If you own a property that you suspect may not be investment-grade, how do you work out if it is worth selling and replacing it with a better-quality property?

Risks and costs associated with replacing a poor investment

Replacing an investment asset comes with risks and several costs:

- Asset selection risk: This is the risk that the replacement asset does not deliver materially better future returns than your existing asset, either because you purchased an impaired property, due to general market conditions or maybe your existing property does not perform as poorly as you expect.

- Selling costs: Selling a property takes time and incurs costs. You may need to make minor cosmetic improvements to ensure the property is well presented. It’s often best to sell a property when it’s vacant, so the cost of vacancy should be factored in. Additionally, you’ll need to pay a fee to the selling agent and likely incur advertising and staging costs also.

- Rebuying costs: You will need to pay stamp duty, and if you use a buyer’s agent (which I recommend), that cost should also be included. In addition, there are legal fees and other expenses, such as building and pest inspections.

- Capital gains tax (CGT): While CGT cannot be avoided, it can only be delayed. But the longer you delay paying tax, the better off you are.

Set a realistic expectation and benchmark

It’s important to have realistic expectations when it comes to long-term investment returns.

For example, you cannot expect an entry-level one-bedroom, investment-grade apartment to deliver the same total returns as an investment-grade house.

Generally, an investment-grade house is likely to provide higher returns.

Historically, houses in Melbourne and Sydney have delivered an average return of around 9.7% p.a., which includes both rental income (before expenses) and capital growth.

To be conservative, I think a gross long-term return of 9% p.a. is a reasonable expectation for investment-grade houses.

Of course, the goal is to exceed this return, but for the purposes of planning, it is important to be conservative.

The location and type of property play a significant role in whether this 9% p.a. benchmark is achievable and the components (income vs growth) of the return.

For example, a property in a small regional town with an oversupply of vacant land and very low demand will almost certainly fail to achieve a 9% p.a. total return over the long run.

However, a house in an established, blue-chip suburb in Melbourne or Sydney is much more likely to meet or probably exceed this benchmark.

The location also affects the components of return. If we accept that supply and demand fundamentals in regional locations are not the same as in capital cities, a reasonable long-term total return in those areas might range from 6% to 7.5% per annum.

Therefore, if houses are yielding 4% in rental returns, it would be reasonable to expect long-term capital growth is likely to be in the range of 2% and 3.5% p.a., on average.

Expecting higher growth over the long run would be unreasonable because the total return is too high.

In this blog, I outline three key attributes that a property must possess to be considered investment-grade:

(1) a persistent imbalance between demand and supply,

(2) strong historical growth, and

(3) a large proportion of the property’s value in the underlying land.

Due to these attributes, investment-grade properties tend to deliver most of their return from capital growth, with relatively low income.

As such, the benchmark for long-term annual returns from investment-grade properties I use when planning is 2% in rental yield plus 7% in capital growth.

Form a review regarding future expected returns

If you own a property and are uncertain whether to retain it or sell, it’s essential to form a realistic expectation of future long-term returns.

While rental yields can fluctuate in some locations, they tend to be relatively stable over time.

Therefore, you can probably base your income return expectations on the current rental yield, which is calculated by dividing the annual rental income by the property’s market value.

The growth return will then be the difference between the total expected return and the rental yield.

Please be careful about relying too heavily on recent shorter-term returns when setting expectations for the future.

As I have mentioned frequently in this blog, property markets operate in two cycles: flat and growth.

If your property has been in a growth cycle over the last 5-10 years, it’s reasonable to expect that the market will experience a flat cycle, as returns revert to their long-term averages.

For this reason, it is often best to look at multi-decade capital growth data when formulating return expectations.

Once you have established an estimate of what your property might return in the future, over the long run, you must compare it to investment-grade property returns.

As discussed above, I use 2% p.a. in rental yield plus 7% p.a. in capital growth.

Estimate how much better off you might be

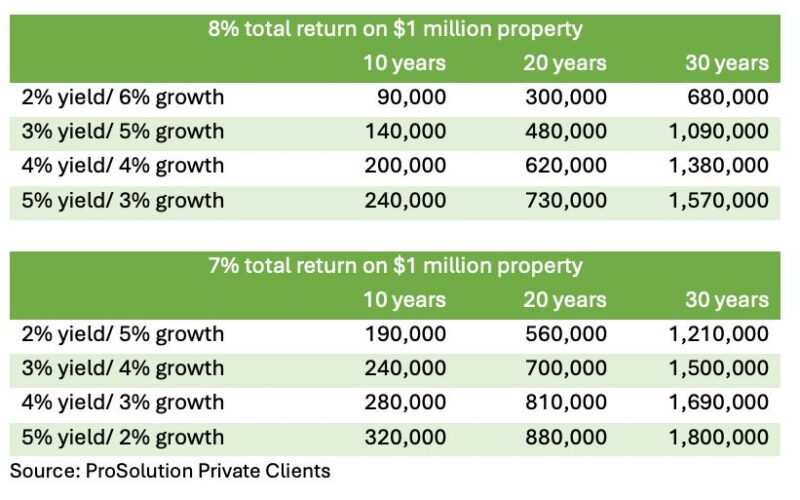

The tables below compare the difference in net wealth (in today’s dollars, after tax) between holding onto a sub-grade property versus selling it and investing in an investment-grade asset.

This analysis only applies if you determine your property is not investment grade, so I have prepared two tables: one assuming an 8% p.a. total return (1% below investment grade) and another assuming a 7% p.a. total return (2% below investment grade).

The tables show outcomes based on various combinations of income and growth returns over different time periods.

Here’s how to interpret these tables: For instance, if I believe my substandard $1 million property will generate 4% income and 4% growth annually, selling this property and purchasing a $1 million investment-grade asset would leave me $200,000 better off in today’s dollars after tax in 10 years.

In 20 years, the difference would be $620,000, and in 30 years, it would be almost $1.4 million – all in today’s dollars.

These tables are based on a $1 million property, so you will need to adjust the numbers according to your property’s value.

- Also read:Australian housing market update | July 2026

- Also read:Melbourne property market forecast for 2026 & 2027 | Separating the fundamentals from the sentiment

- Also read:Brisbane Property Market Forecast [2026 & Beyond] – What The Olympics Decade Means for Investors.

- Also read:Sydney property market forecast for 2026 and 2027 | Why the short-term softness is a long-term opportunity

- Also read:Latest Property Price Forecasts. Australian Property Market Outlook 2026-2027: Navigating a Market Correction

For instance, if your property is worth $700,000, simply multiply the figures below by 0.7.

If your expected total return is lower than 7% p.a., you can likely estimate your results by extrapolating from these tables.

How significant are the transactional costs?

As mentioned earlier, there are several transaction costs involved in replacing an underperforming property, and these should be factored into the analysis, except for CGT.

The reason for excluding CGT is that it is already accounted for in the figures above, as these amounts are represented on an after-tax basis.

I feel this approach is reasonable, given that property investments are typically made to fund retirement, and eventually, the property will need to be sold.

CGT can be delayed but never avoided.

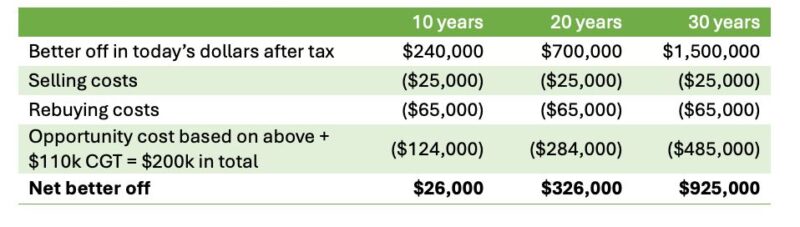

Therefore, when assessing the benefits of replacing a poor-quality asset, you should subtract transaction costs and the opportunity cost from the projected benefits.

The formula is:

After-tax improvement in wealth – selling costs – buying costs (such as stamp duty and buyer’s agent fees) – opportunity cost = net benefit.

What is the opportunity cost?

It’s important to account for the opportunity cost of paying taxes and expenses sooner than expected.

While you may need to pay CGT one day, it is better to defer that payment for as long as possible than to pay it today.

To calculate the opportunity cost, add up all transaction costs, including selling costs, buying costs, and CGT, and estimate the opportunity cost based on the table below.

The table below calculates what return you could earn on those monies if these expenses were avoided or delayed (the amounts are after-tax and in today’s dollars, assuming a 7% p.a. return).

An example of the full calculation

Perhaps this is best illustrated using an example. Assume I expect my property to deliver a return of 3% income and 4% growth.

This is how I would calculate if I would be better off:

Key matters to consider

These numbers only get you part of the way.

You need more context to help you make a firm decision.

Can you afford to buy a superior-quality replacement asset?

Does your financial position and borrowing capacity allow you to purchase an asset that is materially better quality?

How sensitive are you to underperformance?

It’s important to assess whether the underperformance of an investment will impact your retirement outcomes.

If you already have enough assets to fund your retirement, it might not be worth the risk of replacing an investment unless the numbers clearly show you will be significantly better off.

However, if your financial situation means that every dollar counts and could make a substantial difference, then optimising your investments becomes more important.

Time until retirement or sale

Clearly, the longer your investment horizon, the more important it becomes to optimise your investment assets.

However, if you plan to sell an underperforming property within the next decade, it’s probably unlikely that replacing it now will provide a better outcome.

Can you replace the asset without selling it?

If I am concerned that one of my clients’ properties might not deliver investment-grade returns, I will consider buying a replacement property and holding onto both, if possible.

If the existing property does end up underperforming, we can sell it in the future, but at least we will already have a replacement asset in place.

This approach helps hedge our position.

This is information, not advice

I have done my best to write this blog so that it is helpful to a wide audience, clearly outlining our approach to this topic.

However, it’s important to recognise that individual circumstances can vary, and there may be specific factors or nuances to consider.

Therefore, please view anything discussed in this blog as general information rather than personal advice.