Key takeaways

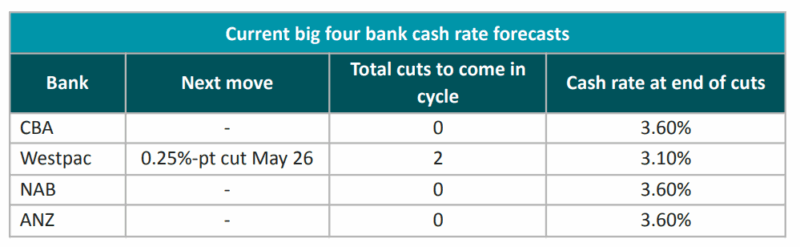

ANZ has revised its forecast and ruled out further cash rate cuts, aligning with CBA and NAB that the cash rate is likely to stay on hold through 2026.

Westpac still expects two cuts in 2026, but it’s now swimming against the tide of the other three majors.

With inflation “moving in the wrong direction” and unemployment back around 4.3%, the case for near-term cuts is weak and some economists are even flagging that the next move could be up.

Canstar’s Consumer Pulse shows 66% of borrowers say they’re prepared for rates to stay put in 2026, but 34% are either not prepared or unsure.

Competitive mortgage rates are still available for borrowers willing to refinance or negotiate, while term deposit rate increases (34 banks lifting at least one TD rate in November) suggest markets think further cash rate cuts are unlikely.

For a while there, “the next rate cut” started to feel like a foregone conclusion.

Borrowers were counting on it, buyers were pricing it in, and the media narrative was drifting toward relief.

But now the story is different, with most economists suggesting there won't be another interest rate cut anytime soon.

In a fresh update to its cash-rate outlook, ANZ has now ruled out any further RBA cash rate cuts this cycle; a meaningful shift given it had previously expected one more cut in early 2026.

With ANZ changing its forecast, three of the big four major banks: CBA, NAB and ANZ, now expect the cash rate to remain on hold through 2026, with no further cuts in this cycle.

That leaves Westpac as the outlier, still forecasting two more cuts: one around May 2026 and another around August 2026.

Of course, the convergence of three majors around “no more cuts” will shape consumer confidence, pricing behaviour, lending strategy and, ultimately, property demand.

Why ANZ has changed its mind

The logic behind ANZ’s shift is pretty straightforward:

-

Inflation is “moving in the wrong direction”

-

Unemployment has eased back to 4.3%

That combination makes further cuts hard to justify.

When inflation stops declining convincingly and the labour market stays tight, the RBA’s incentive to “support the economy” with lower rates fades quickly.

And it’s not just a case of “no cuts.” The more confronting implication raised in the release is this: some economists are now suggesting the next move could be up rather than down.

Canstar’s Data Insights Director, Sally Tindall, captures the key message in a way borrowers can’t ignore:

“ANZ has joined a growing cohort of economists who now believe we’ve hit the bottom of the cash rate cycle.

While the RBA is unlikely to start hiking rates without plenty of notice, if inflation continues to move in the wrong direction, the next move from the central bank could be up rather than down.”

Note: Now that’s not fear-mongering. It’s a reminder of how central banking works: inflation is the boss, and when inflation misbehaves, rate cuts become politically uncomfortable and economically risky.

Borrowers: most say they’re “prepared”… but a third are not

Canstar’s Consumer Pulse data shows:

-

66% of borrowers say they’re prepared for rates to remain on hold in 2026

-

23% say they’re not prepared

-

11% aren’t sure

So one in three borrowers are either under pressure or uncertain, and that matters because household cash flow is still the backbone of housing market sentiment.

But “prepared” is a slippery word. Some people feel prepared because they’ve tightened spending.

Others feel prepared because they assume wages will rise, tax cuts will help, or refinancing will remain easy.

And that’s where risk creeps in: comfort based on assumptions is not the same as financial resilience.

The practical truth: even without RBA cuts, you can still lower your rate

This is the part many borrowers miss.

Even if the RBA keeps the cash rate on hold, your mortgage rate is not set in stone, especially if you’re on a variable rate and haven’t negotiated in years.

Canstar’s tracking shows there are still sharp deals available, with the lowest variable rates around 4.99% and the lowest fixed rates around 4.64% (for qualifying borrowers and specific loan criteria).

Yes, some banks are lifting fixed rates, but that reinforces the message that lenders are positioning for a world in which funding costs don’t fall further.

Ms Tindall expalins:

“Variable borrowers staring down the barrel of no more cash rate cuts should know they can still take matters into their own hands, whether that’s refinancing to a more competitive lender or haggling with their existing bank.”

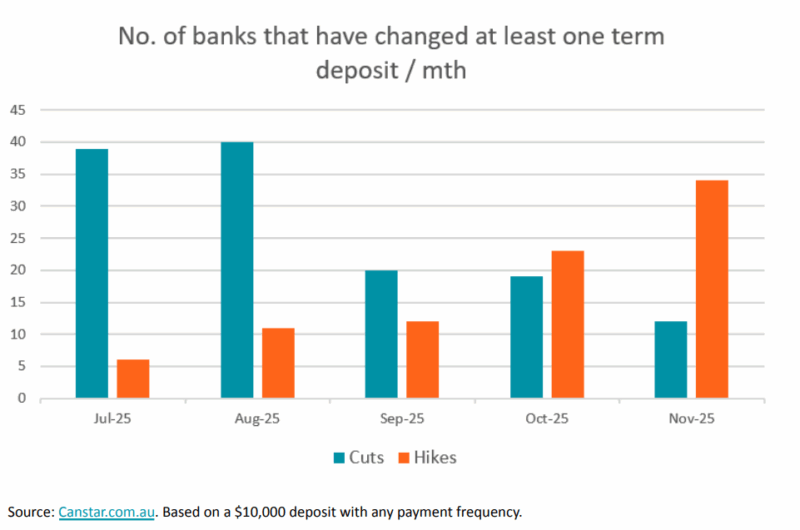

The “canary in the coal mine”: term deposits are sending a loud message

If you want a forward-looking clue about where markets think rates are heading, watch term deposits, because banks don’t price term deposits based on hope.

They price them based on:

-

competition for funding,

-

expected wholesale funding costs,

-

and what they think the cash rate will do over the relevant period.

Canstar’s data shows 34 banks increased at least one term deposit rate in November, compared with just six in July.

Now that’s a big shift in a short time

Ms Tindall notes:

- Also read:Melbourne property market forecast for 2026 | Is it a good time to invest in Melbourne?

- Also read:Latest Property Price Forecasts Revealed. Australian Property Market Outlook 2026: Where To Now After The Rate Rise.

- Also read:Brisbane Property Market Forecast [2026] – What’s Ahead & Where to Invest

- Also read:Sydney property market forecast for 2026. Is it a good time to invest in Sydney?

- Also read:Perth housing market update | March 2026

“Certainly, if term deposit rates are the canary in the coal mine, then further cash rate cuts are unlikely.”

In other words, the “easy money” era is well and truly behind us, and markets are adjusting to a more normal cost of capital.

What this means for property investors

1. Rate stability can be bullish for property, even if rates are higher than we’d like

Markets like certainty. When buyers believe rates are stable, they stop waiting for the perfect moment and start acting.

When enough people stop waiting, demand for property firms.

2. The next phase rewards quality and strategy, not shortcuts

If further rate cuts aren’t coming to “save” poor deals, the gap widens between:

-

investment-grade assets (scarce, desirable, high land value, in strong locations), and

-

secondary assets (compromised location, oversupply risk, weak owner-occupier appeal).

This is the cycle where A-grade outperforms, and B/C-grade gets exposed.

3. Serviceability becomes the filter, and filters change who can buy what

When rates stay higher for longer, borrowing power stays constrained.

That doesn’t kill property markets, it reshapes them:

-

owner-occupier “heartland” markets with deep demand stay resilient,

-

compromised stock takes longer to sell,

-

while well-located properties with strong appeal continue to attract competition.

4. Investor psychology matters more than interest rates

When people believe cuts are coming, they feel optimistic and stretch.

When they believe cuts are not coming, they become selective. That’s not bad, it’s healthy.

It pushes investors back toward fundamentals: cash buffers, income resilience, asset quality, and long-term thinking.

What I’d do next (for homeowners and investors)

Here’s the action plan I’d be working through right now:

For homeowners

-

Pressure-test your budget at today’s rate for 12–24 months (not “until cuts arrive”).

-

Call your lender and ask for a pricing review, especially if you have a strong repayment history.

-

Compare refinance options properly (fees, revert rates, offset structure, cashback traps, serviceability rules).

For property investors

-

Assume the current rate environment is the base case and buy only if the deal stacks up under that assumption.

-

Build a liquidity buffer (I generally like meaningful buffers, not token amounts, because buffers buy you time and optionality).

-

Prioritise investment-grade assets that will appeal to affluent owner-occupiers over time (that’s where the long-term price pressure comes from).

-

Review your debt structure: split loans, offsets, deductibility, risk management, and flexibility matter more than squeezing out the last 0.10%.

- Seek advice from an independent property strategist, like the team at Metropole, to help you understand your options. Find out more about this service here and lock in a chat with one of our wealth strategists.

For savers (and I know many investors also hold cash strategically)

Ms Tindall also points to “laddering” term deposits: spreading money across different terms to keep flexibility while still accessing competitive rates:

“Laddering can be one way to keep your options open… locking in smaller pots of money at different times."

It’s not for everyone, but if you’re holding cash for a future purchase or keeping reserves, it’s worth considering.

The bottom line

If three major banks now expect no further cuts, and term deposit pricing is rising, the message is simple:

Tip: Stop waiting for cheaper money. Start making strategic decisions in the market we actually have.

Because the investors who do well in this next phase won’t be the ones who guessed the next RBA move.

They’ll be the ones who bought well, managed risk, and stayed patient while others hesitated.