Key takeaways

Relying only on super, even at the “comfortable” benchmark, leaves retirees at risk of running out of money.

Building wealth outside of super—particularly through a strategic property portfolio—is essential for financial freedom and peace of mind.

Retirement should be about enjoying life, not just scraping by.

Have you ever stopped to wonder how long your super will actually last you in retirement?

Most Australians glance at their balance and assume it will be enough.

But the truth is sobering: if you retire at 67, there’s a very good chance you’ll spend 20 to 25 years in retirement—and the average super balance simply won’t stretch that far.

We’re living longer than ever before, but our retirement savings haven’t kept pace.

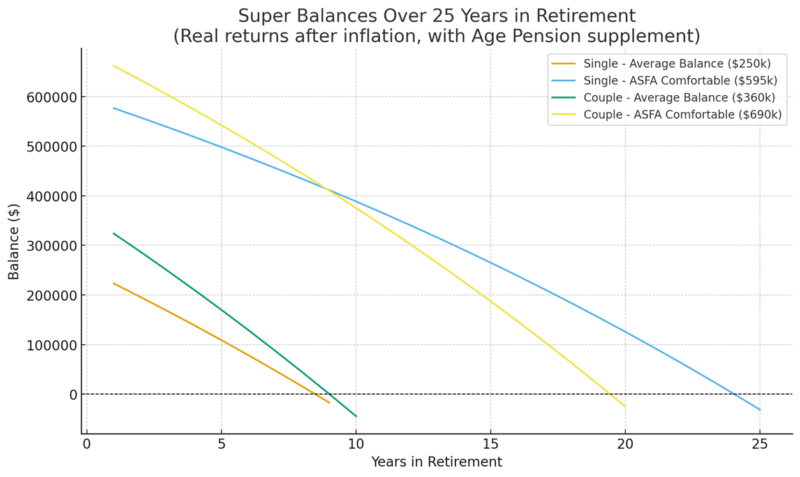

According to the ATO, the average superannuation balance for someone retiring at 67 is about $250,000 for singles and $360,000 for couples.

That might sound like a healthy nest egg, but when you compare it to the Association of Super Funds Australia (ASFA) “comfortable retirement” benchmark of $595,000 for singles and $690,000 for couples, you can see the problem straight away.

Most Australians are entering retirement with a six-figure shortfall.

The longevity trap

Let’s put some numbers behind this.

A “comfortable” retirement is estimated to cost around $51,000 per year for singles or $72,000 per year for couples (assuming you own your home outright).

Yes, the Age Pension will cover some of this, but not enough.

When we modelled these scenarios, here’s what we found:

- Single with average balance ($250k): Super runs out in about 10–12 years, well before the end of a 25-year retirement.

- Single with ASFA benchmark balance ($595k): Lasts almost the full 25 years, but the balance dwindles close to zero by the end.

- Couple with average balance ($360k): Runs out in roughly 12–14 years.

- Couple with ASFA benchmark balance ($690k): Manages to last most of the 25 years, but again, without much buffer.

That’s the trap: even if you do everything “right” with super, you might only just scrape through, with no safety net for rising medical costs, aged care, or the unexpected.

Why super alone won’t cut it

There are three big risks in relying on super alone:

- Also read:6 Lessons from Robert Kiyosaki’s Rich Dad Poor Dad to Build Wealth and Financial Independence

- Also read:Retirement might not be as enjoyable as you expect

- Also read:3 Lessons I learned at Wealth Retreat

- Also read:How does my super get taxed?

- Also read:Why Testamentary Trusts Aren’t Just for the Rich: A Guide to Safeguarding Your Legacy Introduction

- Longevity risk – living longer than your money does.

- Inflation risk – the cost of living keeps rising, eroding your purchasing power.

- Sequence-of-returns risk – if markets fall in the early years of your retirement, your super balance may never recover.

Super is an important pillar, but it was never designed to be the sole answer.

It needs to be supported by other income-producing assets.

The role of real estate in retirement planning

That’s where residential property comes in. A well-chosen property portfolio does three things that super alone cannot:

- Provides rental income that can supplement or replace pension payments.

- Hedges against inflation, since both property values and rents tend to rise over time.

- Builds wealth through leverage, letting you grow a more substantial asset base while you’re still working.

Unlike super, which is locked away until retirement, property can be shaped to suit your needs along the journey, you can sell, refinance, downsize, or simply live off the income.

The bottom line

If you’re heading into retirement with only the average super balance, you’re on track to face a very long retirement funded by very modest means.

Even those who meet the “comfortable” benchmark are at risk of running out of money by their late 80s or early 90s.

That’s why it’s critical to start building assets outside of super during your working years.

A strategically built property portfolio doesn’t just provide wealth—it provides peace of mind.

Because at the end of the day, retirement shouldn’t be about just scraping by. It should be about enjoying the decades you’ve worked so hard for.

Ready to take the next step?

If you’re serious about securing your financial future, it starts with having a clear plan. At Metropole, our experienced wealth strategists can help you map out a path to build the right assets today, so you’ll have the financial freedom you deserve tomorrow.

Why not book a complimentary Wealth Discovery Chat with one of our team?

Act now and click here to organise your chat. You’ll walk away with clarity, confidence, and a strategy tailored to your goals.

Because the best time to prepare for retirement was yesterday. The second-best time is today.