Key takeaways

Cotality’s Home Value Index rose 0.7% in August — the strongest monthly gain since May 2024 — pushing annual growth to 4.1%.

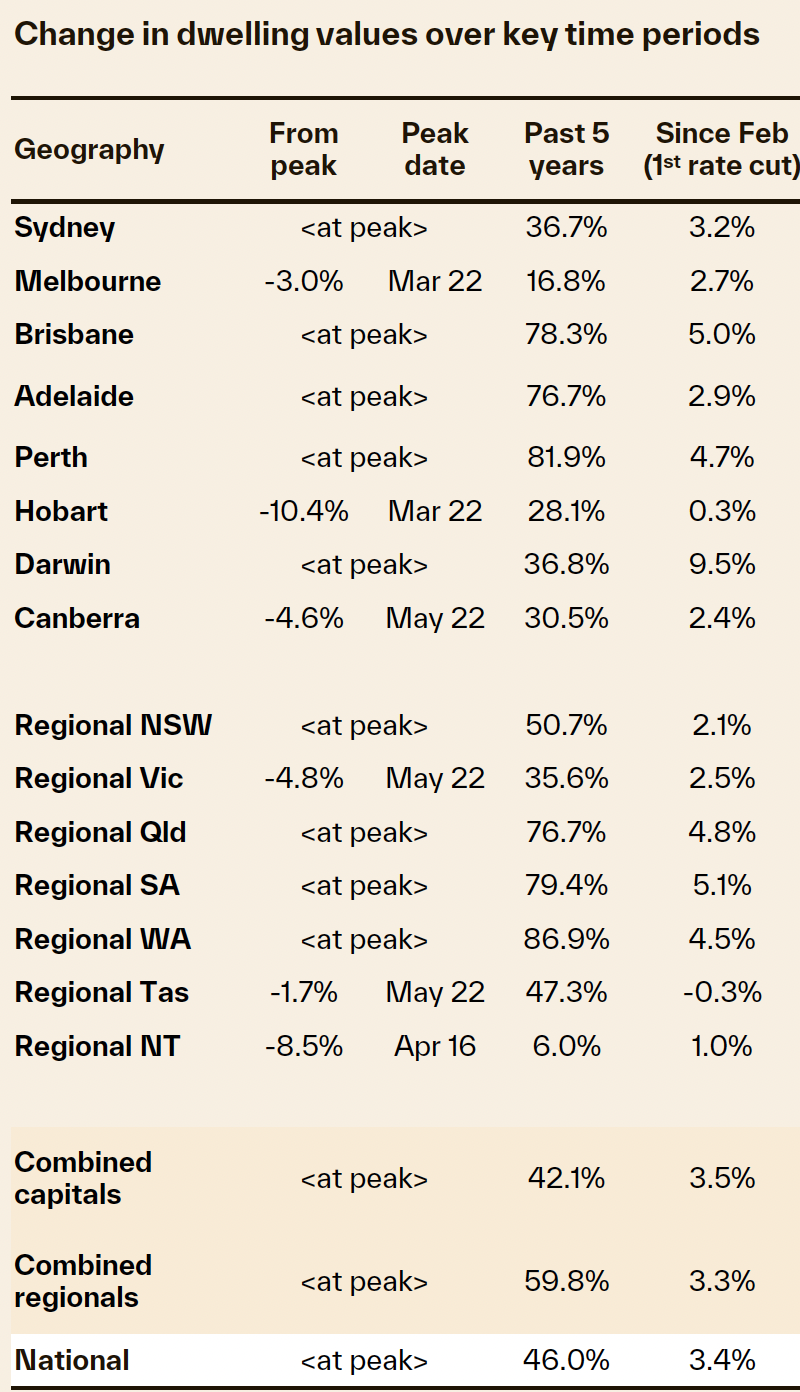

Buyer demand is outpacing supply, with advertised listings 20% below average and auction clearance rates hitting 70%, the highest since early 2024.

Vendors are entering spring in a strong position, with low competition and rising prices across nearly all regions.

The growth cycle has been gradually building momentum since the February rate cut, with buyer demand spurred by a lift in borrowing capacity, real wages growth, rising confidence and what is likely to be a growing sense of urgency as advertised stock levels remain tight.

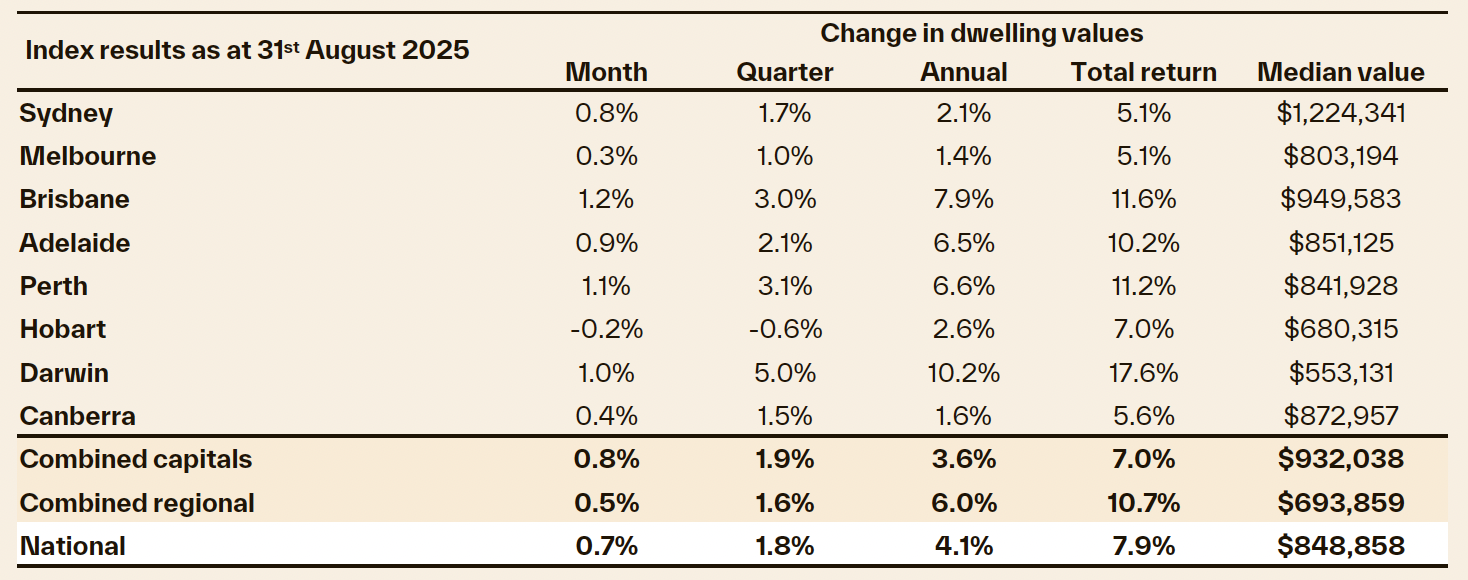

Cotality’s national Home Value Index (HVI) rose 0.7% in August, the strongest month on month gain since May last year.

The result pushed the annual change higher for the second month in a row, to 4.1%.

The growth cycle has been gradually building momentum since the February rate cut, with buyer demand spurred by a lift in borrowing capacity, real wages growth, rising confidence and what is likely to be a growing sense of urgency as advertised stock levels remain tight.

Once again, we are seeing a clear mismatch between available supply and demonstrated demand, placing upwards pressure on housing values.,

The annual trend in estimated home sales is up 2% from last year and is tracking almost 4% above the previous five-year average.

At the same time, advertised supply levels remain about -20% below average for this time of the year.

Vendors are in a strong position as we head into spring.

Auction clearance rates rose to 70% in late August, the highest since February last year, and competition amongst sellers is relatively mild amid such low advertised stock levels.

We are starting to see the usual start of spring upswing in new listings coming to market, but from a low base.

A pickup in the flow of stock coming to market through spring will be good news for buyers, who generally have limited choice at the moment.

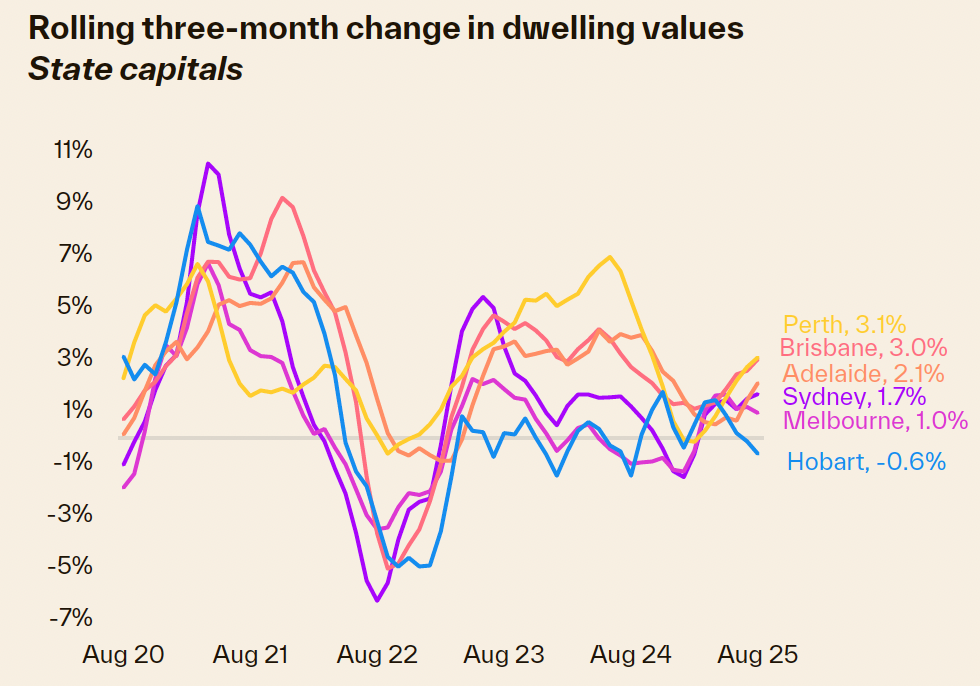

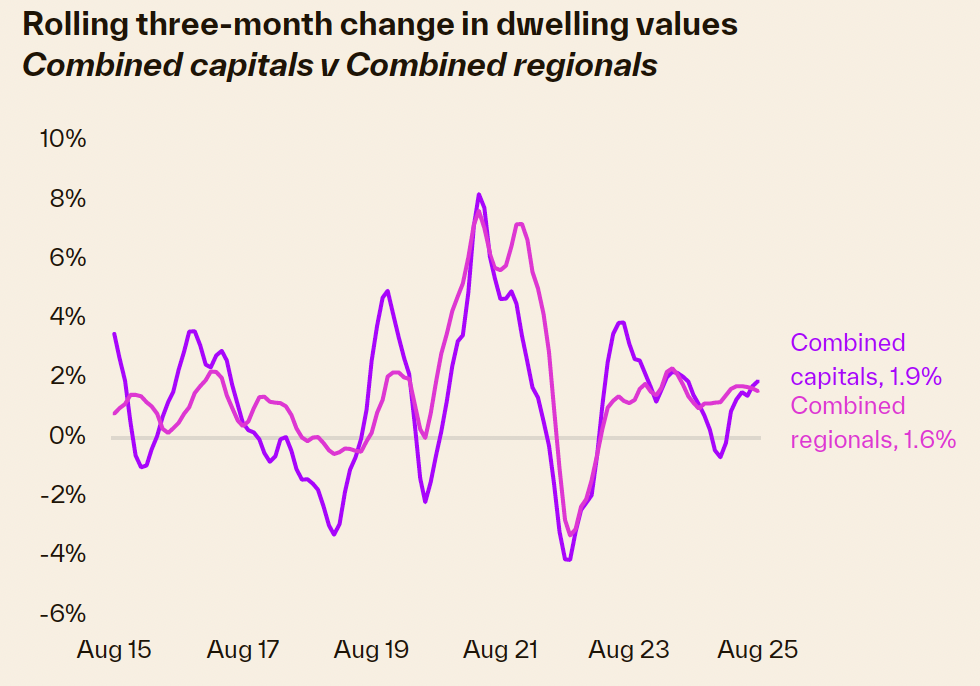

While housing values are rising across most regions, the pace of growth remains modest relative to recent upswings.

During the pandemic, the monthly change in the national index peaked at 3.1% in March 2021, and the upswing commencing in early 2023 climbed quite rapidly, reaching a 1.3% high in May 2023.“I would be surprised if we saw the monthly rate of change in the national HVI getting anywhere near these earlier cyclical peaks, given how stretched housing affordability has become,” Mr. Lawless added.

What is more likely is that home values will rise at a more sustainable pace, with demand dampened by affordability constraints, more normal rates of population growth and cautious lending policy.

While interest rates are falling, the cash rate is still 350 basis points higher than the 0.1% low that underpinned growth in the pandemic.

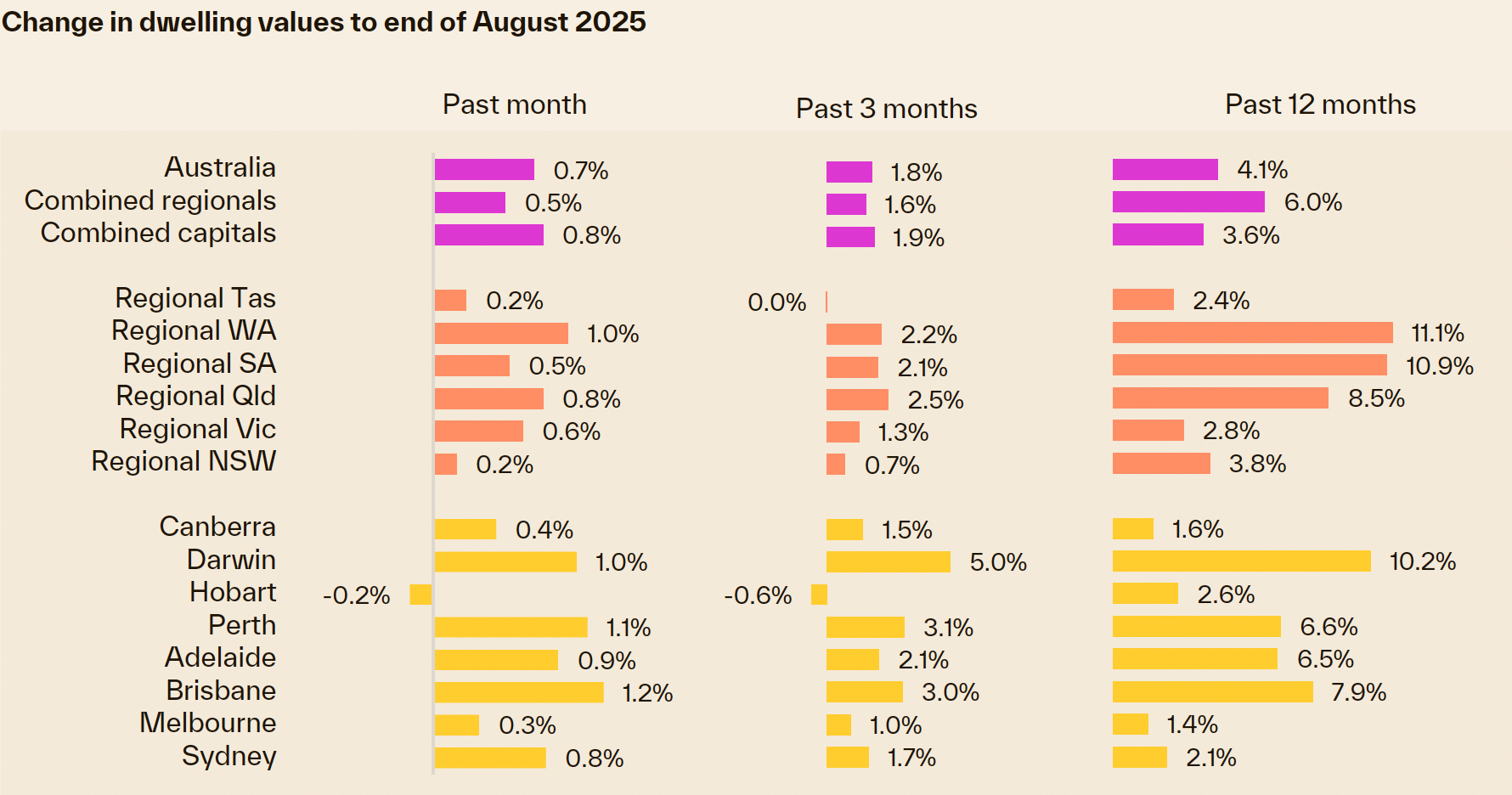

The growth trend remains geographically broad-based, with almost every region recording a rise in values over the month.

Tasmania remains the exception, with Hobart values down -0.2% over the month.

The mid-sized capitals are once again leading the growth trend, with Brisbane (+1.2%) and Perth (+1.1%) recording the highest monthly gains. Adelaide wasn’t far behind with a 0.9% lift in values.

Darwin has also recorded a solid gain, with a 1.0% rise in August, taking values 10.8% higher through the first eight months of the year, by far the highest year-to-date gain across the capital cities.

- Also read:March Home Prices Still Rising | Latest stats from Dr. Andrew Wilson

- Also read:Why Testamentary Trusts Aren’t Just for the Rich: A Guide to Safeguarding Your Legacy Introduction

- Also read:Why the ALP’s Grand Plan to Build 1.2 Million Homes Is Destined to Fail – A Reality Check

- Also read:Here’s how I’ll be investing in property in 2023

It seems that investors are willing to look through the volatile history of Darwin housing trends, with investors attracted to the low price points and high yields. Lending to this segment has more than doubled over the past year.

Additionally, listings are extraordinarily low, down about 50% on the five-year average.

The broad-based rise in housing values is set to continue into spring, a period where we usually see a seasonal uplift in listings.

While a rise in advertised stock levels will test the depth of housing demand, there is a good chance purchasing activity will continue to outpace available supply.

Buyer demand is supported by an increasingly healthy household sector:

- Consumer sentiment reached a 3 ½ year high in August, supported by lower interest rates and easing cost of living pressures. Historically, consumer sentiment and housing activity have shown a close relationship.

- After drawing down on savings accumulated through the pandemic, households are once again managing to accrue savings, with the household saving ratio trending towards pre-pandemic averages in March. While higher savings also imply less consumption, a return to an accrual of savings should help prospective buyers access the credit necessary for a home purchase.

- Real wages growth, at 1.3% per annum, is at its highest level since June 2020 and about 2 ½ times the pre-COVID decade average of just 0.5%. Stronger wages growth, alongside lower debt servicing costs, should help to support purchasing activity and sentiment.

- The jobs market remains tight, with the unemployment rate holding around the low 4% mark or less since the end of 2021, while the underemployment rate, at 5.9% in July, is well below the decade average of 7.9%. Such strong labour market conditions are supporting confidence and the ability to prove up loan serviceability. Furthermore, these conditions, along with very low levels of negative equity, are another reason why mortgage defaults remain so low.

There’s been a clear turnaround for households relative to 2024 when high interest rates and cost of living pressures were weighing on balance sheets and the housing market.

While interest rates are still some way from a stimulatory setting, and cost of living pressures remain, the household sector is now on a much better footing, which is flowing through to the housing sector.

The expanded Home Guarantee Scheme is another factor set to support housing demand.

With unlimited places, no income restrictions and higher price caps, we expect this stimulus measure to be popular with first time buyers from October 1st.

Saving for a deposit is one of the biggest hurdles for accessing home ownership.

Saving a 5% rather than a.20% deposit could shave around 10 years off the time it takes to accrue a deposit in an expensive market like Sydney.

While the scheme is likely to be popular, it doesn’t do anything to address the underlying factors that have caused housing to be so unaffordable in the first place.

Although the outlook for housing markets is looking increasingly positive, some headwinds remain that will likely keep the rate of growth in check.

Stretched affordability is arguably the most significant factor keeping a lid on value growth, but also elevated levels of household debt, a focus on prudent lending standards and normalising population growth are all factors that are also likely to keep the rate of growth below recent cyclical peaks.