Our property markets started 2020 on a strong note.

In the year to March 2020, Sydney and Melbourne house prices have risen 14.5 per cent and 12.5 per cent respectively.

Sydney house prices made up almost all of their lost ground and were likely to reach a new peak shortly, while the Melbourne property market reached a new peak in March.

But then Coronavirus started wreaking havoc on the Australian economy, and while house prices are holding up for now, the COVID-19 crisis has halved property transactions bringing back the property pessimists and doomsayers.

They cite the problems of rising unemployment, falling consumer confidence, a pending recession, restrictions on inspections and auctions and more cautious bank lending practices as reasons why our property markets will tank.

So what’s going to be the economic cost of the coronavirus?

How will COVID-19 affect our property markets and housing prices?

I’ll try and answer these and more questions in this Q&A:

We all know Australia is going into recession, but how bad will it be and how long will it last?

The International Monetary Fund has forecast that the Australian economy will contract by 6.7 per cent in 2020 due to the coronavirus lockdown.

However, the IMF expects the domestic economy to rebound by 6.1 per cent in 2021, assuming that measures to contain the virus are successful.

The IMF's outlook also forecasts that global GDP growth will fall by three per cent in 2020, compared with just 0.1 per cent during the global financial crisis.

Here's what the RBA says will happen to our economy.

Australia this is likely to commence in the second quarter of 2020 which we’re in right now and inevitably we will see some horrible numbers for GDP – economic growth and unemployment.

But a combination of monetary and fiscal responses should see us begin to rebound in the third quarter or fourth quarter of this year.

The RBA recently updated its economic outlook in its May Statement on Monetary Policy.

The RBA provided three economic scenarios, namely a baseline, upside and downside.

Their baseline scenario is a very large fall in activity of 10% over the first half of 2020 with unemployment peaking at 10% in Q2 and then they expect our recovery to start as health restrictions are rolled back

Coronavirus containment measures have seen consumer spending and business investment fall sharply as people have lost their job, restrictions have limited spending and firms sought to conserve cashflow amid the steep fall in demand.

In addition, travel bans have seen a collapse in tourism and education exports.

The RBA notes that while it expects employment to fall 8%, or by 1 million workers, there will be a sharper 20% fall in total hours worked.

This means there will be an extremely large hit to household income even with extensive government handouts and its wage subsidy scheme, which will weigh on consumer spending during the recovery.

The bank also warns that while it expects unemployment to rise to 10% it is uncertain about how many people will drop out of the labour force in this unusual period.

In its baseline case the RBA forecasts that unemployment will then recover steadily from 10% in Q2 2020 to 6.5% in Q2 2022.

Of course these are just best assumption forecasts but recently AMP’s chief economist Shane Oliver highlighted three reasons why Australia is well placed to rebound from the shutdown as compared to other countries around the world.

- Firstly, we have flattened the curve of the Coronavirus remarkably quickly, to the extent that there are now only 20 remaining cases in ICU (which represents less than 1 per cent of ICU beds capacity).

- Secondly, Australia was in a strong fiscal position thanks in part to the resources boom and some prudent Budget management.

And our fiscal response has been the biggest across the entire G20 – not in terms of loans and guarantees, which tend to saddle businesses and individuals with more debt – but in terms of direct fiscal support, actual spending and revenue measures.

The government stimulus packages were originally designed with a 6-month hibernation of the economy in mind, but we could and should be back to business much sooner than that. - Thirdly, China has long since brought COVID-19 under control, and as such is 2 or 3 months ahead of the rest of the world in ramping up its activity, with early signals suggesting infrastructure bullishness and a construction uplift.

This is terrific news for Australia, since China is now by far our most important trading partner, and we should benefit in terms of our resources economy.Indeed the international trade figures for March showed a tremendous uplift in the value of Aussie exports, especially to China.

Of course the second quarter of 2020 will inevitably produce some horrible numbers for growth and unemployment, and not only in Australia.

The Reserve Bank of Australia is also providing $90 billion to the banks at a rate of 0.25 per cent to ensure a cheap line of credit is available throughout the crisis.

The RBA will fund the banks at that low rate over three years, and provide additional funding if the banks increase lending to small and medium-sized businesses

Clearly our housing markets won’t be immune to the Coronavirus economic fallout, but the impact on property values will depend on how long it will take to contain the virus.

Transaction levels are likely to be significantly impacted over the next two months, particularly with restrictions in place limiting people’s ability to leave their homes.

Transaction levels are likely to be significantly impacted over the next two months, particularly with restrictions in place limiting people’s ability to leave their homes.

But this doesn’t mean property values will plummet.

In China, property transactions were at or around zero for the three weeks following movement restrictions and have since (two months later) recovered to 50% of their four-year average.

So while property values may fall a little in the next few months, that won’t really be a reflection of their “intrinsic value” but more a reflection of the market lockdown.

And sooner rather than later we’ll come to a point where property transactions and prices will reflect the fundamentals of the Australian economy, as opposed to the current structural changes taking place.

On the flip side of the coin, suppressed transaction activity means we expect to see a build-up of latent demand and the markets will rebound in the second half of the year.

It is understandable that many Australians expect the property markets to behave like it did during previous economic downturns such as the Global Financial Crisis in 2008.

However, unlike previous downturns that were essentially financially lead, this downturn is a medical problem that morphed in an economic issue because of a short-term shutdown of our economy.

That is very different from a recession preceded by economic excess and speculation.

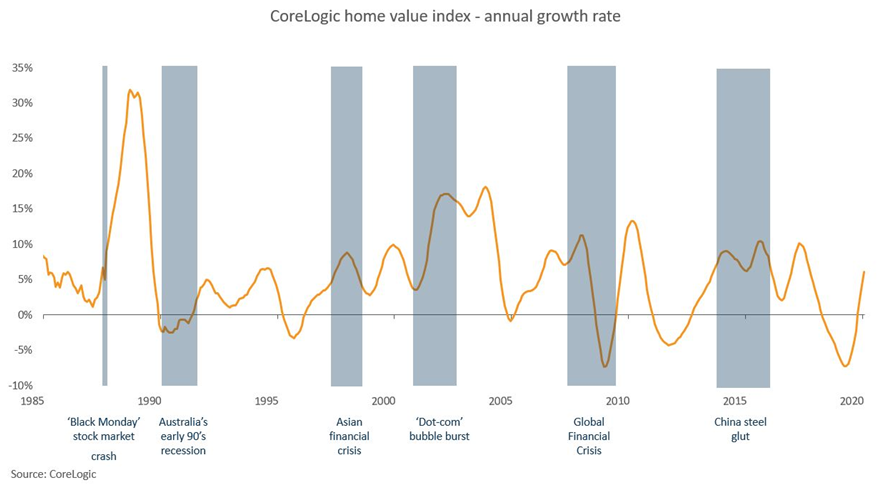

Based on the predicted pace of the post-recession recovery, I would expect the pandemic to have a more limited and shorter-lived impact on house prices than either the early-1990s recession or the Global Financial Crisis.

So, in the short term:

So, in the short term:

- "Investment grade" properties and A grade (above average) homes could fall in value by around -5%

- B grade (average) homes could fall in value by up -10%,

- C grade (less than perfect) will be the hardest hit as there will be a flight to quality.

But this will be on a on very low levels of transactions and he pace of recovery from that point will depend on the state of the wider economy.

The worst affected market will be the more expensive properties that will suffer because of the stock market crash.

And properties in the blue-collar areas and new housing estates where young families are likely to have overextended themselves financially and with many people will be out of work for a while.

On the upside, households and property investors whose incomes remain stable and secure will be able to take advantage of historically low interest rates.

This should support a return to stronger levels of price growth in the medium term.

The following chart shows how Australian residential property has historically fared well against negative economic shocks

Sydney was the strongest property market at the end of 2019 and since bottoming out in May 2019, Sydney dwelling values have recovered most of the losses sustained in previous years and were heading for anew peak in the second quarter of 2020.

Now coronavirus has made all those forecasts of double-digit capital growth for Sydney property fall by the wayside.

The length of the coronavirus shut down, the levels of unemployment and the fall in consumer confidence will determine what happens to Sydney property.

Clearly auctions won’t be conducted in the Sydney property market for some time to come, but more properties will be sold by private treaty.

Clearly auctions won’t be conducted in the Sydney property market for some time to come, but more properties will be sold by private treaty.

Currently investors and home buyers are abandoning the off the plan apartment sector for many reasons including concerns about construction standards and now they have another issue – COVID-19 to worry about.

Many of those who purchased off the plan properties in Sydney a few years ago are now having trouble settling with valuations on completion coming in at well below contract price at a time when banks are more reluctant to lend on these properties.

The banks have also become more reluctant to lend in certain Sydney postcodes, changing the credit policies (lowering their maximum loan to value ratios), particularly for off the plan properties in selected Sydney postcodes.

For some banks these less favoured postcodes include: Alexandria, Asquith, Hornsby, McQuarie Park, Epping, Mays Hill, Pendle Hill, Wentworthville, Westmead, Kellyville, Rouse Hill, Sutherland and Gosford.

At the same time, with the stock market being shattered, Sydney’s more exclusive properties will suffer as normally happens when the stock market collapses.

Similarly, properties in the outer suburbs where local residents will feel the fallout from job losses will suffer.

However well-located apartments and A grade homes in Sydney’s middle ring suburbs should hold their own falling around 5% in value.

Sydney will see fewer property transactions occurring as many high-end homeowners and empty nesters who don’t need to sell will be putting their homes of the market.

The Melbourne property market has been one of the strongest and most consistent performers over the last few decades.

Last year Melbourne house prices recorded the strongest resurgence on record to reach new peaks in March 2020.

But now the Melbourne housing market will be affected by fallout from the COVID-19 as vendors consider pulling their properties from the market during the coronavirus crisis, fire sit on the sidelines waiting to see what happens.

But now the Melbourne housing market will be affected by fallout from the COVID-19 as vendors consider pulling their properties from the market during the coronavirus crisis, fire sit on the sidelines waiting to see what happens.

Melbourne is auction capital of Australia; some would say auction capital of the world, and obviously auctions will not be conducted for some time.

Of course this doesn’t mean property transactions won’t occur. It just means more properties will be sold by private treaty.

However, new sellers are holding off listing their properties for sale, while discretionary sellers who have their properties on the market are cancelling their actions and either hoping for a private sale, or holding off marketing their properties till things get back to normal.

Melbourne’s more expensive properties and those in the outer suburbs will suffer the most, while we are located townhouse, villa units and A grade homes should hold their values well, as most Melbourne residents will still have the jobs and won’t be selling up because of Corona virus.

The banks have also become more reluctant to lend in certain Melbourne postcodes, changing the credit policies (lowering their maximum loan to value ratios), particularly for off the plan properties in selected Melbourne postcodes.

For some banks these less favoured postcodes include: Brunswick, Brunswick East, Fitzroy, Fitzroy North, Abbotsford, Doncaster, Cremorne, Richmond, Box Hill, Prahran, Windsor and Port Melbourne.

Melbourne real estate has always been very resilient and held its own during downturns like the Global Financial Crisis and other stock market collapses.

Brisbane’s property downturn in 2018-9 was quite shallow compared to the big two capital cities and following its recent upturn property values have reached a new peak.

However, Brisbane property prices are still about 55% of Sydney’s while household incomes are only around 12% lower, underpinning the value of Brisbane real estate.

However, Brisbane property prices are still about 55% of Sydney’s while household incomes are only around 12% lower, underpinning the value of Brisbane real estate.

In general Queensland is highly exposed to the Chinese economy, in particular tourism, education and foreign property purchases.

This means the Queensland property markets are likely to suffer but as opposed to regional Queensland, the Brisbane real estate market is underpinned by multiple pillars, and therefore likely to suffer less than the Gold Coast and Sunshine Coast or regional Queensland.

Having recently suffered an oversupply of new and off the plane properties, the banks are again being cautious and reluctant to lend to new or off the plan propertyies in selected Brisbane postcodes by lowering the maximum loan to value ratio.

These postcodes include: Chermside, Hamilton, Milton, Toowong, Woolloongabba and Biggera Waters

Now read: Brisbane property market – how will Coronavirus affect it?

On the flipside, once travel bans are lifted, the Queensland economy and property market should benefit from more local travel by Australians as it is likely that overseas travel will still be restricted.

What will happen to property markets in the long term?

In the medium term, property values will be linked to the extent that quarantine measures affect income, employment, borrowing capacity and credit availability.

Some sectors of our housing markets will be affected more than others.

The largest and most direct industry shocks from the coronavirus are expected in:-

- Tourism, local restrictions will ease up before and overseas travel restrictions may take some time to lift;

- Hospitality, where social distancing leads to a decline in café, bar and restaurant patronage;

- Education, due to fewer foreign students being able to travel;

- Retail, which will be dragged down by low consumer confidence levels; and,

- Recreation, theatres , cinemas and art galleries have closed down.

However, I'm comfortable with the underlying long term fundamentals supporting our property markets int he medium to long term.

Let’s look at a couple of them…

- Population growth

Australia’s population is growing by around 360,000 people per annum, meaning we need to build around 170 to 180,000 new dwellings each year to accommodate all the new households.

Since 60% of our growth is dependent on immigration, in the short-term population growth will fall, but they should increase again as soon as overseas immigrants will be allowed to come to our shores.

- Declining housing supply

The oversupply of dwellings in many Australian locations is now dwindling and there are very few new large projects on the drawing board.

The oversupply of dwellings in many Australian locations is now dwindling and there are very few new large projects on the drawing board.

Considering how long it takes to build new estates or large apartment complexes, we're going to experience an undersupply of well-located properties in our capital cities in the next year or two.

- Interest rates are low and will go down further

The prevailing low interest rate environment is making it easier to own a home, either as an owner occupier or investor.

In fact, it’s never been cheaper for investors to own a property with the “net outlay” – the out-of-pocket expenses - being the lowest they’ve been for decades considering how cheap finance is today.

- Smaller households are becoming the norm

Sure many people live in multigenerational household, but pretty soon Millennials will make up one third of the property market and their households tend, in general, to be smaller as are the households of the booming 65+ year old demographic.

More one and two people households means that, moving forward, we will need more dwellings for the same number of people.

- More renters

Soon 40% of our population will be renters, partly because of affordability issues but also because of lifestyle choices.

The government isn’t providing accommodation for these people. That’s up to you and me as property investors.

- First home buyers are back

First home buyers are back with a vengeance, in part thanks to the government’s new scheme to encourage them, but also because of cheap finance and rising property values.

As opposed to established homebuyer who have a “trade in” that is increasing in value, if first home buyers wait to get into the market they're finding the market moving faster than they can save, so they’re hopping on board the property train as quickly as they can.

- The underlying fundamentals are strong

Sure our economy is facing challenges, and the share market is volatile, but our property markets are underpinned by the fact that 70% of property owners are home owners who are there for the long term.

They're not going to sell up their homes - they'd rather eat dog food than give up their homes.

And the Australia’s banking system is strong, stable and sound.

And the Australia’s banking system is strong, stable and sound.

Even though a few home buyers have overcommitted themselves financially, there should be no real concern about household debt because, in general, it is in the hands of those who can afford it.

There is currently a very low rate of mortgage default of mortgage to increase.

As the community starts to become more concerned about the economic impact of the corona virus, it is likely that there will be a flight to quality assets, and bricks and mortar have always stood the test of time.

In other words, the share market volatility will make some investors look to real estate as an alternative secure investment vehicle underpinned by 7 million homeowners in Australia.

In fact, it the only investment market not dominated by investors.

If you can’t have auctions or public open for inspections what does that mean for a property market?

Auctions are now allowed in in NSW again and hopefully with the relaxed social distancing laws, auctions will be conducted again in other states.

But in the meantime...under the new social distancing recommendations estate agents are still transacting properties and prospective buyers and tenants are looking at properties by private viewing.

- Also read:The Boom and Bust of our Property Cycles: A Journey Through the Investor’s Mind

- Also read:Latest property price forecasts for 2024 revealed. What’s ahead in our housing markets in the next year or two?

- Also read:This week’s Australian Property Market Update – Latest Data, State by State April 16th 2024

- Also read:Melbourne property market forecast for 2024

- Also read:Brisbane’s property market forecast for 2024

While many agents are now putting video walk-throughs online – be careful.

Videos are not a substitute for looking at the property real life.

Videos can hide a multitude of sins, they don’t show you the full perspective, you can’t get an idea of ceiling heights, how well-lit rooms are or real dimensions.

It’s just like reality TV – it’s not real.

So don’t fall into the trap of buying a property sight unseen.

Instead organise a private inspection where you will have the luxury of seeing the property on your own or if you can’t do that yourself get a buyer’s agent to represent you.

Of course you wouldn’t be surprised that I believe you should always have a buyer’s agent representing you, but now it’s more important than ever experienced buyers agents have access to off market properties, and they are able to talk to the selling agent on a professional level meaning they can discover the real motivation of the seller and test agents on the level of discount that can be achieved.

Sure this is a good time to negotiate hard, but don’t be mistaken – not all vendors are highly motivated, and even though property values could drop a little further as the Coronavirus epidemic fallout widens, I don’t see a significant drop in value of well-located investment-grade properties or a great homes.

In other words, if you find the right property at the right price and it suits you long-term strategy – don’t make the mistake of trying to time the market.

Even the smartest market analysts can’t get timing the market right.

What’s happening in the property market at the moment?

Buyers are still buying, and sellers are still selling.

There are two groups of people in our property market - discretionary and non discretionary buyers and sellers.

At times of uncertainty like we’re currently experiencing, discretionary buyers and sellers go on strike.

However, there are still many people who have to buy or sell at present.

For example, families who sold their house a short while ago now have to buy a new property – they need somewhere to live.

Similarly, people who bought a new property recently have to sell your old home.

At the same time, people are moving for new jobs, getting married, getting divorced, having babies. There will always be people who need to transact property.

Having said that, the number of transactions has slowed down considerably.

But remember… much the same happens every year around Christmas time.

Solicitors and conveyancers go on vacation, estate agents, mortgage brokers and banks close down for a while and much of the property market closes for 4 or 5 weeks from around 20 December until after the long Australia Day long weekend at the end of January.

But that doesn’t mean property values plummet they don’t!

Since no transactions are occurring there’s no reason for property values to slump.

Much the same will happen this time around.

Our housing markets will slow down for a short while and then once the lockdown is removed, they will resume activity.

However, this time round general consumer confidence will be dampened but there will still be the non-discretionary buyers looking for property as well as those strategic investors who have prepared themselves during this foundation stage.

They’ll be ready to pounce on the opportunities the marketplace will present them.

Now read: Coronavirus and our property markets – what should you be doing now?

So, can I still sell my home?

Yes – you can.

Real estate agents, buyers’ agents and the rest of the market have adapted to the new restrictions.

Sure the auction market has closed down, but private inspections are now the norm and sellers can still sell via private sale as always.

Remember... in the past more properties have always been sold by private treaty than at auction.

And it’s really only been the Melbourne property market and the Sydney property market that had a high percentage of auction sales.

Won’t rising unemployment kill our property markets?

A: There is no doubt that financial uncertainty, and in particular job uncertainty, negatively impact your property market.

Initially, there were concerns that unemployment rate could reach double digits, but with the most recent financial assistance packages to businesses to keep employees, it’s likely that unemployment will peak at around 8.5%

While unemployment will only have some sectors of business, We are already seeing evidence of how COVID-19 is pushing up the unemployment rate, particularly in the tourism, entertainment and hospitality sectors. Similarly retail and education will be feeling a blow.

The other hand government employment will grow as will implement in the health services sector%.

Is now a good time to buy property?

One of the major lessons I have learned from previous downturns is the importance of taking a long-term perspective which always outsmarts short-term reactive thinking.

And for mine, it’s always property fundamentals that really matter and drive our markets in the long term.

And for mine, it’s always property fundamentals that really matter and drive our markets in the long term.

Things like demographics, supply and demand, affordability, availability finance, and local economic trends.

Of course, we all know the old saying, being fearful when others are greedy and be greedy when others are fearful….

But it’s normal human nature to find it difficult to buy your new home or invest when everyone else is running around thinking the world is coming to an end.

However, now that I have invested through 8 property cycles, I have found that it is exactly these conditions the present the best opportunity.

That means now is the time to get prepared to take advantage of the opportunities that the market will offer.

NOW READ: Is now a good time to buy property?

I’ve read the tenants don’t have to pay rent for six months - is that true?

No that is not the case.

State and territory leaders have agreed to a 6 month moratorium on evictions for tenants in financial distress, but this is not a moratorium on their requirement to pay rent.

The details will be legislated under each state and territory jurisdiction, but so far, only the Queensland government has released details of their scheme.

Of course tenants who are not significantly affected by coronavirus are expected to honour their leases and rental agreements, however at Metropole we have already seen many tenants request rental relief because of job “uncertainty” rather than because they’ve lost their jobs.

What is the Queensland relief scheme?

A one-off payment of up to 4 weeks rent (maximum of $2,000) will be available to eligible tenants who do not have access to other financial assistance, with the grant paid directly to their landlord.

To be eligible, applicants must live in Queensland, have a bond or shortly have a bond with the Residential Tenancies Authority, have less than $10,000 in cash and savings and have applied to Centrelink for income support if they’ve lost their jobs.

Further, these tenants must have first tried to negotiate a payment plan with their landlord.

How should I respond if I’m asked to reduce my tenant’s rent?

Most property investors will be hit by the Corona Crunch at some time and it won’t just be from tenants not being able to pay their rent.

They will be amongst the many people who have been affected by reduced working hours or job loss, and like many Australians will find it difficult to put food on the table for their families.

Clearly this is the time for understanding and compassion – nobody wins by making things difficult for a tenant who is in financial trouble.

Clearly this is the time for understanding and compassion – nobody wins by making things difficult for a tenant who is in financial trouble.

It’s important to understand the tenants don’t want to be in rental arrears, but if paying their rent leaves them without money for food or medical attention, the decision most tenants will make is obvious.

But remember, the moratorium doesn’t allow tenants to simply walk away from their obligations – it’s not a rental holiday.

Don’t be tempted to get personally involved in discussions with your tenant, that’s what you employ a property manager for, so take their professional advice.

Your property manager should ask your tenant to demonstrate true financial hardship directly related to Coronavirus – simply saying “we can’t pay the rent” is not enough.

They will ask evidence of hardship including details of their employment or loss of it, other people living in the property who can supplement the rent, assets including cash at bank, and evidence of applications for Centrelink for assistance, to establish whether the tenant’s claims are authentic.

You see… many tenants will benefit from the JobKeeper or JobSeeker (formerly Newstart) schemes and these tenants should be expected to keep paying their rent.

And fortunately, many investors will be able to fall back on their landlord’s insurance to cover some of their losses, but how the landlord deals with the situation may affect if they can claim insurance.

Will my landlord insurance cover rental losses because of COVID-19?

There are many different insurance companies protecting landlords, offering a multitude of different policies.

I’m pleased to see that currently, they’re standing behind their policies.

According to EBM Rentcover Insurance it is business as usual for your landlord insurance policy.

“Pandemics do not alter any of the existing terms and conditions in your landlord insurance policy.”

‘Rest assured, just because we are in the middle of a global pandemic, an insurance policy will still cover what it is designed to cover. Landlord insurance policies are black and white.”

For more information read more here: COVID-19 and the impact on landlord insurance

Should I agree to reduce the tenant’s rent?

While it is important to be considerate, and I can understand the desire to support a tenant through this difficult time, our recommendation is not to offer reducing or forgoing rent until the government releases details of its rental relief packages.

These were expected to be announced at the end of last week, and as I’ve explained only the Queensland package is available so far.

These were expected to be announced at the end of last week, and as I’ve explained only the Queensland package is available so far.

Reducing rent, putting rent on hold or not issuing late notices will jeopardise a landlord’s ability to claim on their landlord insurance, and may potentially risk any benefits announced as part of the government relief packages.

Until details of the tenant and landlord relief packages are made available, our advice is for landlords to put a payment plan in place for any tenants who are genuinely suffering financial difficulties.

For example, you could offer them an arrangement where they pay less rent (maybe half) for the next few months, but agree to catch up their rental payments through increased rental in 3 or 4 months once they secure employment.

Property investors should also speak to their bank about getting a mortgage holiday – either pausing or reducing their monthly repayments.

Read more: There’s a 6 month moratorium on evictions – what should I do?

What will happen to vacancy rates with unemployment rising?

Obviously a rental markets will also be affected by the COVID-19 Cocoon –with prospective tenants are not as active in the market at present.

Some are bunkering down sharing with their friends, while others have gone home to the comfort of mum and dad's home.

At the same time more properties have become available for lease.

Some of these are were previously being leased to short-term tenants on AirBnB, while others have become vacant as many overseas students have not come back a present to take on the university studies.

This lead to higher vacancy rates for apartments, particularly in Melbourne in Sydney, but at present he doesn't seem to be a dramatic affect on the asking rents.

NOW READ: A landlord’s guide to Coronavirus tenancy problems.

Can my property manager and prospective buyers/tenants still physically inspect my property?

Yes they can, but public open for inspections are banned, meaning prospective buyers and tenants must arrange private inspections and only two people are allowed inside a property at a time.

Property managers can still inspect your property to conduct their regular “routine inspections”, but they will generally ask for you not to be present and will take special precautions by wearing gloves, not touch anything or sanitising anything they must touch like door handles

As always, landlords must give tenants 24 hours’ written notice of entry, stating the reason for entry.

What if I can’t make my mortgage repayments?

Most banks are allowing customers to pause their loan repayments for up to six months if they are experiencing financial hardship.

Contact your broker or bank to discuss your situation as soon as you feel you may be running into trouble, and you may even be eligible for the Government’s stimulus package.

For free financial advice, contact the National Debt Helpline.

Here are some of the options that are available if you run into financial difficulty.

- Use your offset account or a redraw facility.

We always recommend that our clients have an offset account as a financial buffer to see them through difficult times just like this, so many will have funds available to redraw to see them through

- Reduce your repayments.

If you are paying more than the minimum required repayment on your mortgage, as many people have been since they’ve kept up the same repayments as interest rates drop; you can reduce your repayments to the minimum repayment anytime without charge with your lender.

If you are paying more than the minimum required repayment on your mortgage, as many people have been since they’ve kept up the same repayments as interest rates drop; you can reduce your repayments to the minimum repayment anytime without charge with your lender.

The majority of lenders allow you to do this online.

If you choose minimum repayment, be careful to ensure you don’t have excess redraw in your loan account, as this can make the new repayment based on your outstanding balance – causing the redraw to be locked or removed entirely – simple fix, if you have an offset account, you can place the redraw funds into this account.

- Repayment holidays or payment pauses

You need to understand that these aren’t the lenders waiving your repayments or obligations but simply deferring them.

For example, if you take a 6-month payment pause on your loan, then the interest still is charged and capitalised (or added) to your loan.

At the end of this period, then you will then be required to make your normal repayments, PLUS catch up those that you haven’t made over this time.

You will be asked still if you are under some hardship based on the Coronavirus. In other words, have you lost your job or been affected in any other way?

Often the banks will recommend you redraw your loan first if you’ve made extra repayments or use your cash/offset or buffer before going into these measures.

Read more (and watch the video): How will COVID-19 impact on your banking and loans?

So what should I do?

In my opinion for those who have a secure job and their finances organised, this is a great time to buy a home or investment property at a price that you were unlikely to be able to get a couple of weeks ago when the property markets in big capital cities were booming and there were more buyers around than sellers.

It is likely that human nature will cause many would-be buyers to sit on the sidelines for a little while until things become more clear, which means that sellers will be more amenable to accepting offers rather than holding out for a top price.

Remember don’t make long-term decisions like buying a home or an investment property based on the last 30 minutes of news.

There is no doubt there will be opportunities in the market for those who are willing to go against the crowd and when they look back in a year’s time and definitely in 5 or 10 years’ time, they will remember the unprecedented events of 2020 as a great buying opportunity for property.

Now is the time to take action and set yourself for the opportunities that will present themselves as the market moves on

If you're wondering what will happen to property in 2020–2021 you are not alone.

You can trust the team at Metropole to provide you with direction, guidance and results.

In challenging times like we are currently experiencing you need an advisor who takes a holistic approach to your wealth creation and that's what you exactly what you get from the multi award winning team at Metropole.

If you're looking at buying your next home or investment property here's 4 ways we can help you:

- Strategic property advice. - Allow us to build a Strategic Property Plan for you and your family. Planning is bringing the future into the present so you can do something about it now! This will give you direction, results and more certainty. Click here to learn more

- Buyer's agency - As Australia's most trusted buyers’ agents we've been involved in over $3Billion worth of transactions creating wealth for our clients and we can do the same for you. Our on the ground teams in Melbourne, Sydney and Brisbane bring you years of experience and perspective - that's something money just can't buy. We'll help you find your next home or an investment grade property. Click here to learn how we can help you.

- Wealth Advisory - We can provide you with strategic tailored financial planning and wealth advice. Click here to learn more about we can help you.

- Property Management - Our stress free property management services help you maximise your property returns. Click here to find out why our clients enjoy a vacancy rate considerably below the market average, our tenants stay an average of 3 years and our properties lease 10 days faster than the market average.