Key takeaways

When it comes to property investment, many buyers and investors become obsessed with the idea of timing their property purchase with the view that buying at the bottom of the market for the cheapest price is a formula for property success.

And considering the current property market conditions, this seems more prevalent than ever.

But that’s the wrong strategy to employ.

While it's tempting to try to time the market to maximise your profits, this strategy is often a poor choice for property investors. Instead, focusing on "time in the market" is a much more effective approach.

In fact, timing the market is one of the biggest mistakes a property investor can make.

However, "time in the market" is far more important than timing the market.

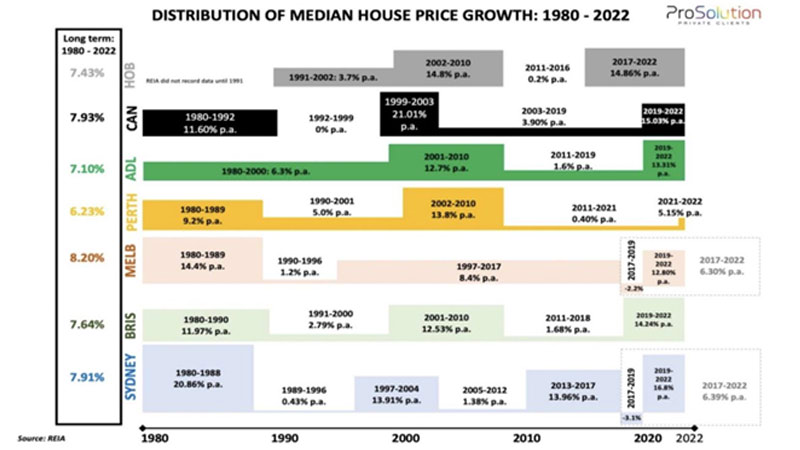

The Melbourne housing market experienced an average compounding property price growth of 8.2% over the last 40 years.

The Sydney housing market experienced an average compounding property price growth of 7.9% over the last 40 years.

The Brisbane housing market experienced an average compounding property price growth of 7.6% over the last 40 years.

Currently there is a window of opportunity for cashed up investors and home buyers with a long term focus.

When it comes to property investment, many investors and buyers become obsessed with the idea of timing their property purchase with the view that buying at the bottom of the market for the cheapest price is a formula for property success.

And considering the current property market conditions, this seems more prevalent than ever.

But, in my mind, timing the market is one of the biggest mistakes a property investor can make.

While it's tempting to try to time the market to maximize your profits, this strategy is often a poor choice for property investors.

Instead, focusing on "time in the market" is a much more effective approach.

And here’s why.

Everything works in cycles

Australia has eight states and territories and the property markets in each location have their own cycle, and then there are property market cycles within those cycles.

They all also vary in length and are affected by a myriad of social and economic factors and then, at times, the government lengthens or shortens the cycle by changing economic policies or interest rates.

The issue is that no one really knows, not even the experts, how long each cycle will last because it depends on a huge number of variables including economic conditions as well as human behaviour – and we all know how hard that is to predict.

CoreLogic’s data is a clear reminder of the cyclical nature of housing markets and how despite all the challenges thrown at them, our property markets are resilient.

What happened over the last 40 years

Independent financial commentator Stuart Wemyss of Prosolution Private Clients has charted ABS statistics going back over 40 years.

- The Melbourne housing market experienced an average compounding property price growth of 8.2%

- The Sydney housing market experienced an average compounding property price growth of 7.9%

- The Brisbane housing market experienced an average compounding property price growth of 7.6%

In other words, well-located properties in our 3 big capital cities have more than doubled in value every 10 years.

And while this long-term growth is impressive, as I said, it's important to remember that each state has its own property cycle with years of minimal or no growth followed by periods of strong growth.

What property investors need to do instead

Instead of timing the market, which is like getting a one-off “free kick”, sophisticated property investors understand that they need to focus their efforts on buying an investment-grade property, in an A-grade location at the time that suits them.

The important part of that statement is that they always buy “investment grade” properties in good locations because these are the types of properties that will outperform in the long run.

Smart investors don’t wait for the lowest prices or a downturn; they buy when they have their finances ready.

It can be tempting, to wait for a market downturn with the idea that you’ll get more ‘bang for your buck’.

But the reality is that investment-grade properties in good locations are more stable than in other markets because they are in continuous, strong demand.

This means that it doesn’t really matter when you enter the market if the value of your property will double in value over a 10-year period as it has over the last 40 years.

What’s important is that you hold the property for long enough to see compound growth.

This strategy would also help you to ride out any temporary market fluctuations.

That way, when it comes time to sell down some of your assets when you reach retirement, or whenever is the right time for you, you will have created wealth from your portfolio's compounding equity over the decades.

What about high interest rates - should I wait for them to drop?

Now, I know some investors are concerned that high interest rates mean it costs more to hold a property with a mortgage, fewer people can afford to buy a house, and more properties will end up on the market as "stretched" investors and homeowners try to sell up, and that higher rates could, therefore, cause house prices to fall for an extended period.

So, in their mind, it makes sense to try and time the market.

While high interest rates may cause some potential real estate investors to hesitate, waiting to buy an investment property can actually be detrimental in the long run.

When interest rates eventually drop and property affordability increases, the many homebuyers and investors who are currently sitting on the sidelines will jump back into the market, pushing up property values.

By the way...there are many, many other factors affecting house prices than just interest rates.

The following chart shows how in the 1980's and 1990's, during periods of very high interest rates, property values kept rising.

And of course that’s exactly what we experienced over the last few years.

Source: Lindeman Reports

There are a number of interesting observations from the chart above:

1. Even at 6.5-7%, interest rates today are still historically quite low despite 13 recent rises.

- We're a far cry from the 17% interest rates of the late 1980's (that I still remember well).

- We're also far well below the pre-GFC interest rates of almost 10%

- And we're even still below the 8% or so rates of 2010/11.

2. The upward movements in interest rates over the last 40 years haven't often resulted in a fall in the median house price.

I'll go into some detail about these other factors below.

Will we have a market downturn?

The forecasts for property values to fall 10-15% are far behind us.

Mid-last year there were headlines in the Australian Financial Review claiming a big crash in prices ahead.

But the fact is, a fall of 10-15% has never happened before.

Not during the recession of the 1990s, not during the global financial crisis, and not during the period of a credit squeeze in 2017-18.

The worst slump in the overall Australian property market was after the credit squeeze in 2016-17 and when there were concerns around proposed changes to negative gearing before the 2019 election.

And at that time the peak to trough drop between December 2017 and June 2019 was 9.9%.

Today, property prices are either over, at, or close to their pre-interest rate rise peaks of, the 2022 boom, and the recovery is only expected to continue.

And as I said, when interest rates begin to fall, more buyers will be drawn back to the market and demand will spike, supporting prices even further.

So let's look at some of the prevailing influences on the housing markets.

Negative influences on our property markets

Sure our housing markets are facing some headwinds, including:

- Consumer confidence has taken a significant hit and that's affecting our housing markets with buyers being more cautious with many taking a wait-and-see approach, while sellers’ confidence is more fragile.

- Fear of high inflation and cost of living pressures is side-lining many buyers.

- Higher interest rates have caused buyers to have a reduced borrowing capacity.

- Uncertainty about our economic future, including ongoing geopolitical problems, slow growth, tight economic policy, and a soft outlook for the Chinese economy, is dampening buyer and seller confidence.

- Affordability issues will constrain many buyers: Rising property values at a time when wage growth has been moderate at best and minimal in real terms for most Australians—means that the average home buyer won’t have more money in their pocket to pay more for their home.

On the other hand, there are some...

Strong fundamentals underpinning our housing markets

These include:

- There is a severe shortage of good properties for sale and virtually no properties to rent.

- FOMO (Fear of Missing Out) has returned across the country. A surge of buyers has returned to the market ahead of the predicted cash rate cut later this year. This is in stark contrast to last year when buyers were more cautious and took their time to make decisions.

- International immigration is strong, and this will further increase the demand for housing.

- There is little new construction in the pipeline – we’re just not building enough dwellings, and increasing construction costs at a time of a shortage of labour means the end value of new projects will need to be up to 30% higher to make projects financially viable for developers.

- Our economy is still growing strongly and is very resilient.

- Unemployment continues to be at very low levels meaning anyone who wants a job can get a job (so they'll be able to pay the mortgage repayments).

- Wages are starting to grow.

- Even though we have been saving less over the last couple of years due to the rising cost of living, overall household balance sheets are strong.

- Most of Australia’s mortgage holders have been able to adjust to higher interest rates, with “close to 99%” of loans remaining on or ahead of repayment schedules, according to the head of the Reserve Bank’s financial stability unit.

- We have a strong banking system that has been strict in its lending criteria, meaning there are very few non-performing loans.

- There are still Government incentives to encourage first-home buyers into the market.

There is currently a window of opportunity

Taking away consumer sentiment, Australia's housing and economic fundamentals are very sound.

Households are cashed up, equity growth has been phenomenal for most homeowners and property investors, the jobs market is strong, and Australia's mortgage delinquencies are very low.

This means that the current poor consumer sentiment, when most other economic fundamentals are strong, is a bit like a cloud covering the sun.

- Also read:This week’s Australian Property Market Update – Latest Data, State by State April 23rd 2024

- Also read:Latest property price forecasts for 2024 revealed. What’s ahead in our housing markets in the next year or two?

- Also read:Melbourne property market forecast for 2024

- Also read:Brisbane’s property market forecast for 2024

- Also read:Sydney property market forecast for 2024

Spring will follow Winter, and Summer will follow Spring—this, too, will pass, and the long-term upward trend of the value of well-located properties will continue.

So my recommendation is that if you're in a financially sound position, you should not try and time the market, but rather buy while others are sitting on the sidelines.

If you think about it...

- There is less competition at present.

- You have more time to conduct your research and due diligence.

- It's a buyer's market so you'll have the upper hand in negotiations.

But don't look for a bargain - A-grade homes and investment-grade properties are in short supply and still selling for reasonably good prices.

These high-quality properties tend to hold their value far better than B and C-grade properties located in inferior positions and inferior suburbs.

There’s a saying in property circles that goes:

When was the best time to buy property? - 20 years ago!

When is the second-best time? - Today!

In other words, you buy when you can afford to and when you are ready to.