Most people assume that if costs rise due to a shock - such as the current Middle East shenanigans - they will fall back once things settle.

But economics and, moreover, business doesn’t work that way. Prices move up quickly with rising costs, but they rarely come back down in any meaningful way.

“Up like a rocker, down like a feather” is frequently referenced by economists, pundits and in public discourse regarding fuel prices and inflation.

It also applies very much to housing construction prices, their escalation and future direction too.

Think staircase not cycle

Housing construction costs do not move like a wave. They move like a staircase.

Each shock - whether it was GFC, Covid and now the 2026 Iran war, to cite three more recent examples - pushes the cost base higher. Then it holds. Then the next shock arrives.

There are structural reasons for this.

Labour costs rise and stay there. Skilled labour remains tight. Productivity in housing construction has gone backwards, not forwards. It takes more time and more effort to deliver the same outcome.

Regulation is cumulative. Every code change, every compliance layer, every additional requirement adds cost. None of it unwinds. In fact in Australia this seems to be getting worse.

For example, as of 2026, new free-standing homes (Class 1 buildings) in most Australian states and territories must meet a minimum 7-star energy rating under the Nationwide House Energy Rating Scheme (NatHERS). This cost impost is projected to add another $20,000 to $40,000 per new home, depending on design, size and inclusions. It is yet another step in the staircase.

As a result building risk is now priced differently. Builders absorbed heavy losses through Covid. The response has been more margin, more contingency, and more caution.

And expectations reset. Developers run feasibility at the new numbers. Valuers anchor to recent evidence. Buyers recalibrate what this new normal looks like.

The system re-prices itself and then holds. That is why costs don’t come back down.

Step 1 - The GFC

But before we revisit Covid’s impact, let’s go back to where the current building staircase started, the Global Financial Crisis.

The GFC didn’t just hit demand, it reset the entire cost structure of housing.

In response, governments intervened, regulation increased, and risk was priced more conservatively across the system.

Construction costs didn’t fall back, they established a new floor. From that point on, housing became more complex, more regulated, and more expensive to deliver.

It was the first clear reminder that prices rise easily, but rarely come back down.

Step 2 - Covid

Then came Covid.

Covid delivered a full system shock to housing costs. Materials surged, labour tightened, and supply chains broke under pressure.

Governments then poured fuel on demand through stimulus, pushing prices even higher. Construction costs rose by around 40% in the five years to 2025.

In many cases, that added well over $100,000 to the cost to build the average Australian home.

Then conditions began to ease. Freight improved, timber and other major input prices settled down, and lead times shortened. But overall building costs did not come back down. They settled at a higher level instead.

Step 3 - Now

Which brings us to today.

We are now layering another shock on top of that higher base.

I labeled the current Middle East war, Covid Mark 2.

Energy markets are volatile again. Freight costs are rising. Geopolitical tensions in the Middle East are feeding directly into fuel, materials and logistics.

And this matters more than it might appear. Because pricing is forward-looking and hydrocarbons are in almost everything.

Also being a vast island at the arse end of the world that increasingly depends on imports for our energy needs doesn’t help matters. Nor does our reliance on diesel to move most things across the country.

Moreover, firms don’t just respond to today’s costs. They price based on what they think costs might be tomorrow. If uncertainty remains, prices stay elevated as a form of insurance.

This creates what economists call a ratchet effect. I have called it a staircase.

The potential impact

Who really knows what’s in store next. But I will place a large bet that it isn’t a return to smooth sailing and calm waters.

Economic shocks seem to be gathering pace and increasingly happening on multiple fonts.

My comments below are based on the current scope of the Middle East conflict and they assume a somewhat satisfactory resolution - and with that a return to somewhat normal conditions in the Strait of Hormuz - in plenty of time before the American mid-term elections.

By this I mean that it is all done and dusted by the end of June this year.

On this basis, and for now, I want to leave my earlier housing market outlook commentary intact as I want to review matters in coming weeks and report back after Easter.

By then, fingers crossed, there will be more clarity in the direction of events across the Middle East.

To recall I said just two months ago that Australian dwelling values are likely to increase during 2026.

But - as notedat the time - more slowly and unevenly. Growth of 2% to 6%, I said, appeared realistic. Importantly this year, I also said, was likely to be the end of the current housing upswing.

I followed this commentary with a statement that beyond 2026 Australian dwelling price growth looks more pedestrian than spectacular. I added that the housing market was unlikely to fall far, but it was also very unlikely to run hard; saying the same forces that limit price declines also cap upside. Those included higher interest rates, tighter credit and stretched affordability.

At the time of writing I questioned myself, thinking that maybe my comments were too pessimistic. Well they might turn out be optimistic given the current state of play.

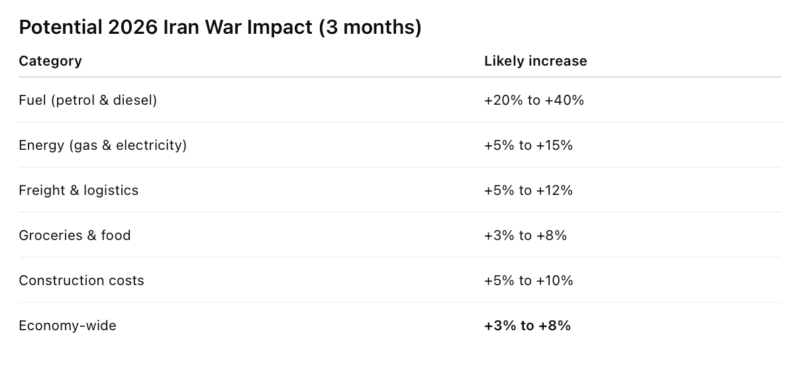

I do think - and assuming again a somewhat quick (and somewhat complete) resolution of the current Middle East conflict and associate issues - that costs across Australia will lift substantially, and maybe as high as 40% on some items - by the end of June.

Construction prices are expected to lift by 5% to 10%. General prices by 3% to 8%.

Costs will then, given the content of this post, most likely settle at new highs and not that far off those new peaks.

And for what it’s worth, if this stays contained to Iran and drags on for six months, not three as per the table above, then construction costs could lift by about 15%.

If it spills beyond Iran - in aggression terms, not just defence - then you’re likely looking at closer to a 20% lift in building costs, and around 15% across the broader cost base. And you can forget about driving anywhere easily.

The IMF has estimated that for every 10% lift in the price of oil, global inflation lifts 0.4%.

Since the conflict kicked off in late February 2026, global oil prices have risen roughly 40%, with spikes even higher at times.

So this means inflation is likely to rise by at least 1.6%, thereby lifting Australia’s CPI from 3.7% to 5.3%.

Let’s hope this gets resolved quick smart and that Iran’s Mullah’s, the Iranian Islamic Revolutionary Guard or Thump don’t escalate matters further.

Moreover, that China doesn’t use the current situation to take control of Taiwan. Or that Russia doesn’t further escalate hostilities in Ukraine or worse still invade elsewhere across Europe.

Plus fingers crossed that Pakistan and Afghanistan can keep a lid on current hostilities. The list seems endless. And I must have missed a few, like Gaza, but I am not alone in forgetting about that.

If we face another major economic shock or two now, well all bets are off.

My end note (for now)

Another inflationary bout matters because it changes how we think about housing supply.

If feasibility does not work today, it will not magically fix itself tomorrow through cheaper inputs or even supply of more skilled migrant labour (and more on this after Easter too).

Higher prices will also reduced housing demand. It will also increase sales risk. Most buyer segments - including the more affluent baby boomers - are already baulking at current new dwelling price points.

The only real levers left are the hard ones.

Build smaller. Build differently. Use land more efficiently. Improve productivity. Speed up decision making. Rethink design. Better understand what your target market really wants. Or build less.