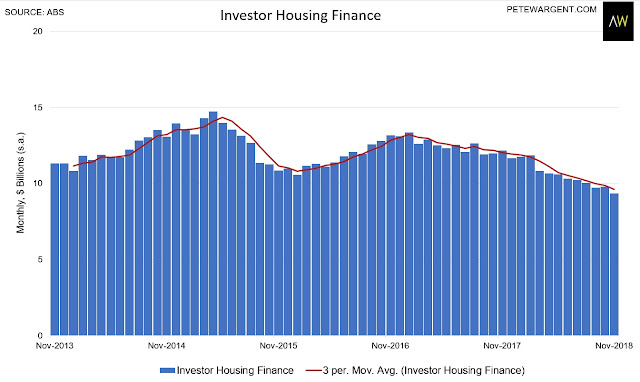

Some commentary speaks of investors voluntarily pulling back, but this hasn't been my experience at all - most industry practitioners appear to have people queuing up to borrow and invest, but credit won't be extended on tighter regulation and criteria.

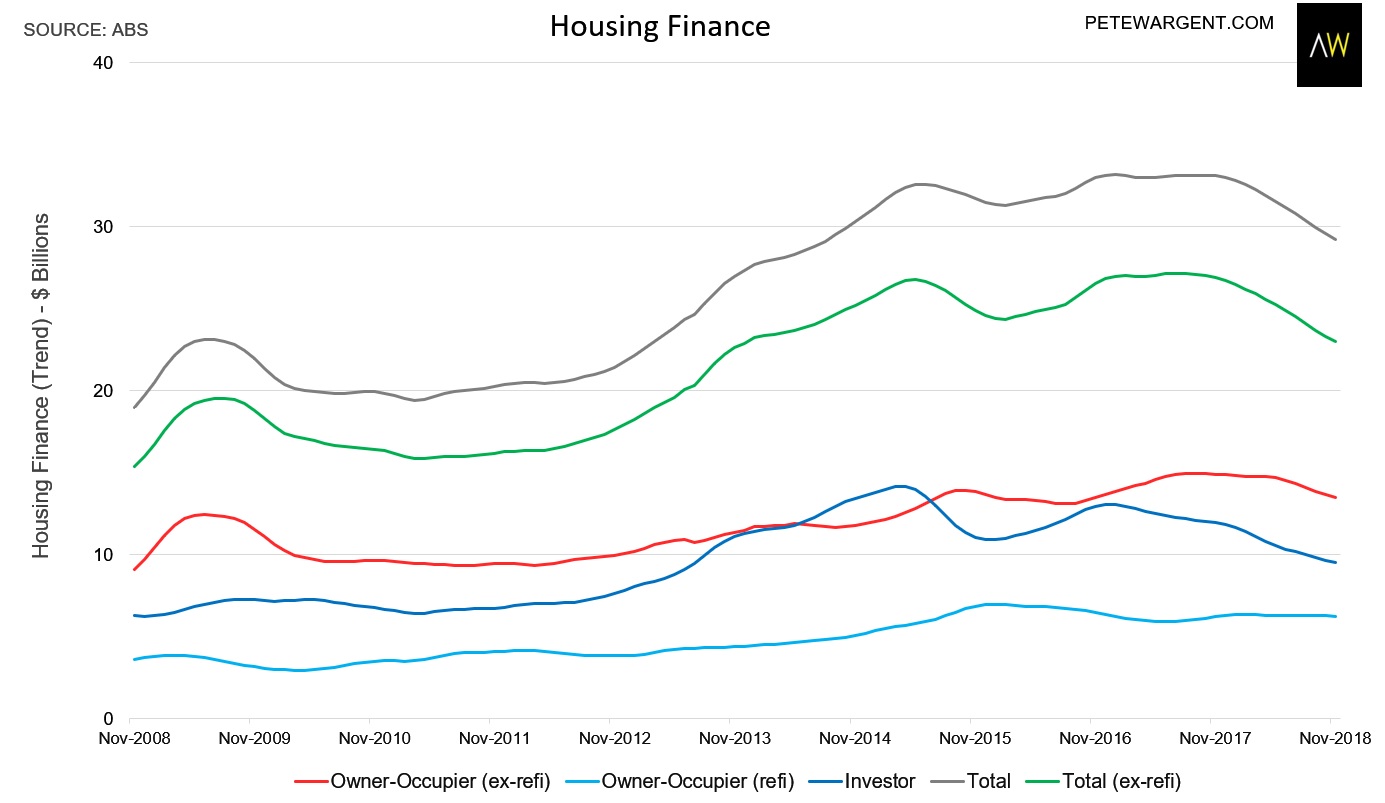

The trend for monthly housing finance was down nearly $4 billion or 12 per cent from a year earlier at $29 billion, as too many different constraints on lending bit in unison.

Labor's negative gearing and capital gains tax policies were proposed all the way back in 2016 to level the playing field and reduce investors in the market

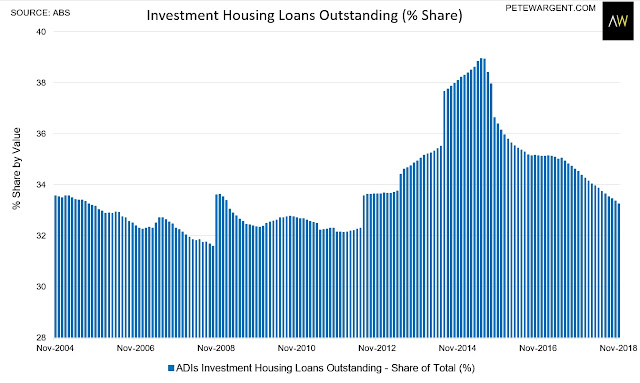

This has already happened with investment loans down by more than a third, but I doubt the ALP will back down because election promises will be made on the back of the supposed 'savings'.

However, it's increasingly difficult to see how the ALP can claim $32 billion of savings when there's no growth in tax deductible debt and the Coalition has already stripped out Division 40 deductions (while there presently aren't any capital gains to tax either!)

Average loan sizes declined for both homebuyers and investors in November.

Commentators have called at least a dozen of the last zero recoveries for Western Australia, but tentatively this is now happening with the trend number of home loans on the rise out west.

Soft almost everywhere else.

New home sales are also trending down.

- Also read:The latest Corelogic Rental Market Report

- Also read:The Boom and Bust of our Property Cycles: A Journey Through the Investor’s Mind

- Also read:Perth housing market update | April 2024

- Also read:Latest property price forecasts for 2024 revealed. What’s ahead in our housing markets in the next year or two?

- Also read:Sydney housing market update | April 2024