Once a rite of passage, owning a home in Australia now seems like a privilege reserved for the few.

How did we get here?

A recent article in the Australian Financial Review exposed a dramatic shift in the housing market, one where the dream of owning a home is increasingly reserved for the affluent.

And as Australia heads towards another federal election, the issue of housing affordability for younger generations will likely take center stage, is young Australians complain that the dream of owning a home is increasingly reserved for the affluent.

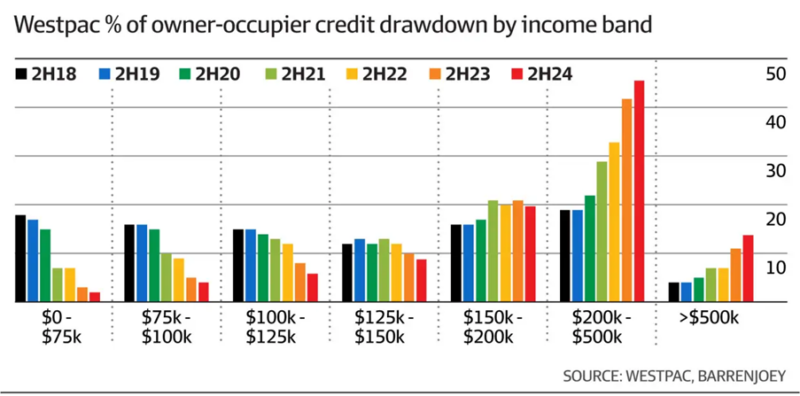

The disparity in mortgage credit distribution

In the past six years, there has been a shift in how mortgage credit is allocated across different income groups.

The AFR reports analysis by veteran banking analyst Jonathan Mott of Barrenjoey using Westpac data which reveals that just six years ago - back in 2018 –– households earnings under $125,000 received 50 per cent of owner-occupied mortgage credit, while households earnings over $200,000 received about 23 per cent.

Now, those numbers look much different.

Those earning under $125,000 received just 12 per cent of owner-occupier loans, while those households earning over $200,000 received over 60 per cent.

More than that, households earning over $500,000 – that is, the top 1 per cent to 2 per cent of households in Australia – now receive more owner-occupier credit than the bottom 55 per cent.

This stark imbalance shows how housing credit has transformed into a luxury good, further accentuating the economic divide.

Source: Australian Financial Review

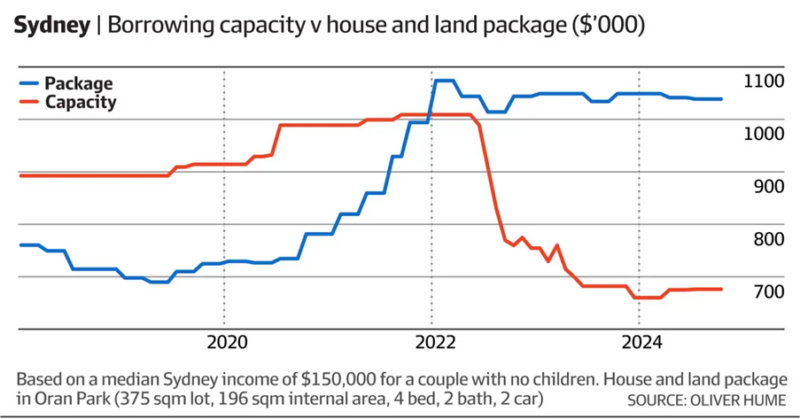

The rising cost versus falling borrowing capacity

The impact of this credit shift is more pronounced when viewed through the lens of actual housing costs versus borrowing capacity.

In Melbourne's northern suburbs, the price of an average house and land package has jumped 39% in just six years to $751,000.

- Also read:Making an offer on a property – what price should you offer?

- Also read:Caveats – The Red Flags of Real Estate

- Also read:Are all real estate agents rich and overpaid?

- Also read:The offer and acceptance process when buying a property

- Also read:How much of your income should you spend on a mortgage?

Meanwhile, the borrowing capacity of a typical dual-income young household has declined by 24% to around $522,000.

Source: Australian Financial Review

A similar pattern emerges in Sydney, with house and land packages rising by approximately 37% to $1,040,000, outpacing the borrowing ability of young couples, which has also decreased by about 24% to $676,000.

Source: Australian Financial Review

Policy recommendations and the path forward

Addressing these challenges requires a multifaceted approach according to Mott who suggests several policy interventions to ease the burden on first-time homebuyers:

- Lowering capital requirements for first-home buyer loans

- Excluding student debt from borrowing capacity assessments

- Allowing for higher borrowing limits for those accepting greater risks

- Enabling young Australians to use their superannuation for home purchases

Further, a Liberal-led Senate committee has proposed that the Australian Prudential Regulation Authority (APRA) incorporate first-home buyer considerations into their policy frameworks.

They recommend using a lower serviceability buffer for first-home buyers, recognising that younger households generally have a stronger income growth outlook.

The bottom line

It should be remembered that last year, there were around 530,000 property transactions in Australia and around 110,000 first home buyers getting into the market.

This means that around 20% of all transactions were to first-time buyers who managed to overcome the many hurdles in their path.

However, as young Australians grapple with a property market that increasingly feels like a fortress to the wealthy, the need for innovative, inclusive housing policies has never been clearer.

Let’s see what our politicians come up with this election year.