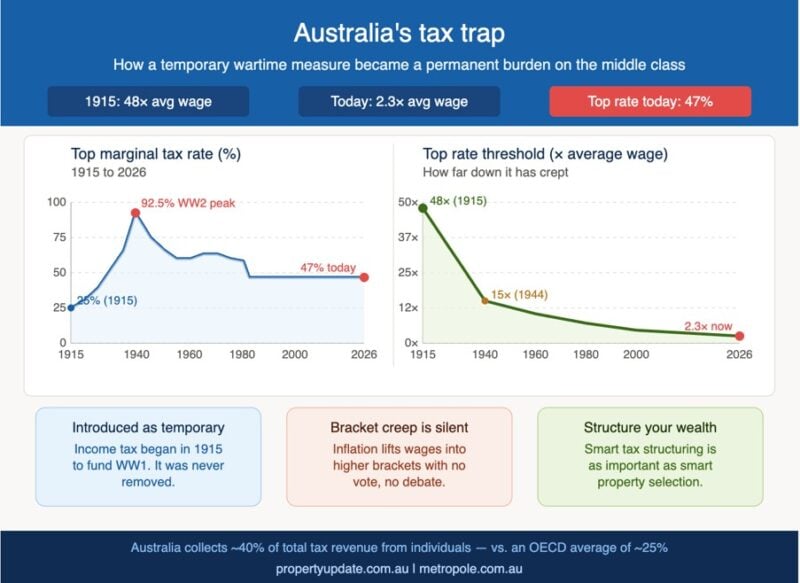

When income tax was first introduced, the top rate only applied to those earning the equivalent of $960,000 in today's dollars, roughly 48 times the average wage. Today that same top rate kicks in at just 2.3 times the average wage, catching teachers, nurses, tradies, and property investors.

Bracket creep is the silent mechanism behind this shift, where inflation pushes your wages into higher tax brackets even though your real purchasing power hasn't improved at all.

Australia is one of only four OECD countries that does not automatically index tax brackets to inflation, meaning the tax grab compounds every single year without any public debate or vote.

Australia collects around 40% of its total tax revenue from personal income taxes, compared to an OECD average of around 25%, making ordinary earners carry a disproportionately heavy load compared to most comparable countries.

Both Labor and Coalition governments have exploited bracket creep for decades, allowing it to silently accumulate and then handing back a portion as pre-election "tax cuts" to generate good publicity.

For property investors, the combination of high marginal rates, bracket creep, and the 2026 Federal Budget's changes to negative gearing, CGT, and trust distributions makes intelligent tax structuring more important than ever.

The solution is straightforward but politically inconvenient: index the tax brackets to inflation. Don't expect it to happen anytime soon.

Most Australians know they pay a lot of tax.

What most don't realise is just how dramatically the system has shifted over the past century, and how that shift is quietly eating away at the wealth of ordinary working Australians, especially investors.

Here's something worth thinking about as you head into tax time…Australia's top marginal tax rate of 47% is one of the highest in the world.

Yet the story behind that number is far more troubling than the rate itself.

Federal income tax in this country didn't start out as a fixture of Australian life. It was introduced in 1915-16 as a temporary measure to fund World War One spending.

It may have been temporary, yet we've been paying it ever since.

A tax that was never meant to reach you

When income tax was first introduced, the government wasn't coming for ordinary wage earners or even successful professionals.

The income threshold for the top marginal rate of 25% in 1915-16 was equivalent to about $960,000 in today's dollars, which was roughly 48 times the average wage, so it only affected the genuinely super-wealthy.

The tax was designed to hit people earning the equivalent of nearly $1 million today, not someone earning $200,000.

Wartime brought even more dramatic rates. Australia's top marginal rate hit 92.5% during 1943 to 1945 under the Curtin and Chifley governments.

For context, the top rate in the US at the time was 99% on incomes above US$400,000, and 99.25% in the UK.

Even at those extraordinary levels, the rates were aimed at very high earners, not the broader workforce, but something changed over the decades that followed.

How the tax crept down to the middle class

Today, Australia's top tax rate of 47% cuts in at just 2.3 times the average wage, meaning it now hits the broad middle class.

Think about what that means in practical terms. A nurse, a teacher, a tradie running their own business, a property investor with a few properties; these are the people now subject to a tax rate that was originally designed to capture only the elite tier of earners.

This shift happened through two mechanisms working together.

The first was deliberate policy, as governments progressively lowered the income thresholds at which higher rates applied, catching more and more ordinary taxpayers.

The second, and in some ways the more insidious of the two, is what economists call bracket creep.

The silent tax grab nobody voted for

Bracket creep is disarmingly simple. As your wages rise with inflation, you move into higher tax brackets even though your real purchasing power hasn't improved at all.

You're earning more dollars that are worth less, but you're paying a higher rate of tax on them.

The OECD has specifically identified bracket creep as a factor that raised effective tax rates for Australian households and contributed to depressing real household incomes.

Now that’s the assessment of the world's leading economic research body.

Among the OECD member countries studied, just four, including Australia, do not automatically adjust their tax brackets in line with the inflation rate to neutralise the impact of wages growth.

So while most developed countries protect their citizens from this silent squeeze, Australia lets it run.

- Also read:6 Lessons from Robert Kiyosaki’s Rich Dad Poor Dad to Build Wealth and Financial Independence

- Also read:Retirement might not be as enjoyable as you expect

- Also read:3 Lessons I learned at Wealth Retreat

- Also read:How does my super get taxed?

- Also read:Why Testamentary Trusts Aren’t Just for the Rich: A Guide to Safeguarding Your Legacy Introduction

And governments of both persuasions have used it to their advantage.

Both Labor and Coalition governments routinely exploit bracket creep by handing out "tax cuts" before elections, but all they're doing is partially correcting the effects of bracket creep they've allowed to accumulate in the first place.

They take your money quietly, then give some of it back noisily just before polling day. It's a remarkably effective political trick.

The solution is straightforward: simply index the income thresholds for each tax bracket to inflation.

But governments hate that idea because it removes the ability to hand out those pre-election tax cut announcements, and it forces them to rein in government spending instead.

The bigger picture for investors

Australia funds a larger share of public spending through personal income tax than most comparable countries.

OECD data shows Australia collects about 40% of its total tax revenue from individuals, compared to an OECD average closer to 25%.

That's a remarkable imbalance, and it falls hardest on exactly the people who are working hard, earning well, and trying to build something.

The Parliamentary Budget Office has confirmed that Australia is more reliant on revenue from personal taxes compared to other OECD economies.

Our 10% GST is comparatively low, which means the personal income tax system has to do more of the heavy lifting to fund government services. The burden falls on earners, not consumers.

Of course, for anyone building a property portfolio, this matters enormously.

When you're working in a profession earning a decent income, drawing rent from investment properties, and potentially earning capital gains, the tax system is working against your wealth-building at every turn.

Bracket creep alone has been estimated to cost a typical high-income investor hundreds of thousands of dollars in compounded wealth over a working life.

And this is before we even factor in the 2026 Federal Budget's changes to negative gearing, capital gains tax, and discretionary trust distributions, which layer yet more complexity and cost onto serious investors.

What this means for your wealth strategy

This is one of the reasons I've always believed that smart tax structuring is as important as smart property selection.

If you're building a multi-property portfolio and your strategy hasn't evolved to account for the reality of Australia's tax environment, you're leaving a significant amount of wealth on the table.

The difference between good tax planning and no tax planning can easily run into hundreds of thousands of dollars across a portfolio over time.

Some of the most effective strategies involve thinking carefully about how properties and other investments are owned, whether that's in your own name, through a trust structure, or through superannuation, particularly given the current rule changes.

None of this is about avoidance or cutting corners. It's about understanding the system you're operating in and making intelligent decisions within it.

The tax system has shifted dramatically over 110 years from targeting the genuinely wealthy to catching almost anyone who earns a reasonable income. That shift happened largely without public debate, without votes, and without most people noticing.

But for serious investors, noticing is exactly where it starts.

If you'd like to talk through how your current portfolio and income structure sits in today's tax environment, our team at Metropole can help. The rules have changed significantly, but with the right strategy, the fundamentals of long-term wealth building remain as sound as they've always been.

Click here now and lock in a time to have a chat with one of the world's strategists at Mitra.