Key takeaways

Booming capital city housing markets have continued to surge in February despite an increase in official interest rates.

Overall results however, were mixed, with seasonal impacts continuing to subdue notably the Melbourne and Sydney markets.

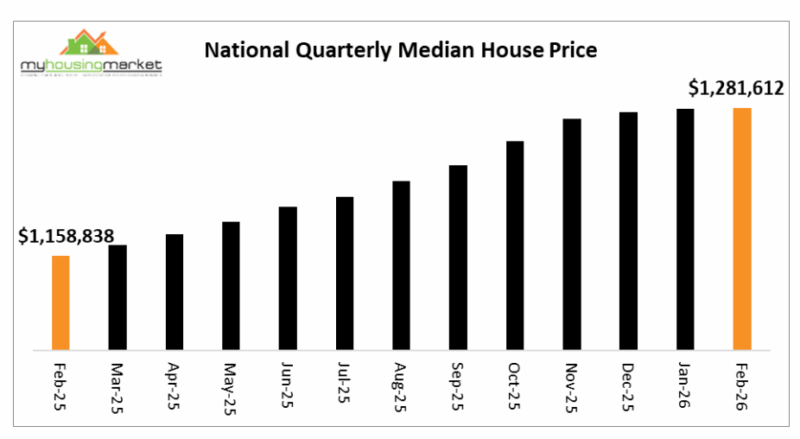

The national capital city median house price increased marginally by 0.1% over the February quarter to $1,281,612 compared to the January quarter, according to the latest data from My Housing Market.

Annual national house prices however are now higher by 10.6% and have increased over 12 consecutive months.

Booming capital city housing markets have continued to surge over February despite an increase in official interest rates. Overall results however were mixed, with seasonal impacts continuing to subdue notably the Melbourne and Sydney markets.

The national capital city median house price increased marginally by 0.1% over the February quarter to $1,281,612 compared to the January quarter, according to the latest data from My Housing Market.

Annual national house prices however are now higher by 10.6% and have increased over 12 consecutive months.

The boomtime housing markets of Darwin, Perth, Brisbane and Adelaide have continued to surge into 2026 with each reporting more robust results over February.

House price growth in other capitals however was mixed, with prices in Melbourne and Sydney continuing to fall reflecting the usual impacts of significantly reduced early year buyer and seller activity in those cities.

Annual growth rates over February have increased in all capitals except Melbourne and Darwin compared to the previous months results

Adelaide was the top monthly performer with house prices higher by 2.0% closely followed by Perth up 1.8%, Darwin up 1.6%, Brisbane higher by 1.1% with Canberra up 0.5%.

House prices in Sydney fell by 0.3% over the month with Hobart down 0.5% and Melbourne falling 1.5%.

Darwin, Perth, Brisbane, and Adelaide continue to report clearly the highest annual house price increases - up by 25.1%, 20.5%, 17.6% and 15.4% respectively.

Quarterly Median House Prices February 2026

| Median | Month | This Year | 1 Year | 2 Year | |

| Sydney | $1,764,491 | -0.3% | -0.6% | 7.5% | 11.6% |

| Melbourne | $1,097,125 | -1.5% | -2.2% | 5.2% | 4.7% |

| Brisbane | $1,186,136 | 1.1% | 1.7% | 17.6% | 30.9% |

| Adelaide | $1,121,919 | 2.0% | 2.1% | 15.4% | 26.4% |

| Perth | $1,174,190 | 1.8% | 4.9% | 20.5% | 43.4% |

| Hobart | $738,964 | -0.5% | -1.4% | 11.0% | 8.8% |

| Darwin | $770,516 | 1.6% | 1.3% | 25.1% | 24.4% |

| Canberra | $1,015,182 | 0.5% | 0.7% | 9.7% | 7.1% |

| National | $1,281,612 | 0.1% | 0.3% | 10.6% | 16.6% |

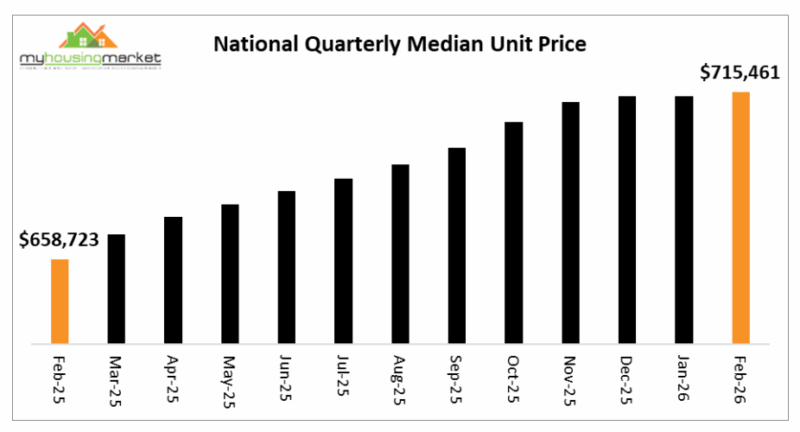

National unit prices also higher

National unit prices were also higher over the February quarter compared to the January quarter, rising by 0.2% to $715,461 – and have now increased by 8.6% compared to the February quarter 2025 result.

Darwin was the top monthly performer over February with unit prices rising by 4.0% followed by Brisbane up 3.7% with Perth higher by 2.3% and Adelaide up 1.5%. Canberra and Melbourne unit prices however each fell by 0.4 % with Sydney and Hobart each falling 0.6% over the month.

Quarterly Median Unit Prices February 2026

| Median | Month | This Year | 1 Year | 2 Year | |

| Sydney | $807,547 | -0.6% | -0.2% | 4.8% | 7.7% |

| Melbourne | $582,795 | -0.4% | -2.6% | 5.9% | 4.8% |

| Brisbane | $749,440 | 3.7% | 5.5% | 27.8% | 56.7% |

| Adelaide | $621,199 | 1.5% | -1.4% | 16.1% | 35.0% |

| Perth | $652,206 | 2.3% | 5.1% | 25.2% | 51.3% |

| Hobart | $539,938 | -0.6% | 0.7% | -3.9% | 12.9% |

| Darwin | $443,187 | 4.0% | 2.9% | 25.6% | 23.1% |

| Canberra | $500,766 | -0.4% | -1.4% | -0.4% | -0.2% |

| National | $715,461 | 0.2% | 0.2% | 8.6% | 13.8% |

Similar to houses, Brisbane, Darwin, Perth, and Adelaide continue to record clearly the highest annual unit price growth to February 2026. up by 27.8%, 25.6%, 25.2% and 16.1% respectively.

Comment

Capital city home prices have generally remained resilient over February despite an increase in RBA interest rates, with a number of markets continuing to report boomtime results carrying over from strong 2025 market conditions.

Seasonal conditions however continued to impact markets as a result of typically reduced numbers of early-year buyers and sellers.

Capital city home auction markets remained largely dormant over the quarter impacting the price mix of homes transacted, with a significantly lower proportion of higher prices homes in the market – particularly in Sydney, and Melbourne.

2025 was a strong year for home price growth generally as RBA reductions of official interest rates in February, May and August significantly improved housing affordability and enhanced buyer and seller confidence in chronically undersupplied housing markets.

House price outcomes were mixed over February 2026 with Adelaide, Darwin, Perth and Brisbane again boomtime performers, however prices in Sydney and Melbourne were lower particularly reflecting local auction markets generally in recess.

Unit price growth was also mixed, albeit positive overall through February, with annual results in Brisbane, Perth, Darwin and Adelaide continuing to clearly lead the capitals, and adding to extraordinary price increases in those cities over the past 2 years.

2026 is set to continue to produce home prices growth for most capitals although the rising spectre of multiple interest rate increases will act to dampen affordability and confidence. Buyer and seller momentum however will continue to drive housing markets particularly the booming markets of Adelaide, Darwin, Perth and Brisbane that are again set to lead capital city outcomes for both houses and units - although results are unlikely to match the extraordinary 2025 results.

Sydney will likely continue to report solid results, with the Melbourne market having revived moderately through 2025 looking to consolidate the gains of the previous year.

Underlying drivers continue to support housing market activity generally, although the February RBA rate rise is now likely to be followed by more increases over the shorter-term with inflation continuing to rise and now consistently above the RBA target range.

The economy however remains clearly strong with continuing low jobless rates, high jobs growth and falling unemployed.

High housing demand continues to outpace low and diminishing housing supply and although high post-COVID migration levels have clearly eased recently, numbers remain robust and will add to chronic housing undersupply supporting high rents and low vacancy rates generally in capital city rental markets. Following a period of easing rental growth, the latest data is reporting continuing low home rental vacancy rates overall with rents predictably now on the rise again.

High rents and higher prices continue to provide clear incentives for first home buyers and investors chasing solid investment returns. Ongoing government initiatives to support first home buyers will increase demand and act to place upward pressure on prices. Government proposals to manipulate housing demand through changes to the tax system however remain problematic with the real prospect of uncertain and unintended consequences.

Capital city housing markets generally recorded higher house and unit prices over 2023, 2024 and surged over 2025 fuelled by rising buyer and seller confidence through sharp cuts to interest rates.

2026 is again set to report higher home prices driven by a continuing strong economy, chronic low levels of new home construction, rising underlying demand and continuing solid housing market momentum - although at lower levels than 2025 and clearly dampened by the increased likelihood of rising inflation and higher RBA interest rates.

- Also read:Booming Housing Markets Rise Over February | Latest stats from Dr. Andrew Wilson

- Also read:Why Testamentary Trusts Aren’t Just for the Rich: A Guide to Safeguarding Your Legacy Introduction

- Also read:Why the ALP’s Grand Plan to Build 1.2 Million Homes Is Destined to Fail – A Reality Check

- Also read:Here’s how I’ll be investing in property in 2023