Key takeaways

Both CBA and NAB now expect the RBA to increase the cash rate in February, reversing their previous forecasts.

NAB expects two hikes next year, while CBA sees at least one, signalling a clear shift in the economic outlook.

Stubborn inflation, resilient employment, and the RBA Governor’s recent warning have prompted banks to prepare borrowers for a potential tightening cycle rather than cuts.

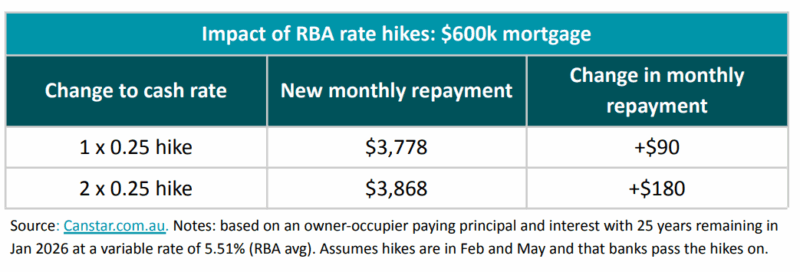

A $600,000 mortgage would rise by $90 per 0.25% hike, meaning two hikes could add $180 a month to repayments, over $2,100 a year. This will particularly affect investors with multiple loans.

NAB and Westpac have lifted fixed rates, and ANZ now offers the lowest big-four 2-year rate at 5.19%. But cheaper lenders outside the big four could save borrowers up to $4,773 over two years on a $600k loan.

Just when many Australians were daring to believe the rate-hike cycle was behind us, the narrative has flipped again.

And boy has it flipped quickly!

Two of our biggest banks—CBA and NAB have now revised their forecasts and expect the RBA to lift the cash rate as early as February 2026.

And that's just six months after the last right cut!

After a few months of optimism that rates had peaked, the conversation is shifting back to hikes, not cuts reflecting a harsh new reality confronting households and the economy.

Inflation was supposed to be beaten, but has instead shown disturbing signs of persistence.

And if you're a property investor or a homeowner, this will means your cash flow, your buffers, and your borrowing strategy are being shaped in real-time.

So let's look at what’s changed, what the banks are now predicting, and what this means for anyone trying to build or hold a property portfolio in today’s environment.

Why the sudden u-turn?

Until recently, both CBA and NAB thought the RBA was done tightening.

But a mix of stubborn inflation, stronger-than-expected economic growth, and the RBA Governor’s own warning has forced them to recalibrate.

NAB now expects two rate hikes—one in February and another in May.

CBA expects one hike in February, but acknowledges more could follow if conditions don’t improve.

ANZ continues to believe the central bank will remain on hold through 2026, though it acknowledges the risk of an early hike has increased following the RBA’s distinctly hawkish tone at its December meeting.

Westpac has now also updated its cash rate forecast, predicting the RBA will keep the cash rate on hold at 3.6% for the foreseeable future.

Previously, Westpac's chief economist Luci Ellis, believed rate cuts were on the horizon later in 2026.

When the big four are this divided, you know we're navigating an unusual economic moment.

What this means for mortgage holders

A rate rise is never “just” a number on a chart; it translates directly into household budgets.

According to the modelling from Canstar, every 0.25 percentage-point hike adds around $90 a month to repayments on a $600,000 mortgage.

Two hikes? That’s $180 a month, or over $2,100 a year.

In a cost-of-living environment where every dollar is already doing overtime, that’s not insignificant.

And for investors managing multiple loans, these incremental increases compound quickly.

Canstar’s data insights director, Sally Tindall, put it bluntly:

“The RBA Governor’s blunt warning last week put the nation formally on notice.

Cash rate cuts are now behind us, and what’s in front could well be a rate hike.

Households with a mortgage should prepare for the possibility of hikes, and not just one… two hikes next year could see their minimum monthly repayments rise by $180.”

This aligns with the broader theme we’ve been discussing for months: Inflation is proving sticky, the labour market is still too tight, and the RBA will not hesitate to act if the data refuses to cooperate.

Fixed rates are rising too, and fast

It’s not just variable-rate borrowers feeling the pressure.

NAB has just hiked its fixed rates by up to 0.20 percentage points, following Westpac’s increases only days earlier.

ANZ now briefly holds the lowest Big Four fixed rate at 5.19% for two years.

- Also read:Home Prices Now Falling Following Rate Rises | Latest stats from Dr. Andrew Wilson

- Also read:Why Testamentary Trusts Aren’t Just for the Rich: A Guide to Safeguarding Your Legacy Introduction

- Also read:Why the ALP’s Grand Plan to Build 1.2 Million Homes Is Destined to Fail – A Reality Check

- Also read:Here’s how I’ll be investing in property in 2023

But even that “lowest” big-four rate is nowhere near the sharpest pricing in the broader market.

According to Canstar’s comparison, the difference between ANZ’s lowest 2-year fixed rate and the lowest rate available anywhere in the market equates to a staggering $4,773 in interest saved over just two years on a $600,000 loan.

That’s effectively an extra monthly repayment simply by shopping around.

So, what should savvy investors do next?

Let’s step back from the noise and look at this strategically.

Rate forecasts shift frequently, but trends matter, and trendlines point to a tighter monetary environment than many expected for 2026.

Here’s how I’d be thinking about this as a seasoned investor:

1. Revisit your buffers now, not later

Assume the hikes will come. If they don’t, great - you’re ahead. But if they do, you’ll be insulated.

2. Stress-test your portfolio at higher rates

Whether you use 6.5%, 7%, or even higher as your testing rate, ensure your cash flows still stack up.

Investors who plan for worst-case scenarios rarely find themselves in trouble.

3. Don’t rush to fix, but do shop around

Fixing now locks in certainty, but at higher rates than many expect to pay long term.

Flexibility remains valuable.

That said, comparing fixed-rate options outside the majors could save you thousands.

4. Expect lending conditions to tighten

If rates rise, borrowing power falls.

This tends to put downward pressure on some segments of the market while strengthening others (think: A-grade locations, scarce family homes, lifestyle and gentrifying suburbs).

Careful property selection, especially for investors, becomes even more crucial.

5. Investors with strong incomes and buffers will be the winners

Periods like this often quietly reward those who remain active while others retreat.

But the key is strategic activity, not speculative risk-taking.

As someone who has watched these cycles for a long time, I'll say this: the market always overreacts, both on the way up and the way down.

Will the RBA hike in February? Possibly.

Will that derail the property market? Highly unlikely.

Australia’s chronic undersupply, strong migration, and resilient labour market provide a powerful foundation that rate adjustments alone can’t topple.

But the investors who thrive are the ones who stay informed, stay prepared, and stay strategic.

This latest shift from the banks is a timely reminder: the era of cheap money is over, and the era of smart money has begun.