The Reserve Bank's latest figures showed credit growth slowing to 4.4 per cent, down from 5.2 per cent a year earlier, and broad money growth at fresh quarter-century lows of just 1.86 per cent.

While it may be a happy new year for most of us, it's not so much for bankers, with lending growth continuing to flounder.

- Also read:Brisbane’s property market forecast for 2025

- Also read:Melbourne property market forecast for 2025

- Also read:Latest property price forecasts for 2025 revealed. What’s ahead in our housing markets in the next year or two?

- Also read:Sydney property market forecast for 2025

- Also read:Home Prices Surge Following Rate Cut | Latest Housing Market Stats Dr. Andrew Wilson

It was noteworthy to hear last week that the RBA has been watching the gross household debt-to-income ratio as a main point of concern, especially as this ratio has already peaked is now falling.

The distinction from housing debt-to-income was quite interesting (to me at least) as the lines between housing, small business, and personal credit are blurred at best, with small business loans often secured against a home, and so on.

Property is a game of finance

As you can see in the chart below, changes in the direction of housing credit growth have tended to lead changes in dwelling price growth.

You can also see that no such change had occurred by the end of November 2018.

A simple credit impulse model as favoured by ANZ economists suggests that capital city (i.e. Sydney and Melbourne) dwelling price declines should moderate, although there are several factors unique to this cycle - not least the boom and bust in Chinese investors - that could throw the model a bit off course (this may have already happened to some extent since 2014).

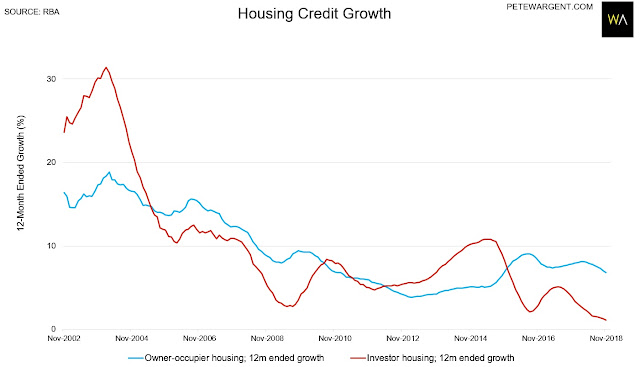

Lowest investor credit growth on record.

Investor credit growth was already at the lowest level on record, and it fell to even lower levels last month, allowing APRA to remove another of its now-redundant arbitrary caps, this time on interest-only lending.

Given the enormous growth in the population aged 25 to 34 in particular, this is now a remarkably low level of growth in investor credit, even if it did follow on from a boom.

Not surprisingly the growth in owner-occupier credit also declined for a ninth consecutive month.

CoreLogic will release its latest home value index for the month of December, and this will show significant declines for Sydney and Melbourne in 2018.

The wrap

In short, business credit was moderate, personal credit was negative, and housing credit has no pulse - let's hope that doesn't turn into a full-blown coronary.